(Any views expressed here are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

Want More? Follow the Author on Instagram and X

Access the Korean language version here: Naver

The Wharton business school celebrates capitalism and American exceptionalism. Wide-eyed and bushy-tailed students from across the globe drink the Kool-Aid as professors extol the benefits of free-market capitalism and the “rules-based” Pax Americana order, enforced at the tip of a Tomahawk cruise missile. But if your entry into the workplace occurred in September 2008, like mine did, you quickly learned that most of your education was a crock of utter bullshit. The reality is that the system is not a true meritocracy – instead, it’s the firms that can best suckle on the government teet that end up being the most financially successful. Capitalism is for poor people.

I learned my first lesson in real capitalism—or what I now refer to as corporate socialism— after seeing which bulge-bracket investment banks prospered and which faltered in the aftermath of the 2008 Global Financial Crisis (GFC). The American banks, after Lehman Brothers’ bankruptcy, all took government bailouts via direct equity injections. Although the European banks received secret financial support from the U.S. Federal Reserve (Fed), they didn’t receive government equity injections or forced mergers (paid for with central bank loan guarantees) until 2011. So, when my analyst class at Deutsche Bank received our first full year bonus in February 2010 for the 2009 calendar year, we came up short vs. our friends who worked at the American banks that had pressed F9.

This is the KBW banking index, which includes the largest U.S.-listed commercial banks. It rallied over 500% from its post-GFC March 2009 lows.

This is the Euro Stoxx banks index, which includes the largest European banks. It only rallied 100% from its post-2011 crisis lows.

Corporate socialism is far more profitable and prevalent in America than in Europe, regardless of what the political pundits say.

Just remember, kids, privatised gains and socialised losses are the recipes for a large bonus.

Given China’s rhetoric about its economic system’s supposed difference and superiority to those practised in the West, you’d think they might enact different policies to solve their economic problems. Wrong.com, plebe.

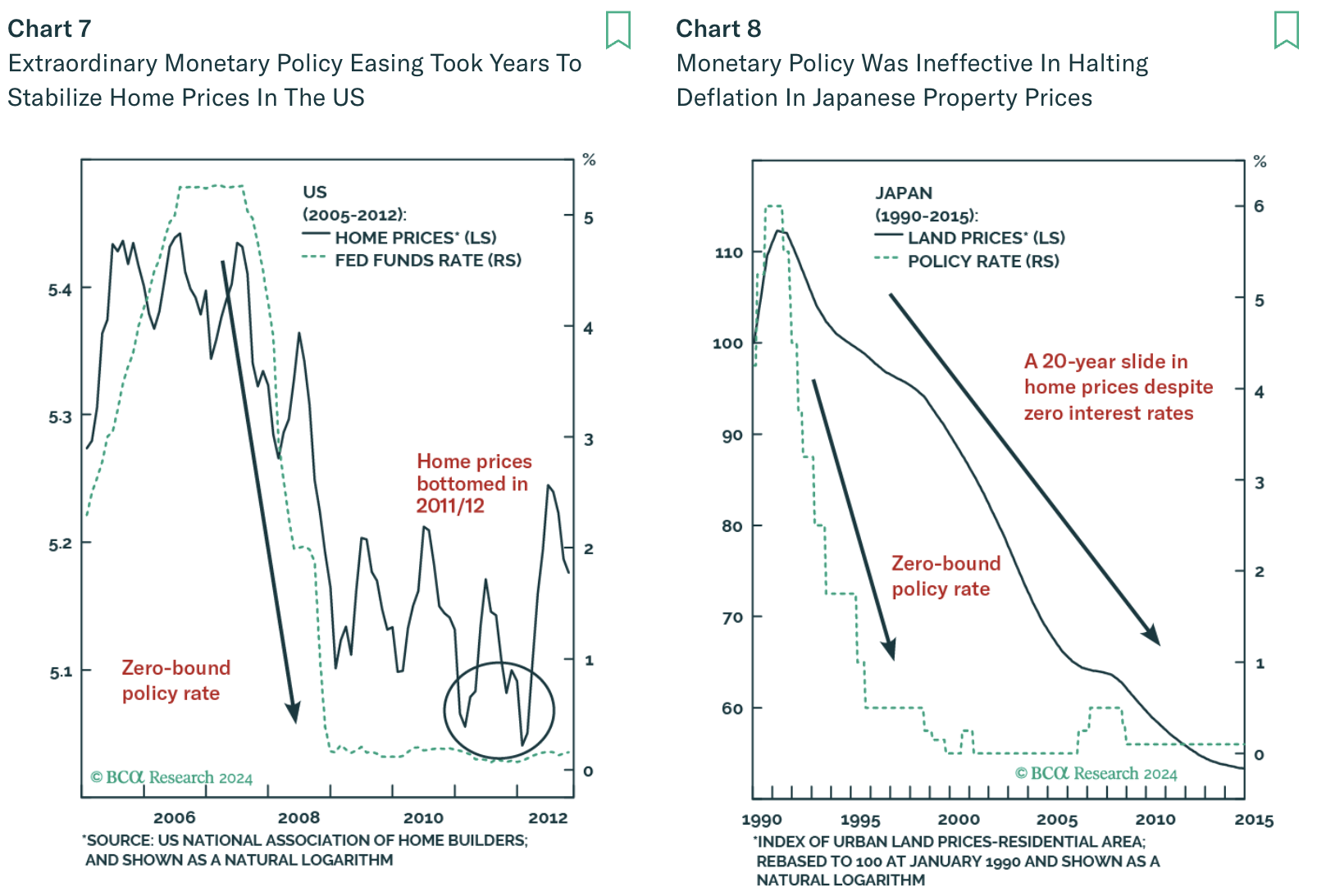

To understand the monumental changes underway in China, I must first contextualise the recent financial crises of the other three major economies: America, Japan, and the European Union (EU). Each of these entities suffered a severe financial crisis precipitated from a bursting property market bubble.

- Japan in 1989

- America in 2008

- The EU in 2011

China can now be added to the list of economies victimised by a bursting property bubble.

The Chinese central government, under President Xi Jinping’s leadership, initiated this process by restricting credit to property developers in 2020, through a policy known as the ‘Three Red Lines’.

ChatGPT explains the policy:

China’s “Three Red Lines” policy is a regulatory framework introduced in August 2020 to curb excessive borrowing among property developers and mitigate financial risks in the real estate sector. The policy sets strict thresholds on three key financial metrics: a liability-to-asset ratio (excluding advance receipts) of less than 70%, a net gearing ratio (net debt divided by equity) of less than 100%, and a cash-to-short-term debt ratio of more than one. Developers are categorised based on how many of these thresholds they breach, and their permissible debt growth is accordingly limited—those meeting all criteria can expand debt by up to 15% annually, while those breaching all three cannot increase their debt levels. By enforcing these “three red lines,” the Chinese government aims to promote financial stability by encouraging developers to deleverage and strengthen their financial positions.

China’s economy, like every other victim, subsequently entered into a liquidity trap or balance sheet recession. Private firms and households hunkered down, decreased economic activity, and saved money in order to repair their balance sheets. When credit demand falls amongst households and businesses, the standard-issue Keynesian economic medicine – i.e., running a modest fiscal deficit and lowering the price of money via central bank policy rate cuts – is ineffective. What is needed to forestall the dreaded deflation is a monetary and fiscal bazooka. The time it takes to switch into panic mode depends on a country’s culture. But make no mistake – regardless of the economic “-ism” supposedly practised, every country always comes around to injecting monetary chemotherapy.

I refer to this palliative treatment as chemotherapy because while it might cure the deflationary cancer, it ultimately kills the host. The host is the middle and lower classes, who are ravaged by asset price inflation with no discernible improvement in the real economy. And like modern oncology, this ultimately ineffective monetary chemotherapy is extremely profitable for a small cabal of financial witch doctors whose head offices are in New York, London/Paris/Frankfurt, Tokyo, and now possibly Beijing/Shanghai.

The monetary chemo is a two-pronged treatment.

First the banking system must be recapitalised using public funds. The banks’ balance sheets are always chock full of dogshit property loans. The private market will not provide any more equity capital, and that is why bank share prices collapse, indicating insolvency, which ultimately leads to bankruptcy. The government must inject fresh funds and change the accounting rules ex-post to legitimise the lies the banks tell the world about their financial health. For example, Japan allowed its banks to maintain accounting solvency by permitting property assets to be held at the cost of purchase rather than their actual current market value. After a government capital injection, banks can resume expanding their loan books, which increases the amount of broad money in an economy. As the quantity of bank credit expands, so does nominal GDP.

Second, the central bank must engage in money printing, which today is called quantitative easing (QE). This is done by purchasing government debt with printed money. With a reliable buyer of its debt at any price, the government can engage in massive stimulus programs. QE also forces reluctant savers back into the risky financial markets. As the central bank hoovers up all the safest interest-bearing government debt, savers replace their “safe” government bonds by speculating in the financial markets. There is urgency to these activities as savers rightly see the coming inflationary impact of the monetary chemotherapy. Ultimately that means buying property and stocks once again. For those without sufficient financial assets, they are just plain fucked.

The bankrupt banks are saved because the financial assets (property and stocks) underpinning their loan books rise in price. I call this reflation, and it’s the opposite of deflation. The government is able to increase stimulus because revenue is growing due to an uptick in nominal GDP, which is rising as a result of an increase in bank-directed broad money creation and the banks’ ability to issue an infinite amount of debt (which the central bank ultimately buys with printed money). For those in the financial speculation business (that means you, readers) the link between real economic performance and asset prices is severed. The stock market is no longer a forward-looking reflection of the economy, it is the economy itself. The only thing that matters is monetary policy and the pace at which the quantity of money is created. Of course, the specific government policies regarding which types of firms are earmarked to receive capital are important if you want to be a stock picker, but Bitcoin and crypto prices are affected predominantly by aggregate money supply. As long as fiat money is created, Bitcoin will soar. It doesn’t matter who the ultimate recipient is.

The rhetoric right now from financial analysts is that the announced Chinese stimulus measures are still not enough to right size the economy. That is true, but tucked inside the recent announcements are clues that China, directed by President Xi, stands ready to inject the monetary chemo to cure their deflationary cancer. That means that Bitcoin will soar on a secular basis as China reflates its banking system and property sector. Given that the Chinese property bubble was the largest in human history, the amount of yuan credit created will rival the sum of dollars printed in the US in response to COVID in 2020-2021.

To argue my point, I will step through the following:

- Why do modern governments all blow massive property bubbles?

- An analysis of the scale of the Chinese property bubble and why President Xi ultimately decided to end it.

- The clues indicating that Xi is ready to reflate the Chinese economy.

- How Chinese yuan will find its way into Bitcoin.

Social Order

Modern governments are based on broad popular support. In an age where the largest nation states and their rulers do not rely on organised religion for legitimacy, how can the state co-opt the general population to support its rule? The easiest way to remove the threat of revolution is to tie citizens’ financial net worth to the success of the regime in power.

The most important financial asset you own – or wish you owned – is your primary residence. The human body is made to survive in a very narrow temperature band. Our dwelling, at a fundamental level, is a temperature-controlled structure that allows us to maintain homeostasis. However, if you are out on the streets, you will invariably be too hot or too cold, which in extremis leads to death.

Forget about the cost of housing – assume you saved enough money to purchase a home for you and your family. Your biggest concern is, who protects your property rights? Absent a government that enjoys the ability to legally kill those who oppose its domestic rules and regulations, a private militia is required to enforce these rights. What is to stop a well-armed neighbour from claiming your land is theirs? When the state is strong and its laws respected, you need not worry about vagabonds stealing your shit. But when the state is weak, you must be ready to impart violence on those who would abrogate your property rights. Therefore, if you own property, you inherently trust the government to protect your rights. In return for their protection, you will do as they say. Ultimately that means you will not revolt, since it would cause self-inflicted financial ruin.

It is in the government’s interest to convert as many citizens as possible into property owners and thus tie their financial and physical wellbeing to the state. Because energy is expensive and is always required to build structures, the government strives to create programs that encourage private ownership of property, usually via various debt-based financing schemes. Even in a so-called communist country like China, property rights were one of the first things that were reformed, starting with Deng Xiaoping in the late 1980’s and early 1990’s.

Let me offer some praise for my alma mater. One of the best courses I took was on housing policy, taught by former US President Bill “I did not have sexual relations with that woman” Clinton’s Undersecretary of Housing. I took this class during the first half of 2008, right as the subprime housing crisis was metastasizing. We learned about the various government programs enacted to raise the home ownership rate. My main takeaway from this course was that property bubbles always require government support and financing. In the context of the US, the government encouraged home ownership in a big way starting during the Clinton years (1992 to 2000) by expanding the role of the Government Sponsored Entities (GSE) like Fanny Mae and Freddie Mac, starting with the 1992 Federal Housing Enterprises Financial Safety and Soundness Act. The GSEs are publicly listed private companies, but have the implicit backing of the federal government. They underwrite the majority of residential mortgages because they finance their loan book as if they were the federal government. As a result, Fanny and Freddie are some of the most profitable financial services companies. The banks play their part by earning risk-free profits originating the loans and then ultimately passing the risk onto the public sector’s balance sheet. Of course, given these skewed incentives, the masters of the universe took it too far – but they never would have taken these risks without a government backstop.

Huh … sounds a lot like how Local Government Vehicles are funded in pinko commie Mainland China. Chi-merica Unite!

Thank you to BCA Research, Ned Davis Research, Gavekal Research for their excellent charts on the Chinese economy.

A Property Bubble with Chinese Characteristics

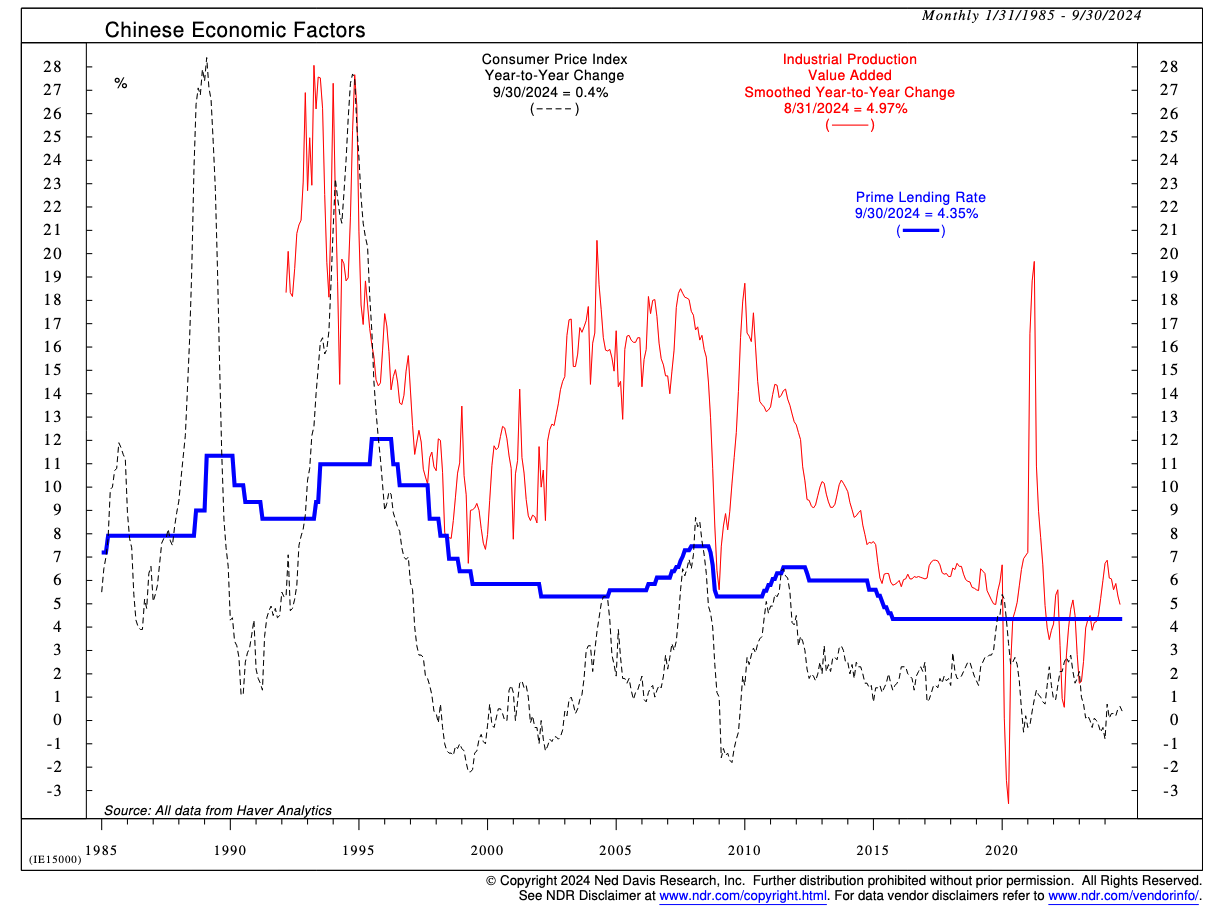

To start with, let me explain the Chinese economic model. In order to quickly industrialise, the Chinese state financially repressed savers through the State Owned (SOE) banking system to provide capital cheaply to SOE industrial firms. If the largest users of bank credit are industrial firms, a fair rate of interest for depositors is industrial value-added percentage. Industrial value-added percentage refers to the proportion of a country’s GDP that is contributed by the industrial sector, calculated by taking the value added generated by all industrial activities and dividing it by the total GDP.

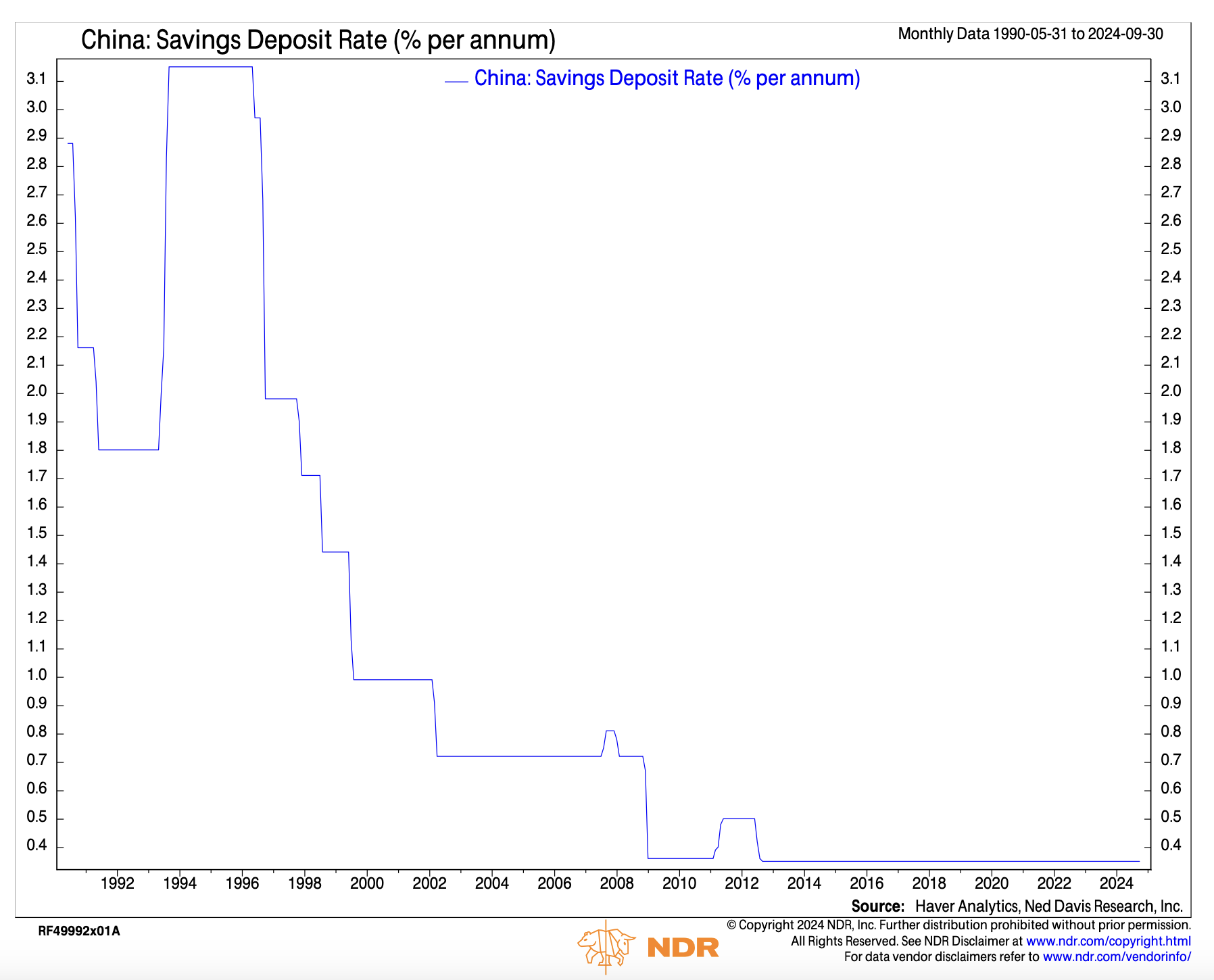

As you can see, the Prime Lending Rate is consistently lower than the Industrial Production Value Added. That is because the SOE banks pay paltry deposit rates to ordinary savers – see the chart below.

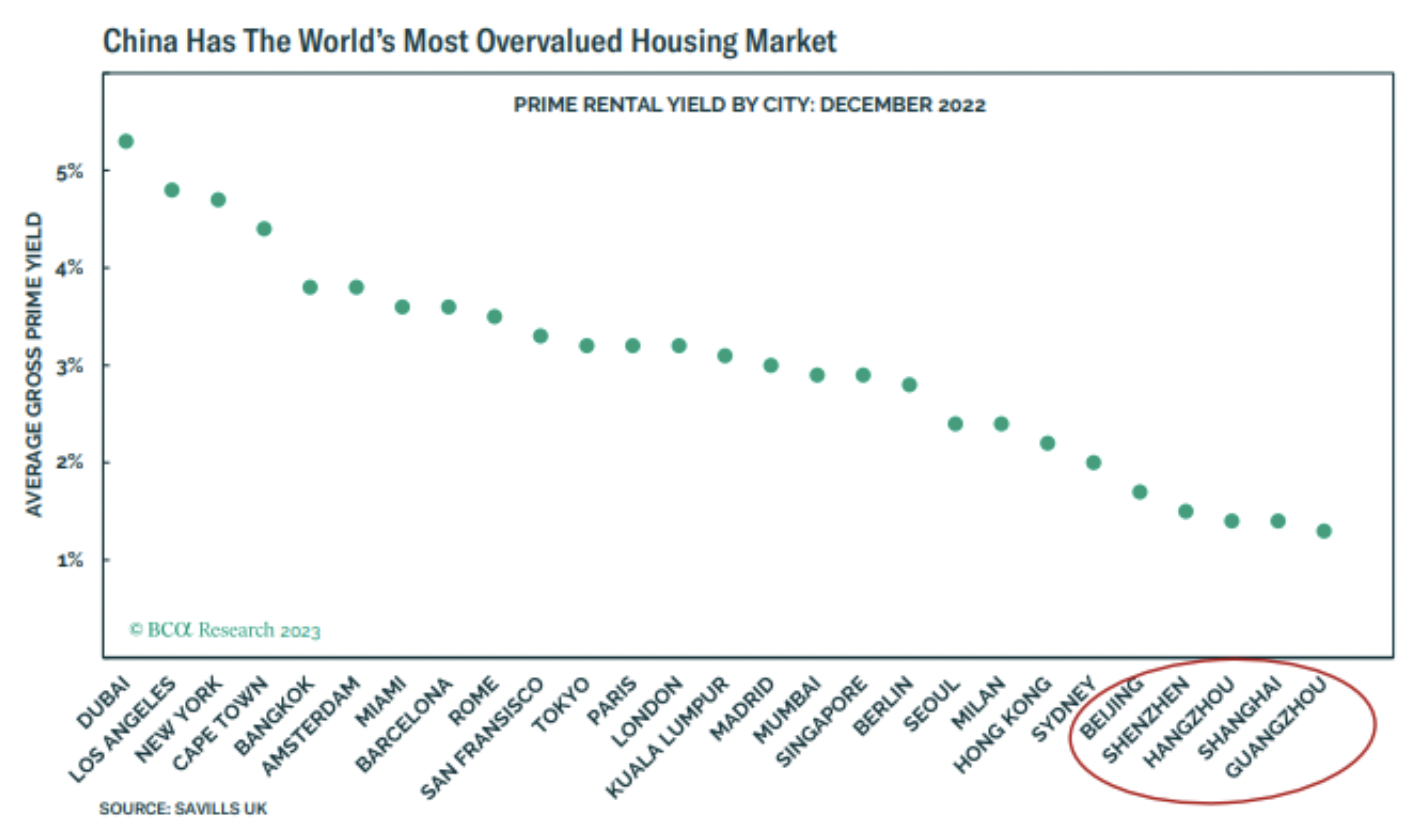

Savers recognise they are getting a raw deal, but because the Chinese yuan is a restricted currency, savers cannot invest abroad. To earn a better return on capital, they can invest in either the local stock or property markets.

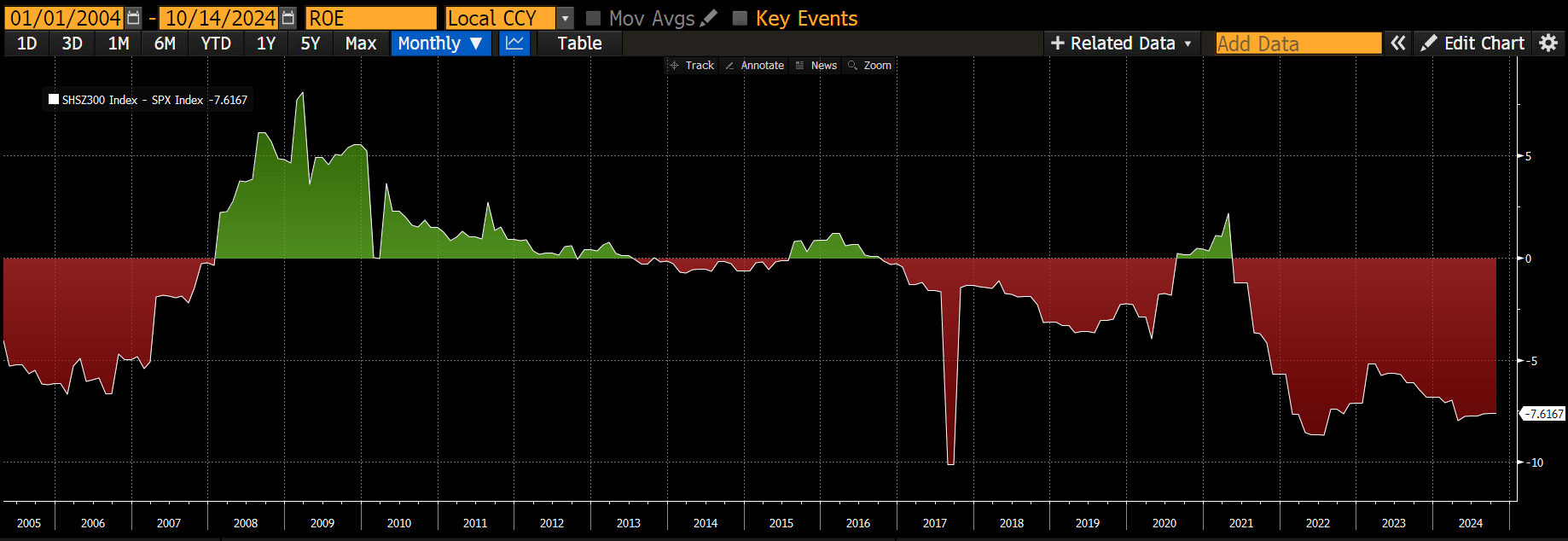

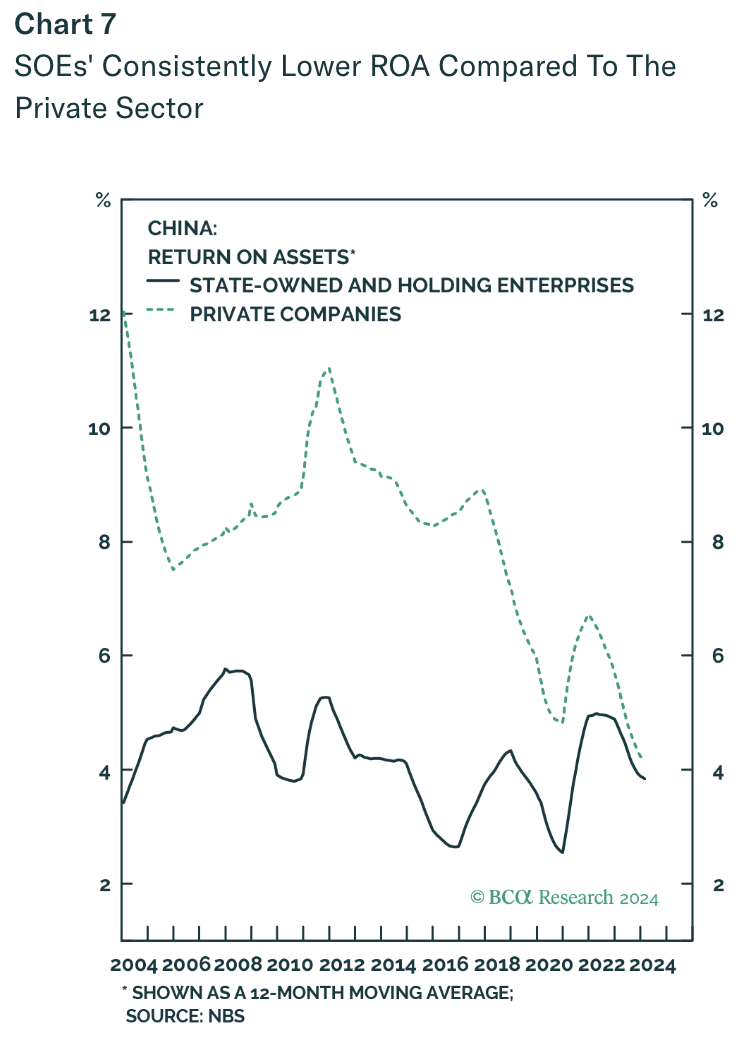

The problem with the stock market is that the best companies are SOEs. SOEs receive the cheapest bank credit and are allowed to engage in monopolistic behaviour due their exclusive licences to operate in the most lucrative industries (telecoms, oil and gas, mining etc.). You would think that means that SOE stock performance is amazing. But the return on equity (ROE) for SOEs is lacklustre. That is because all senior members of SOEs are Chinese Communist Party (CCP) members. The interests of the Party and shareholders don’t always align, and the Party’s demands take precedence.

This chart shows the CSI300 Index ROE minus that of the S&P 500 Index. As you can see, Chinese stocks perform worse than US ones.

Private firms who are subject to real competition earn a much better return than SOEs. However, SOEs are more represented in the major stock market indices.

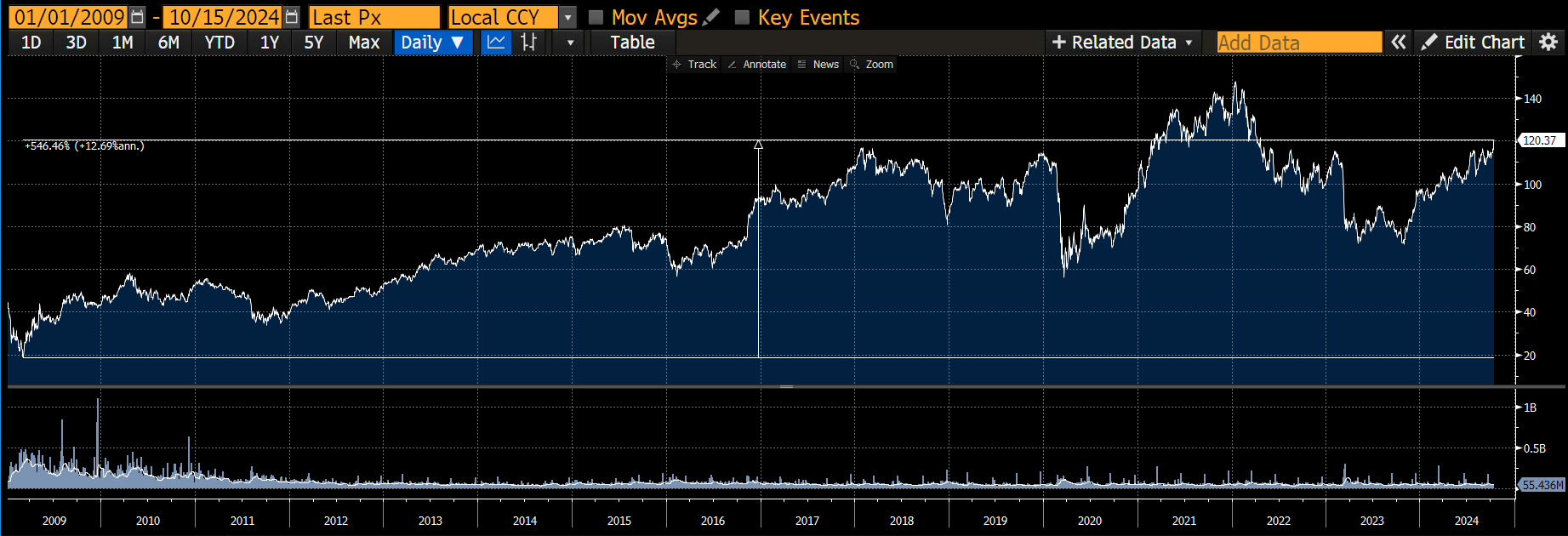

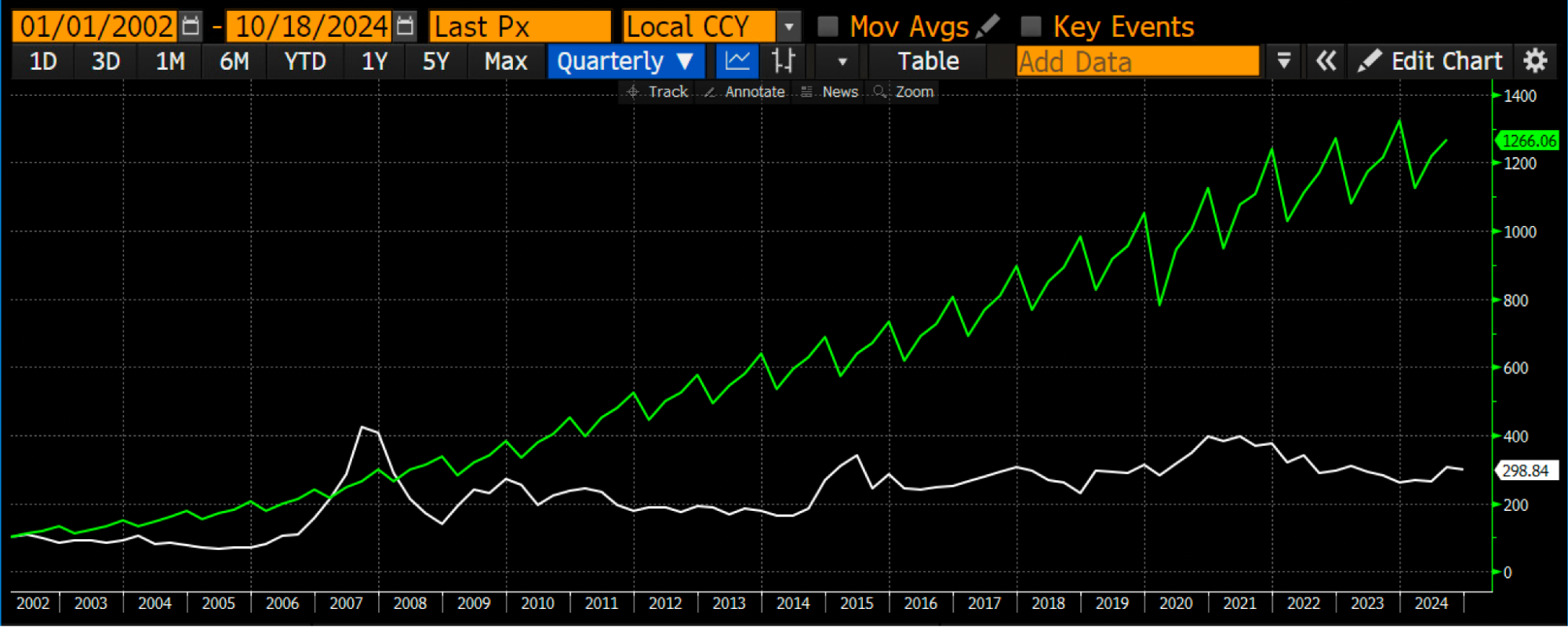

Indexed at 100, Chinese GDP (green) +1200% vs. CSI300 Index (white) +200%.

Since the stock market really got going in the early 2000s, stocks have vastly underperformed the insane growth in the Chinese economy (as you can see from the chart above). Ordinary Chinese people aren’t dumb, and therefore, stock ownership is not the preferred method to grow savings. Instead, they turn to the property market.

Chairman Mao started the process of urbanising China, and then President Deng and his more free-market friendly policies sent urbanisation into hyperdrive. The Party believes that the key to reestablishing the global primacy of 中国, China or literally “The Middle Kingdom”, can only happen through global manufacturing prowess. That means moving peasants off the farm and into the city to manufacture goods for export. As a result, every five-year plan has an urbanisation target.

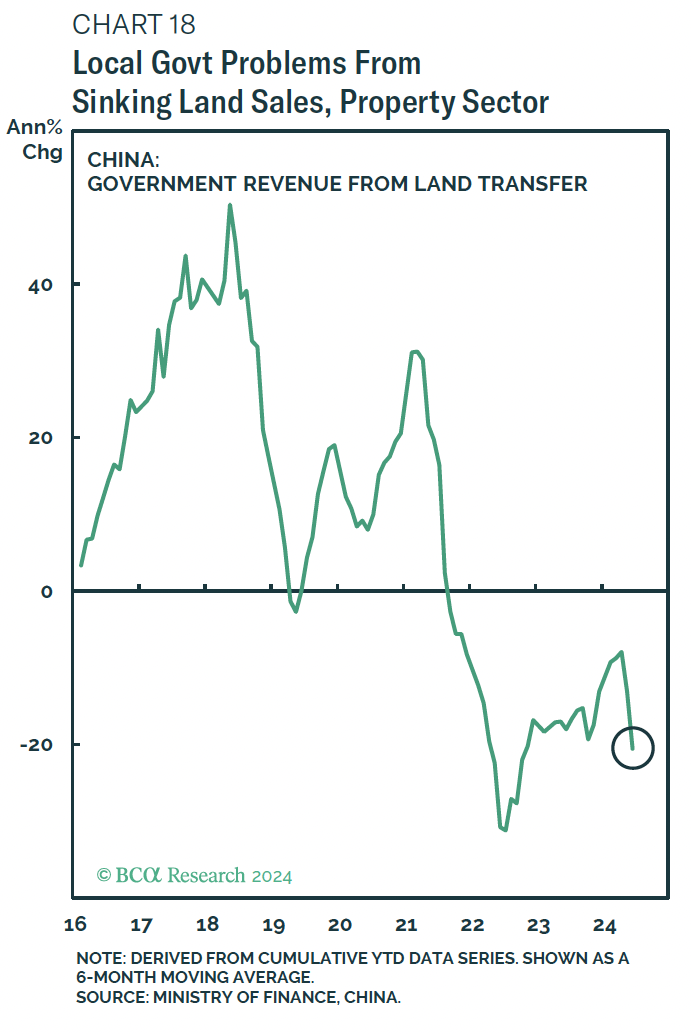

When you move hundreds of millions of people from the farm to the city in only a matter of decades, it requires an insane buildout of residential and industrial property. The first way to make money in property is to sell land to developers. The local governments own their land and sell it via lease holds to developers. Because the central government in Beijing keeps most income tax revenue for itself, local governments fund themselves primarily through land sales. As urbanisation increased alongside the growing economy, land became more valuable and sales revenue ballooned. Beijing also sets a quota for how much debt local governments can issue every year. Usually, this debt is collateralised on their land bank. Thus, the government’s finances are directly tied to rising property prices.

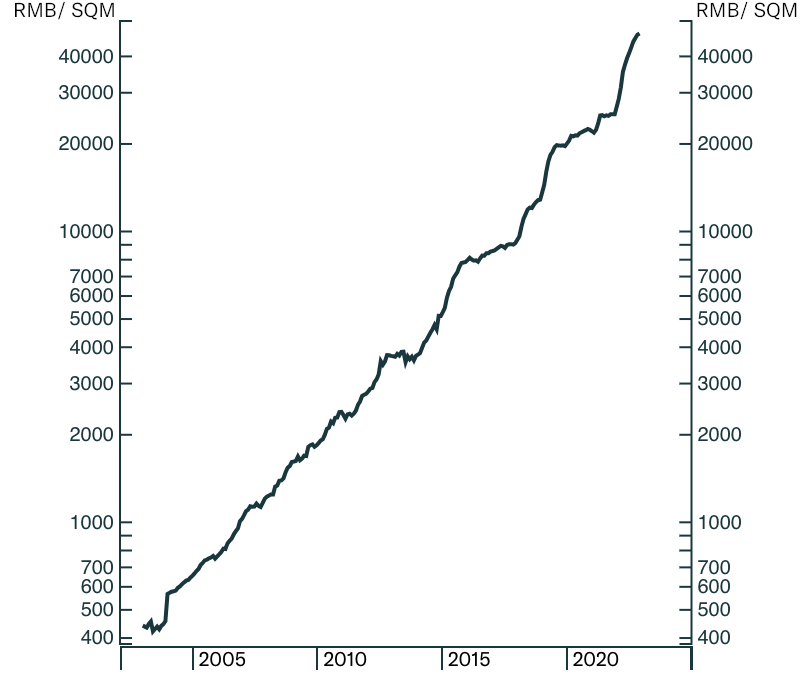

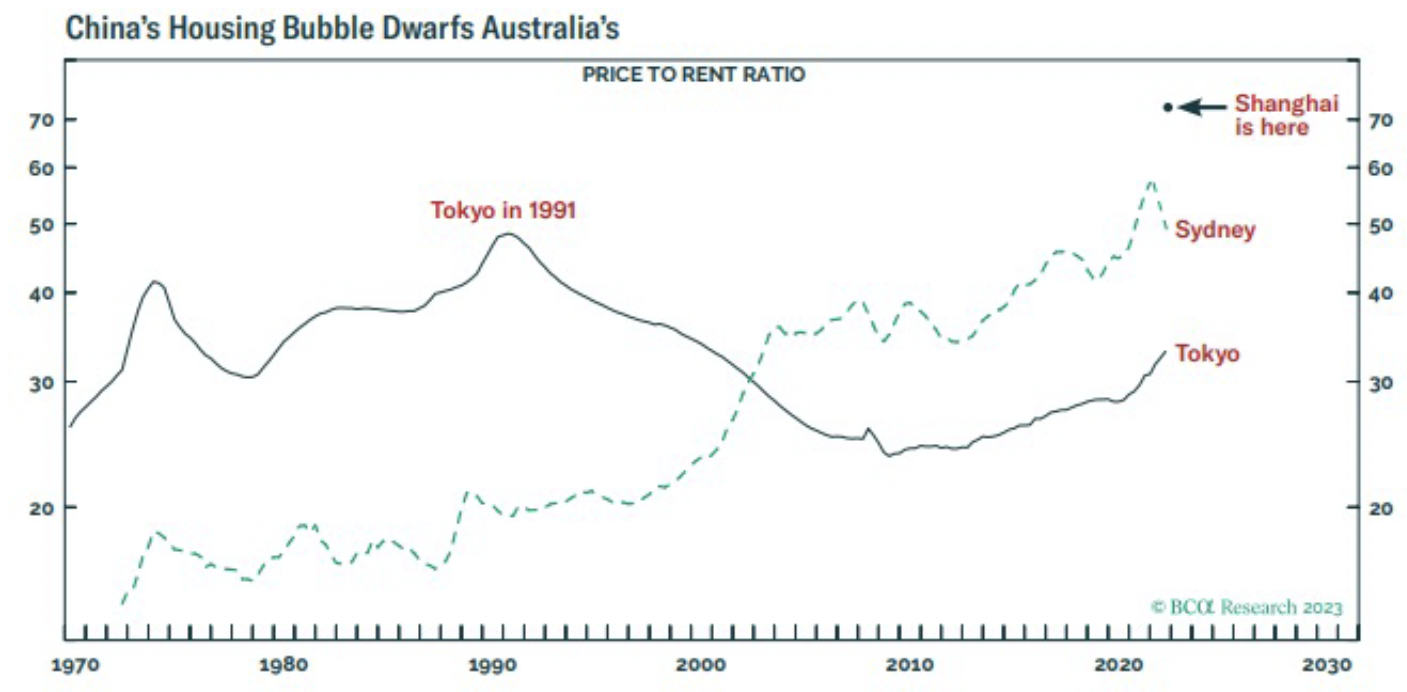

Land prices are up 80x in 19 years for a 26% CAGR.

Ordinary comrades got rich in property by saving and then buying one or more apartments. Property from the early 1990s until 2020 was up only. The banks, who normally don’t offer any type of consumer credit, were more than happy to lend against property. Ordinary household net worth is almost entirely tied to rising property prices.

All stakeholders made money as property prices rose. After the initial needs of a quickly urbanising population were met, the market continued to build apartment units because it was encouraged and the only place the banks felt safe issuing credit. A property bubble of epic proportions ensued.

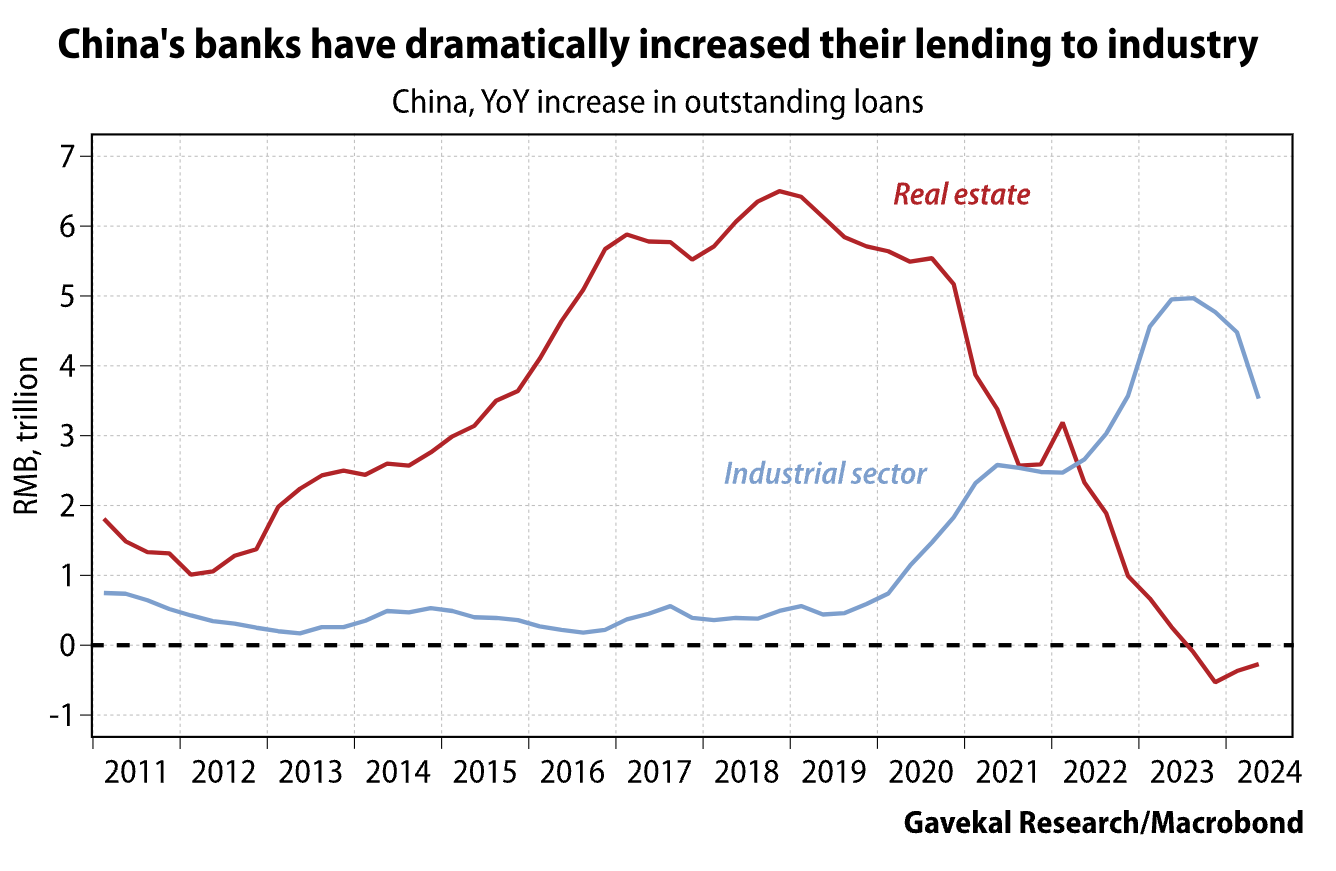

Maintaining a harmonious society is the express goal of the Party. When the vast majority of comrades cannot afford to purchase a dwelling, it tears apart the social fabric. The plummeting birthrate is one symptom of the property bubble disease. Young folks are fucking, but given the high price of real estate, the only housing they can afford is a rubber. In addition, too much bank credit was flowing into property rather than funding development of new technology. Xi Jinping redirected funding from non-productive speculative property development into high-tech manufacturing.

Beijing started to talk tough about reigning in the property market in the mid-2010s, but actually popping the bubble came with a host of risks. Every major SOE bank and industrial firm had mega exposure to the property market. The assets backing a large part of the banks’ loan books were residential property loans made to either households or developers. One of the largest end customer cohorts of firms that produced goods such as air conditioners, steel, cement, etc. were property developers. Furthermore, Beijing continued to keep most of the tax revenue for itself so that the central government balance sheet appeared strong, and that meant local governments would not be able to meet their Party imposed growth targets without land prices continuing to rise. Pricking the property bubble would decimate ordinary households, the banks, the industrial firms, and the local governments. If Beijing lost control of the market on the downside, social harmony could come undone.

Beijing started to talk tough about reigning in the property market in the mid-2010s, but actually popping the bubble came with a host of risks. Every major SOE bank and industrial firm had mega exposure to the property market. The assets backing a large part of the banks’ loan books were residential property loans made to either households or developers. One of the largest end customer cohorts of firms that produced goods such as air conditioners, steel, cement, etc. were property developers. Furthermore, Beijing continued to keep most of the tax revenue for itself so that the central government balance sheet appeared strong, and that meant local governments would not be able to meet their Party imposed growth targets without land prices continuing to rise. Pricking the property bubble would decimate ordinary households, the banks, the industrial firms, and the local governments. If Beijing lost control of the market on the downside, social harmony could come undone.

By 2020, Xi felt his control over the Party and nation was strong enough to end rampant property speculation and all its deleterious effects. In his common prosperity drive he proclaimed, “房子是用来住的,不是用来炒的 – houses are for living in, not speculation”. Then he rolled out the Three Red Lines policy. Very quickly the most over-leveraged property developers halted construction and completion of units, and defaulted on offshore bonds. Evergrande is an example of a high-profile Chinese property developer that imploded after its access to credit was curtailed.

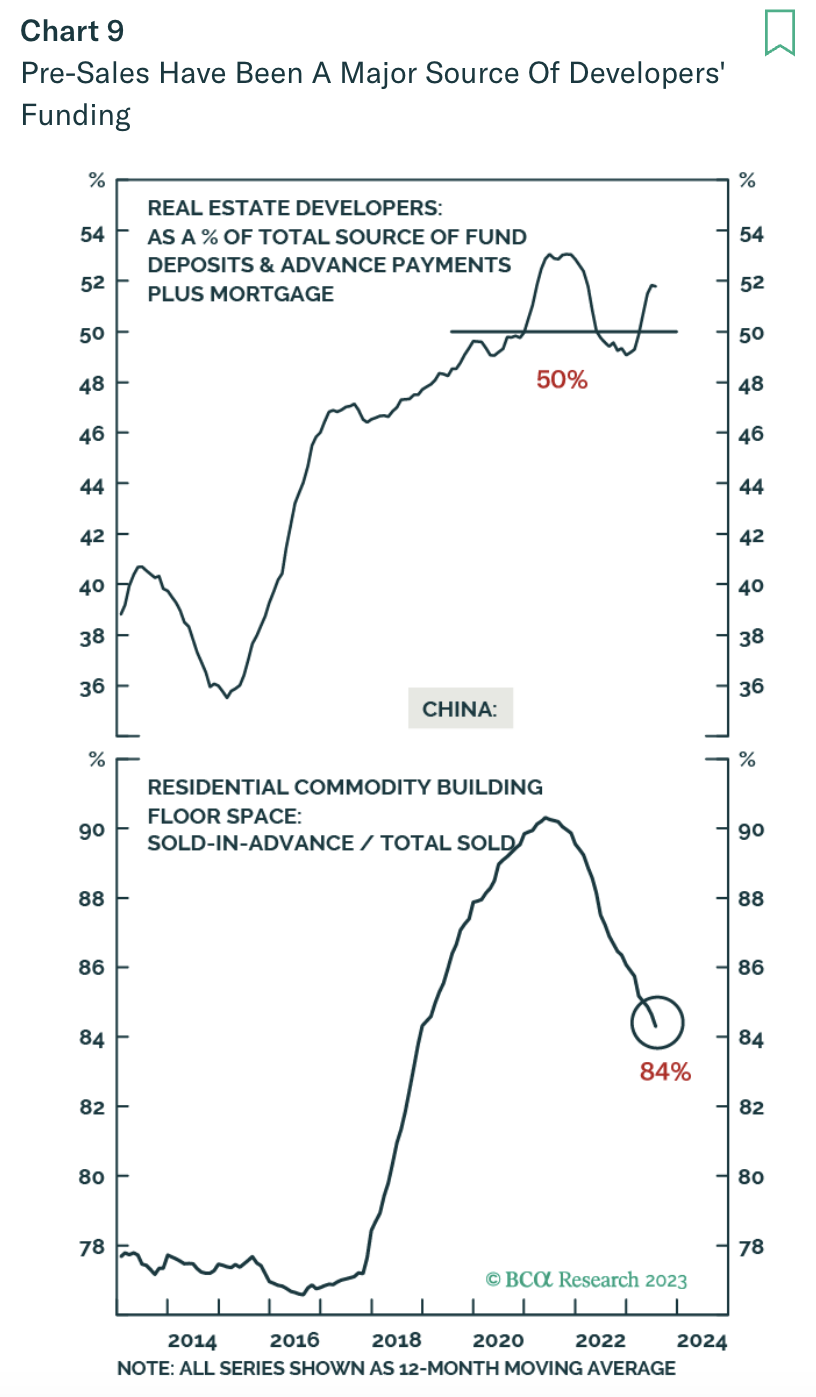

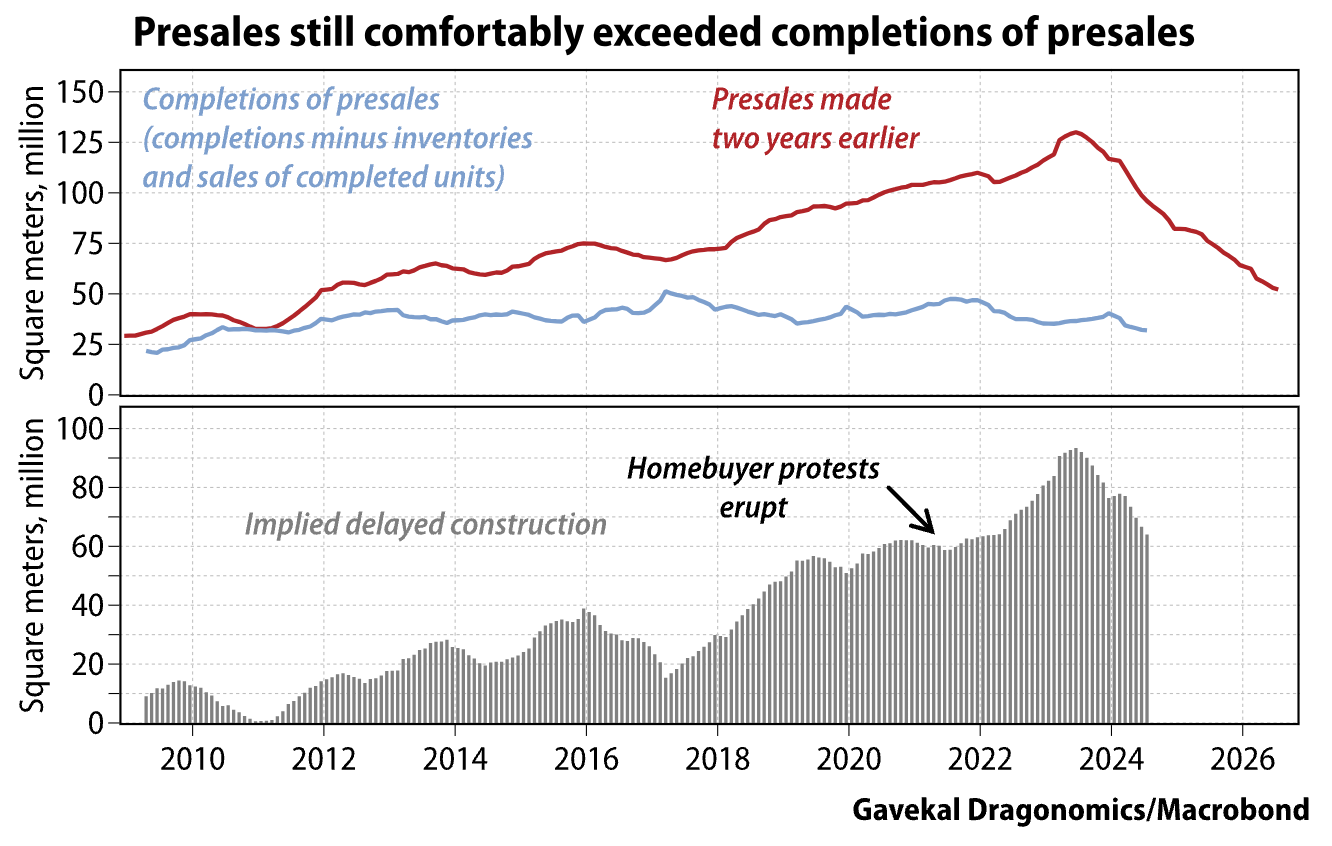

Before I move on in the timeline of the story, I want to quickly touch upon a quirk of the Chinese property market that is not well understood and its implications on what types of policy measures will succeed in ending the crisis. In China, most flats are bought off plan. You must pay a cash deposit up front, and then provide the balance after you receive a mortgage years before the property is completed. In essence, the property developer is a ponzi scheme operator. The full payments of units yet to be delivered are used to pay for the completion of older units. The property developer also uses this pre-sale cash as collateral to obtain bank credit, because they still need more capital to complete older vintage projects and buy land from the local government for new builds.

When the banks were instructed to slow down loans to highly indebted developers, it called into question whether buyers would receive their uncompleted units. If ordinary Chinese households don’t believe that the property developer will complete the unit, they won’t buy off-plan units. Without pre-sales funding, property developers are unable to complete older units. The ultimate result is the developer must stop construction, confidence in the entire property market structure collapses, and everyone loses.

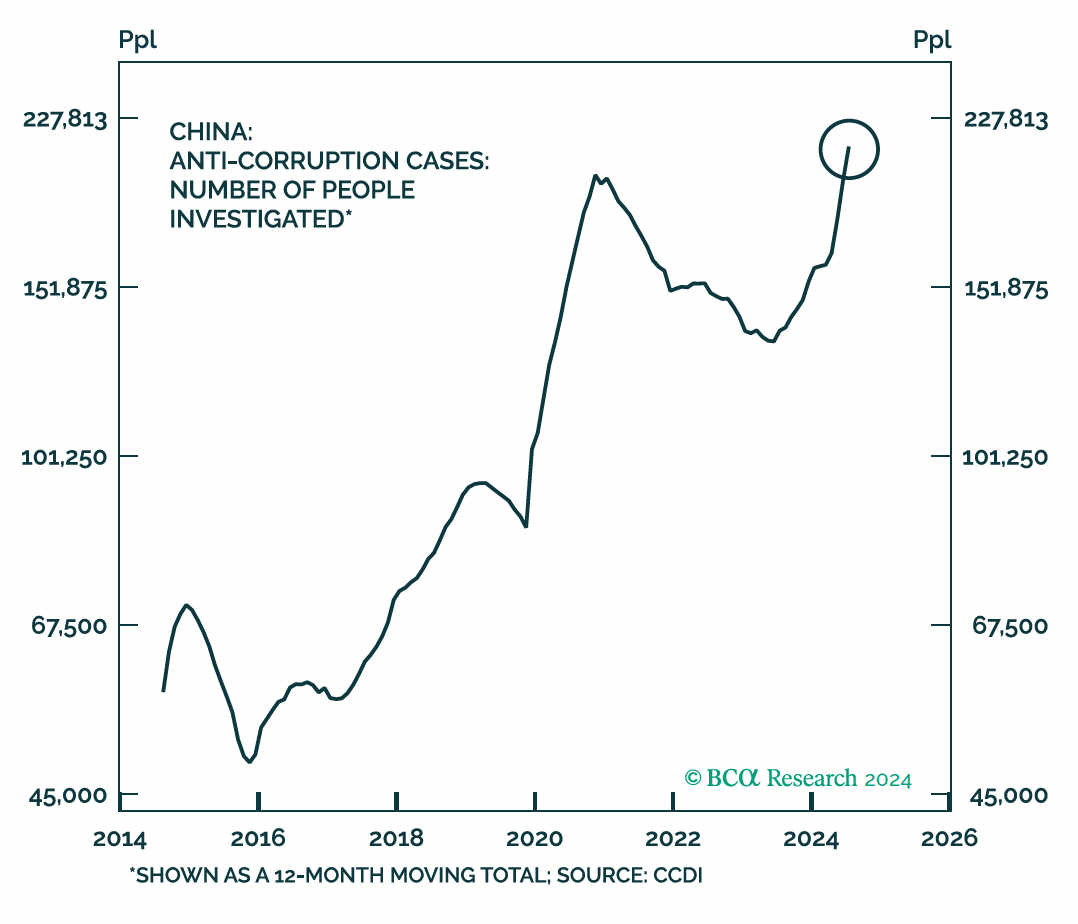

The Chinese government responded early in the crisis by instructing the banks and local governments to lend to property developers so units are completed. However, there is a massive agency problem here. While Xi and the central government is all-powerful on paper, they rely on Party members taking career risk to implement diktats.

Imagine you run a local government. You are promoted if you generate growth, but are investigated by the central corruption committee if you lose money. Being disciplined by the party for corruption infractions occasionally results in a jail or death sentence. Investigations usually come out of blue years after the supposed conduct occurred. Therefore, there is no upside to taking risk, and you sit on your hands even if the central government tells you to lend.

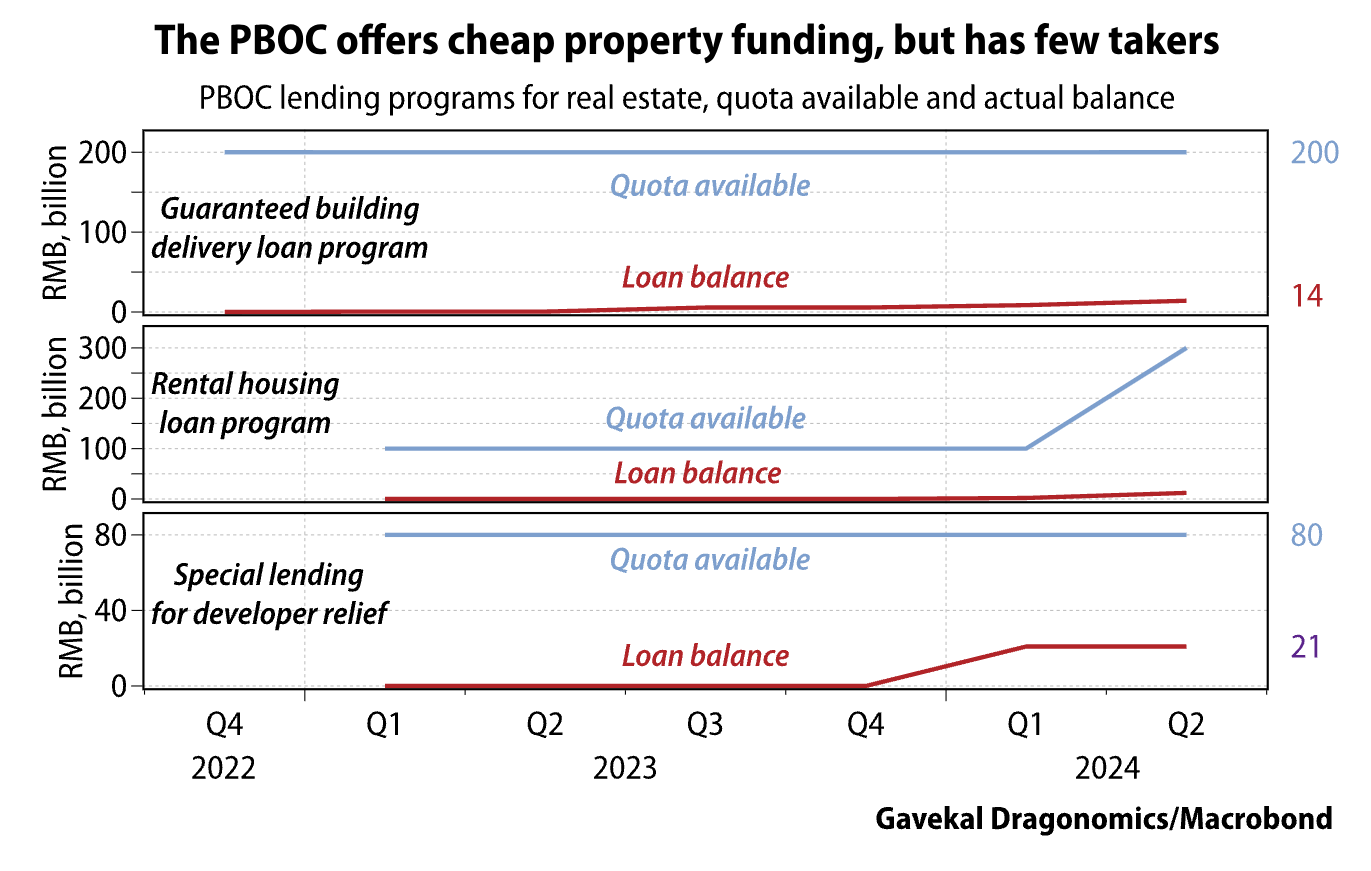

Beijing continues to issue higher quotas allowing for more property developer credit, but it is not being dispersed. The other option would be for the government – either central or local – to get into the construction game and complete the millions of unfinished units to restore confidence in the market. They have not done that yet, and I imagine it’s because such an undertaking is too complicated for a top-down centralised government given the millions of square feet that need to be completed. Furthermore, if the government got into the construction game and its units didn’t live up to the quality initially promised, angry comrades would blame Beijing rather than the defunct property developers.

That brings us to the current moment in time. Putting a bottom in under prices and restoring confidence could take decades using conventional monetary medicine.

Xi ain’t willing to wait that long because of the rapidly slowing Chinese economy. It’s time to call in the witch doctors and get on the chemo drip.

Reflation

Let’s doom scroll a bit through some depressing charts showing the impact of the bursting property bubble on the Chinese economy.

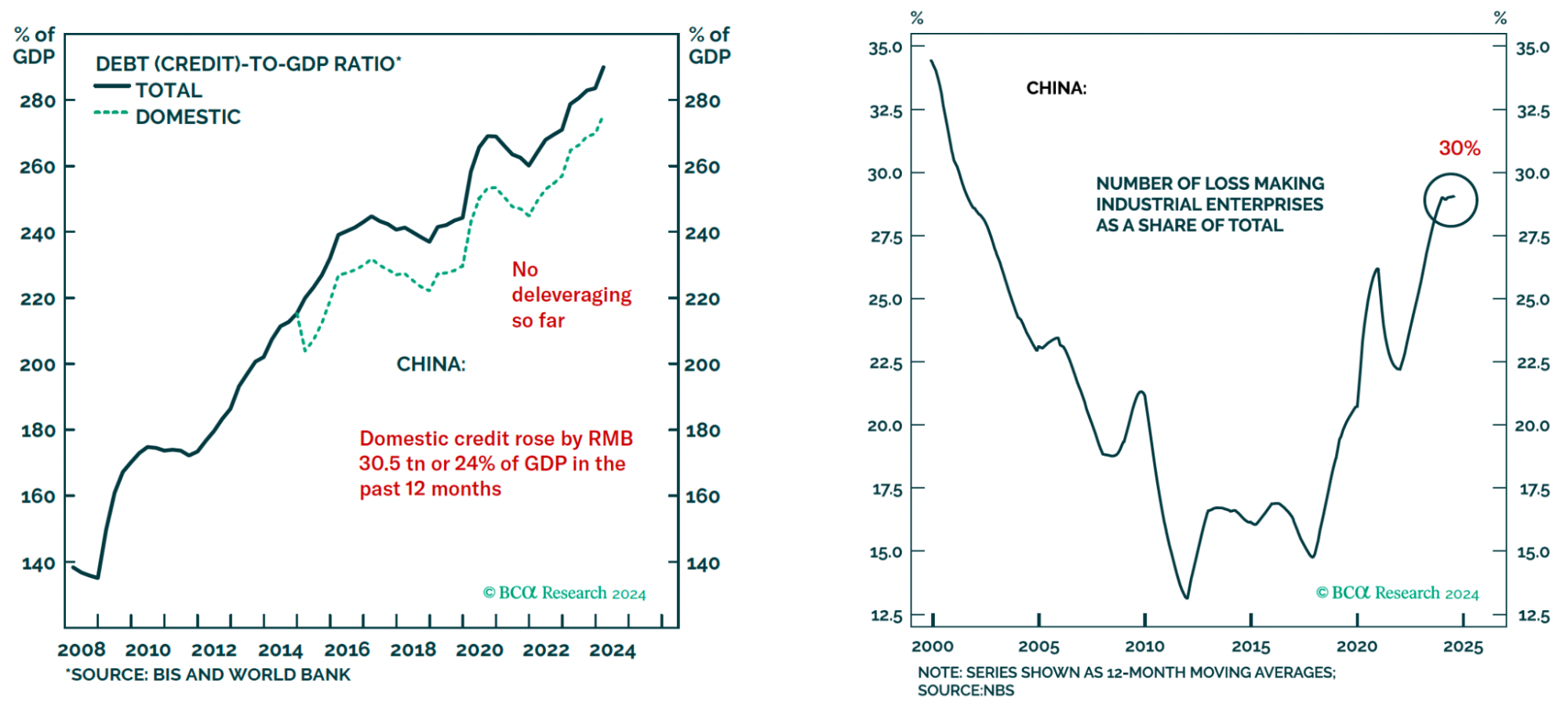

Listening to the four way economics talk about the Chinese economy might convince you Beijing has been sitting on their hands doing nothing. That is far from the case.

There has been a massive absolute amount of fiscal and monetary stimulus. But due to the massive economic overcapacity, that money is needed just to keep the lights on. Witness the rising debt-to-GDP (left chart) which is allowing zombie SOEs to tread water (right chart) and avoid mass layoffs.

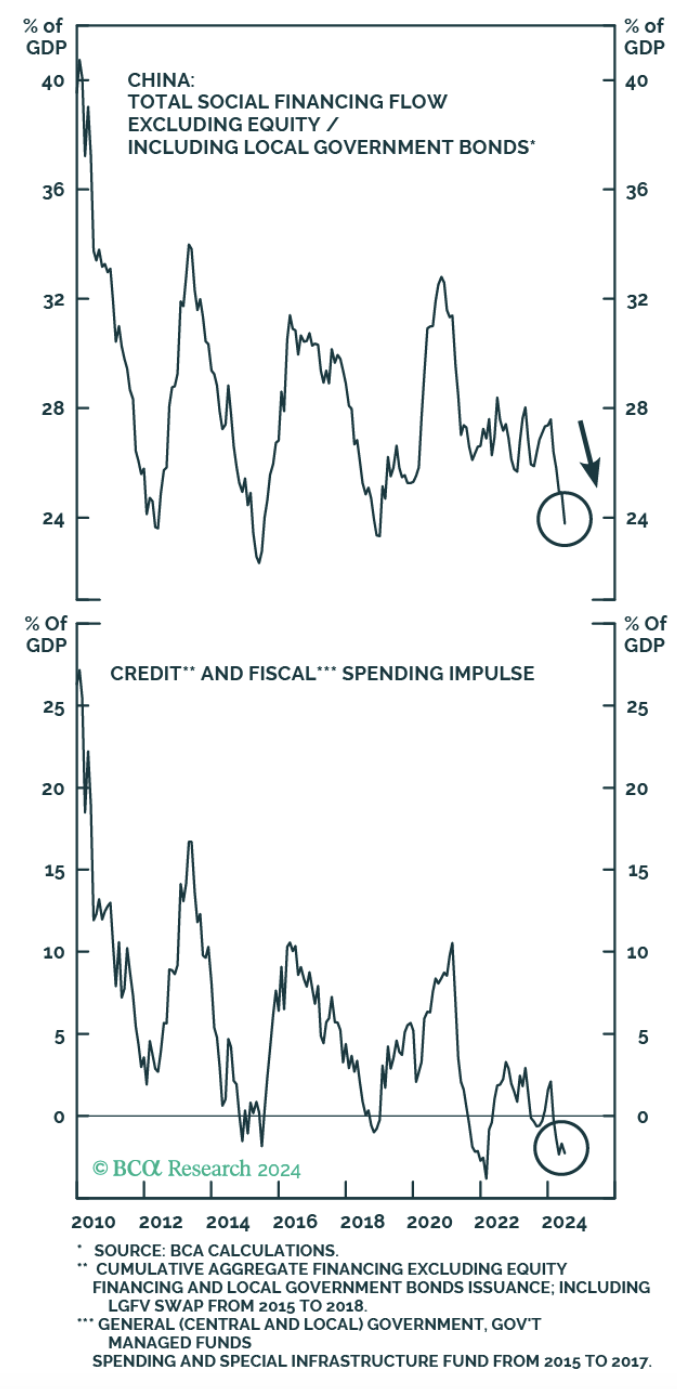

But when you just popped the largest property bubble in human history, you need that chemo to stop deflation. Everything is relative, and relative to the size of the economic black hole ripped open by the property market collapse, the current measures are not enough to generate a positive credit and/or fiscal spending impulse.

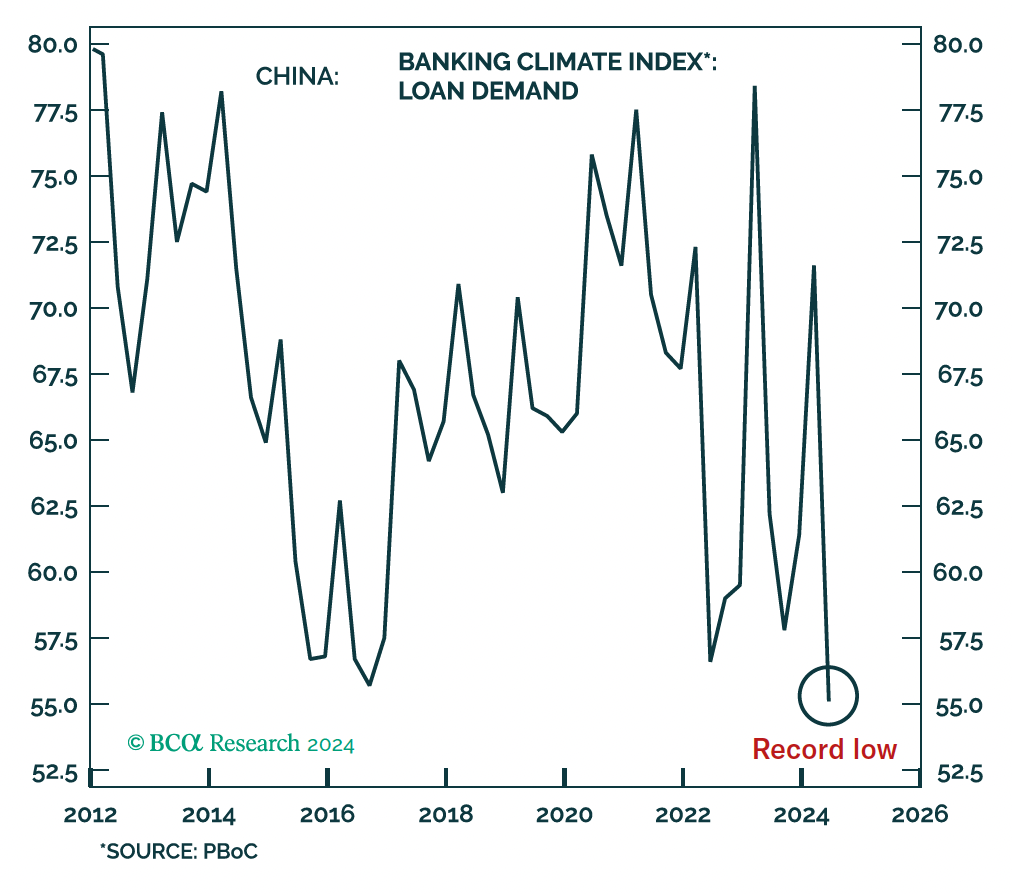

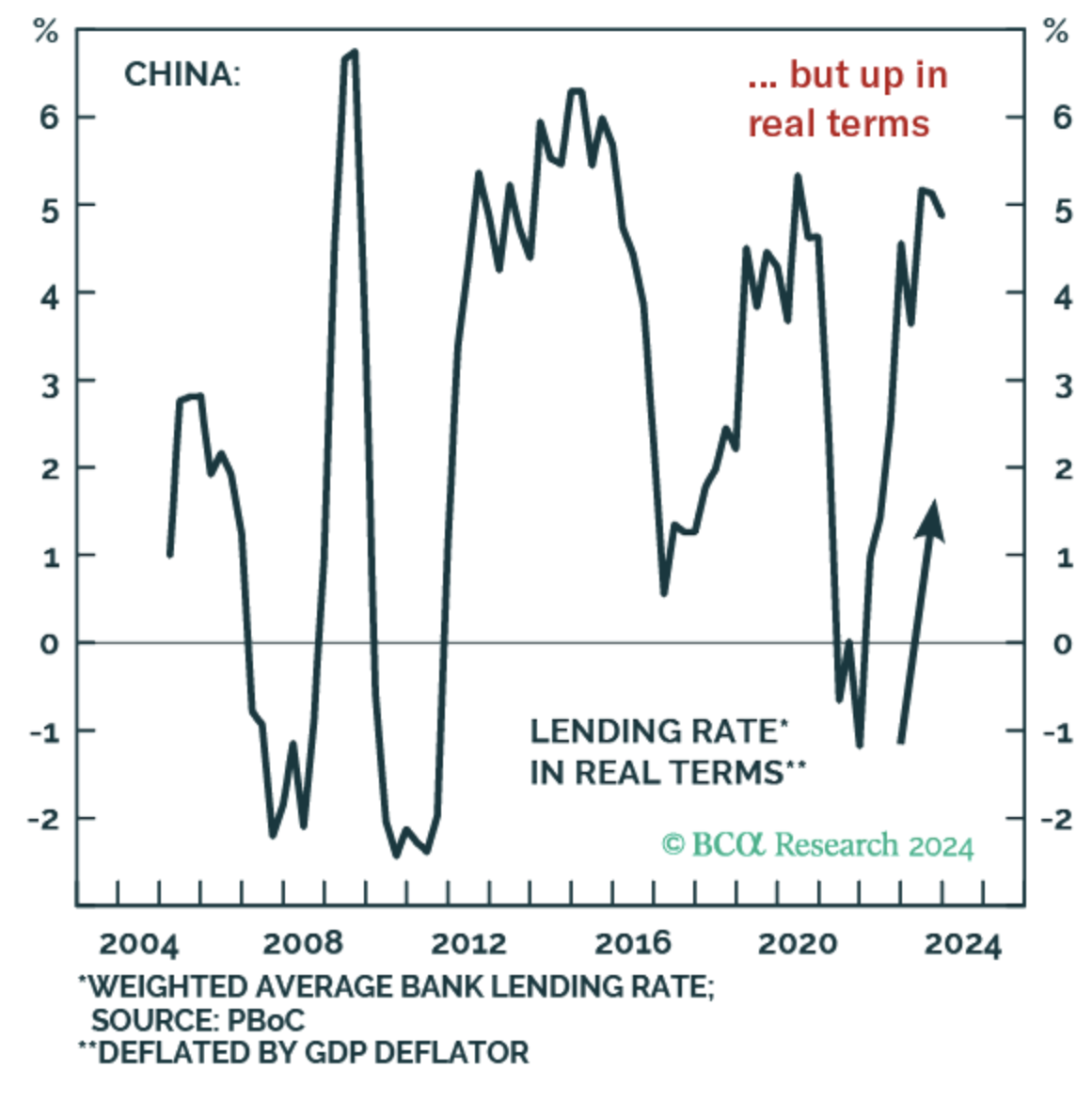

Even with all that stimulus, loan demand is at a record low. That’s because real rates are still too high.

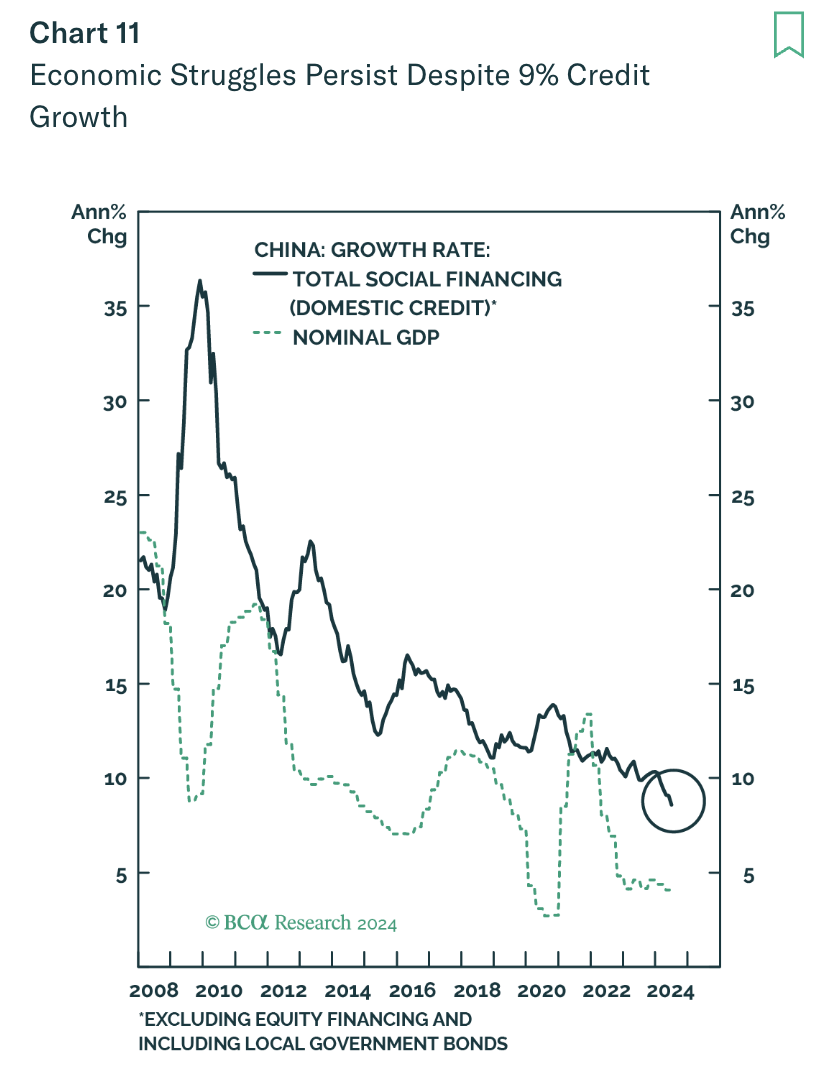

Chinese broad money growth is at the lowest it’s ever been, and as a result nominal GDP growth has slowed dramatically.

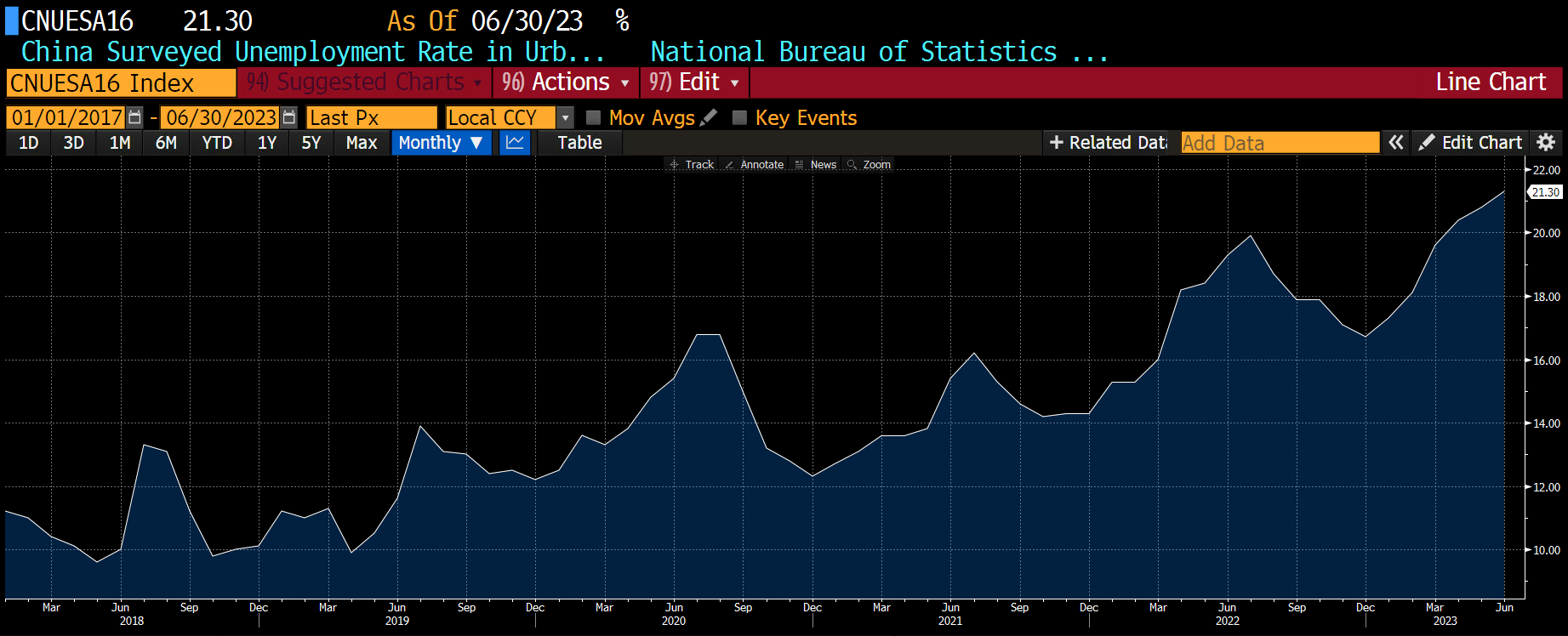

When economic activity contracts under a deflationary liquidation of excess capacity, the real problem for Beijing is aimless youths. The urban youth unemployment rate is so bad, China stopped publishing this statistic in June of last year.

A horde of young, educated, unemployed, propertyless men who cannot get laid because they are unappealing to the opposite sex is a recipe for a popular revolution. I bet the CIA is licking its chops at the prospect of fomenting a colour revolution in China. The young recent graduates have nothing to lose in opposing the regime that has failed to deliver the promised prosperity. If China were the US or EU, it would start a war with another country to send these young men off to the wartime meat grinder. But large outward military adventures are not in China’s DNA. China needs to get economic activity humming again by pursuing QE and increasing broad money growth so your average university-educated Zhou can get a job.

Xi knows what time it is, and starting this summer he instructed the People’s Bank of China (PBOC) to update its toolkit so that it could begin open market operations in the government bond market.

We will gradually include the purchase and sale of China government bonds on the secondary market in our toolkit. Recently, the market has paid more attention to this. We have been enriching and improving our methods for the injection of base money. And over a certain period in the past, the injection was passive through funds outstanding for foreign exchange. Since 2014, as such funds declined in amount, we have acted proactively to inject base money through open market operations and MLF, among other tools.

It should be noted that including China government bond buying and selling in the monetary policy toolkit does not mean quantitative easing. Instead, it is meant to be a channel for base money injection and a tool for liquidity management. The China government bond transaction, both sale and purchase, will play its role together with other tools and create a suitable liquidity environment.

China’s Current Monetary Policy Stance and Evolution of Monetary Policy Framework in the Future

QE is such a dirty word these days because the plebes know it means inflation, and that is Bad News Bears. Whatever the PBOC wants to call it, starting in August of this year, they increased their holdings of local government bonds from CNY1.5tn to CNY4.6tn. This is the first time the PBOC has printed money to buy government debt since 2007.

The only way China is going to jack the fiscal impulse to levels needed to exit this deflationary trap is massive amounts of local and central government bond issuance. Even though Chinese bond yields are the lowest they have ever been, in real terms they are still too restrictive. The price of money needs to touch zero, and the supply must increase dramatically. That can only happen if the PBOC pursues QE.

The Fed, the European Central Bank (ECB), and the Bank of Japan (BOJ) all started QE with modest amounts of government bond purchases. But they eventually got religion and printed a fuck-ton of money in order to exit the deflationary trap. China and the PBOC will do the same. Don’t let the modest initial intervention fool you – the PBOC will eventually print tens of trillions of yuan in order to right size the Chinese economy. Remember, That’s What Xi Said!

QE is coming to China, but that is only half the battle. The banks need to lend again to generate the high nominal GDP growth.

Let’s go back again to the incentives of SOE bank senior managers. They don’t want to issue lots of new loans, of which some will invariably go bad, only to get investigated for corruption a few years ex-post. They need to know Beijing has their backs.

One of the tells that bank credit growth will be encouraged by the PBOC is that in its recent spate of monetary policy measures, the Chinese government announced it would borrow money and inject this capital directly into the banking system. Given that the State owns all the banks, it’s a bit academic to borrow money to pass it from the left to the right hand. But I believe it is all about optics. Beijing is showing via its actions that there is no personal risk to bank managers if they increase loan growth.

Another tell that Beijing is ready to relax its prosecution of corruption is the resuscitation of the “three distinctions” policy. In a recent Party communique, the Politburo told party members that they would forgive mistakes of lower-level officials for actions undertaken to improve the economy. By removing the personal risk of shooting for the moon, officials can start lending money in the quantities needed to jumpstart the economy.

The financial metrics of Chinese banks as it pertains to non-performing-loans (NPL) looks a touch fugazi. According to the BIS, on average, the banking system NPL reaches ~22% after a property crisis. Chinese banks are reporting NPLs of only 2%.1 Are Chinese banks special? I think not. There is a reason why banks in China only want to lend to things directly backed by the government. To put it into a crypto perspective, imagine a bank whose loan book consisted only of loans to FTX, Three Arrows Capital, BlockFi, Genesis, and Voyager. If this bank reported the lowest NPL of any bank, would you believe them after knowing the firms it lent to all went bankrupt? In order to reinvigorate those banking animal spirits; Beijing needs to repair bank balance sheets with equity injections.

Another policy that tells me Beijing is ready to let the banks loose and enable them to issue credit far and wide is the total compensation caps placed on bankers. Due to recent government diktats, I believe the maximum total compensation for any financial services employee is US$420,000, regardless of whether they work for a SOE or private bank. When the US bailed out its banking sector it imposed no such limits; Jamie Dimon, the CEO of JP Morgan, made $17.6 million in 2009 right after his bank received a government bailout. Beijing knows that reflation is extremely profitable for the banking system, especially if the government is essentially backstopping all loans. They also know that the riches do not trickle down, and this creates anger amongst the plebes. The last thing Beijing wants is an Occupy Wall St “eat the rich” type movement to spring up on Nanjing Lu in Shanghai. This is in line with Xi’s common prosperity program.

Beijing is quietly telling the market it’s injecting monetary chemo. You just have to listen. The one side effect that many analysts cite as a reason why Beijing would stop taking its medicine is a weakening of the yuan vs. the dollar.

The CNY

Russell Napier wrote an excellent essay on why he believes China is ready and willing to inject itself with the monetary chemo I described in the last section. He also believes that Xi will tolerate a weakening yuan as a result of the dramatic increase in its supply. I don’t know if I believe Xi is ready to allow the yuan to weaken drastically, as it would bring capital flight into play. But I don’t think the yuan will depreciate that much vs. the dollar. Therefore, this prediction won’t be put to the test.

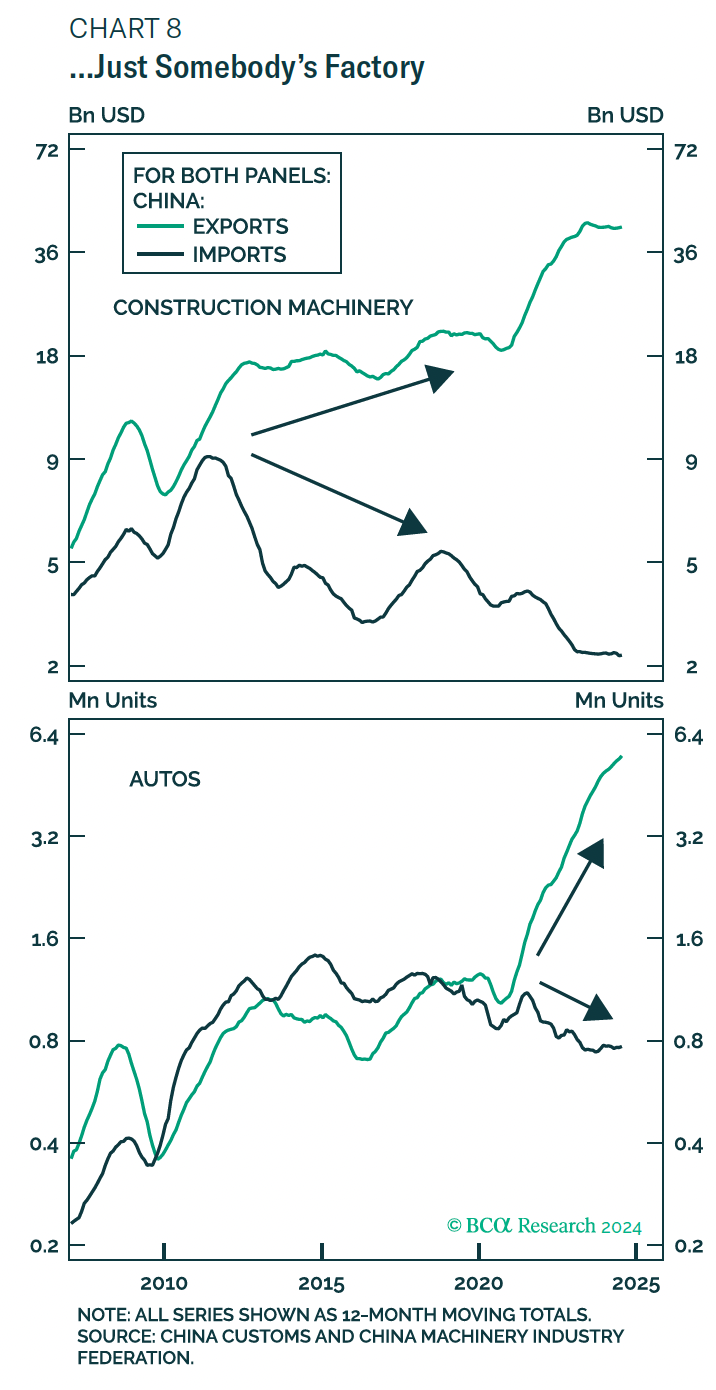

We all know that China is the workshop of the world. It follows that China’s trade surplus continues to hit new all-time highs. But when you dig through the data, China’s trade surplus (exports minus imports) is rising not because it is exporting more stuff, but rather because the import intensity of its economy is falling and China is able to pay for a greater share of imports in yuan rather than dollars.

To illustrate my hypothesis, assume that China starts with monthly exports totalling USD 100 and imports totalling USD 50; that is a trade surplus of USD 50. Now, the import intensity of its export economy falls – e.g., China used to require parts from abroad to make a car, but now most of the parts are produced domestically. This allows the trade surplus to rise, even if the volume of goods exported doesn’t grow. To make that same USD 100 worth of exports only requires USD 25 of imports. Therefore, the surplus rises to USD 75. The second way the surplus can rise is if the import volume is the same, but now half of the imports are paid for with yuan. This also reduces the import figure to USD 25, and the surplus increases to USD 75.

The above charts illustrate how China is exporting more construction machinery and autos using less imported goods.

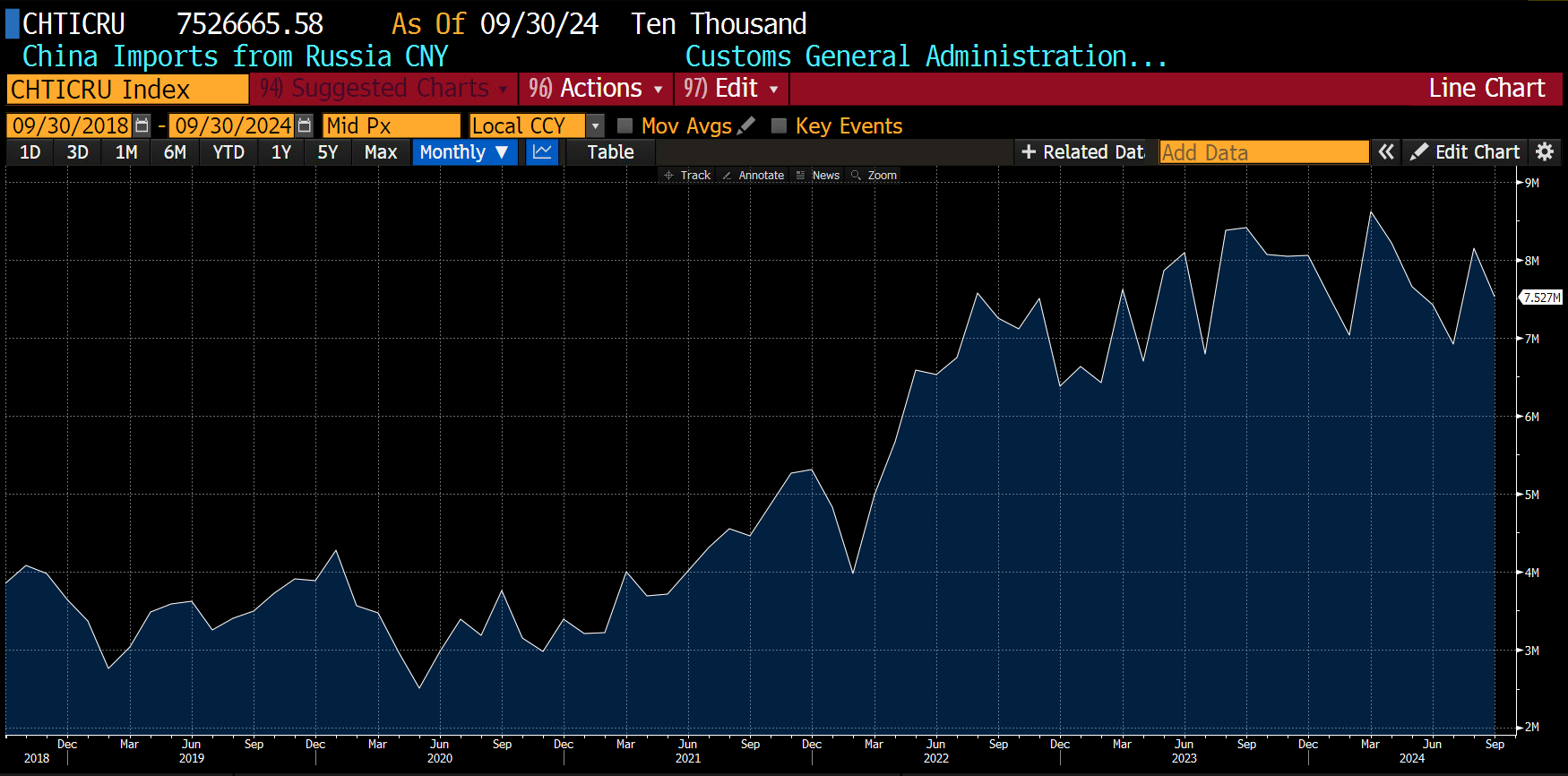

The main commodity that China lacks is energy. But now, China is able to buy commodities with yuan instead of dollars from Saudi Arabia and Russia (for example).

Before the West stole Russia’s dollars/euros and enacted sanctions post the commencement of the Ukraine War in February 2022, China would not have been able to dictate the terms of trade. But now, given no other option, Russia must pay in yuan if asked and supply energy at discounted prices to China.

As China increases the domestic supply of yuan, which in turn boosts economic growth, it will invariably increase inflation. However, given that China produces more goods domestically and pays for a greater share of energy in yuan, the rise in inflation will not lead to a dramatically weaker yuan vs. the dollars as it would have in the past.

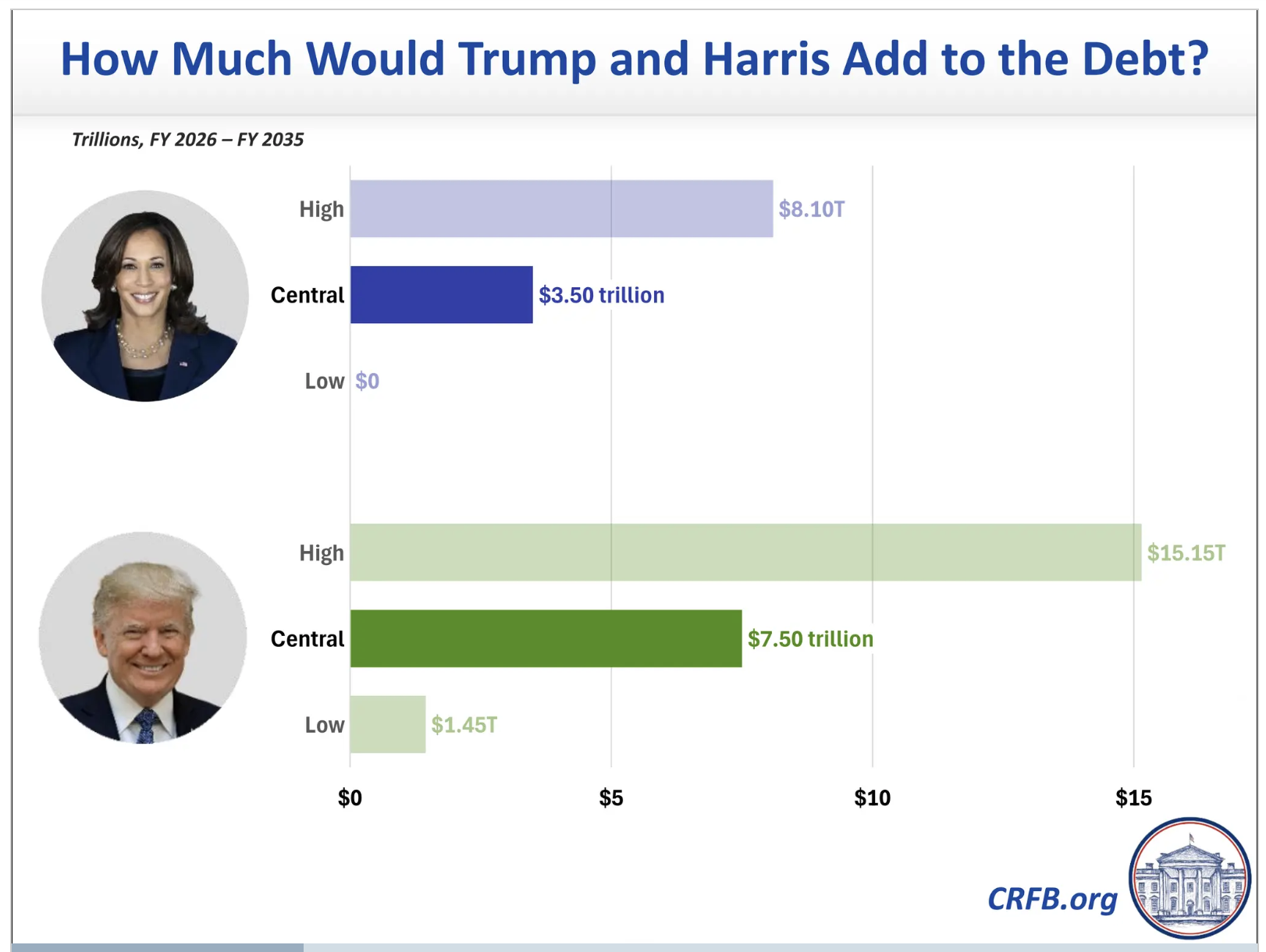

The final reason that the yuan will not dramatically weaken is that concurrent to this Chinese reflationary exercise, the US, regardless of who wins the presidential clown election, will pursue a weak dollar industrial policy. I know Trump and Harris try to draw attention to their differences, but at the core they both will print money and hand it out to key US industrial sectors.

I don’t necessarily agree that Harris would spend less than Trump, but in either case we are talking about trillions of dollars of additional fiat supply hitting the market in the coming years, regardless of who wins. This definitely will cause a structural weakening of the dollar.

The negative domestic currency side effects won’t be felt by China as it pursues this reflationary policy. All the stars are aligned for Beijing to print an insane amount of yuan. What is the antidote for the plebes who will witness a rise in credit creation that isn’t necessarily predicated on a strengthening real economy? Bitcoin 加油!

加油比特币 – Let’s Go Bitcoin

Chinese people are some of the most resourceful people on this planet. They will not allow their precious yuan savings to sit idle as Beijing encourages asset price inflation. Bitcoin is not a foreign concept to middle and high income coastal urban dwellers. While the exchanges were barred from offering a visible Bitcoin/CNY trading pair, Bitcoin and crypto still flourishes in China.

The market has gone back to its peer-2-peer (P2P) roots. Back in the day, when the big three Chinese exchanges (OKCoin (now OKX), Huobi, and BTC China) reigned supreme, funding an exchange account with yuan was always a challenge. Sometimes users could directly wire from their domestic Chinese bank account, while other times they had to go through a convoluted voucher scheme. In any case, Chinese people found a way to move yuan from their local bank account onto the exchange to trade.

Nowadays I’m told that China once again has a vibrant P2P market. All the major Asian spot exchanges like Binance, OKX, and Bybit do big business in the mainland. The exchanges operate P2P message boards where local traders assist comrades in trading crypto. It’s like a Sino-LocalBitcoins. The point is, it’s relatively trivial for a motivated Chinese person to sell yuan for crypto.

The reason why Beijing shut down the Bitcoin/CNY trading pairs – and I’m speculating here – is likely because they didn’t want a functioning smoke alarm that exposed the effects of their currency debasement monetary programs. Such an alarm might inspire investors to choose Bitcoin as a store of value over stocks or property. Given that the Chinese government knows it cannot ban Bitcoin, and Bitcoin and crypto ownership is not banned in China (contrary to what some misinformed financial media say), Beijing would rather it be out of sight and out of mind. Therefore, if my prediction is correct, I won’t have an obvious statistic to point to that clearly tracks yuan inflows into the Bitcoin ecosystem. Apart from the green dojis, I will only be able to know change is underfoot via word-of-mouth.

There will definitely not be inflows into Hong Kong-listed Bitcoin Exchange Traded Funds (ETF). If funds are flowing southbound into the Hong Kong markets through Stock Connect, they aren’t being used to buy domestic equities or property. That is why Mainland Chinese will be forbidden from purchasing Hong Kong Bitcoin ETFs. Soz to all you issuers paying for those expensive ads in the Hong Kong metro stations – Beijing ain’t going to make it that easy for comrades to get Bitcoin exposure.

While I won’t have a chart of inflows into a domestically listed Bitcoin tracker product or a Bitcoin/CNY price ticker to review, I do know that stocks and property underperform a rise in the central bank’s balance sheet.

This is a chart of Bitcoin (white), gold (gold), S&P 500 Index (green), and Case Schiller US Property Price Index (magenta) all divided by the Fed’s balance sheet indexed at 100. Bitcoin has outperformed all these other risky assets to such an extent that you can’t even differentiate the other asset returns on the right axis.

As you know, this is my favourite chart. No major risky asset class outperforms the debasement of the currency like Bitcoin does. Investors instinctively know this, and when it comes time to think about how to safeguard the purchasing power of your savings, Bitcoin will be staring back at you like the Kwisatz Haderach.

For those of you who think the market will instantly recognise the future and pump Bitcoin accordingly, I’m sorry to disappoint you. PBOC QE and a re-acceleration of banking credit growth will take time. It takes time for chemo to kill the patient. During these initial stages Chinese savers are reacting as I would expect: by buying oversold domestic equities and heavily discounted flats. It isn’t obvious to the world yet that this is the policy Xi has decided to pursue. But give it time, and the effects will be undeniable.

The fact economists are bearish on the size and scale of the stimulus so far presents a great buying opportunity. Because when the average wealthy coastal living Zhou decides they must have Bitcoin at any yuan price, the upside price volatility will harken back to August 2015, when, after a shock yuan devaluation by the PBOC, Bitcoin went from $135 to $600 – an almost 5x pump in under 3 months.

Want More? Follow the Author on Instagram and X

Access the Korean language version here: Naver

Subscribe to see the latest Events: Calendar

1This is data from a chart posted by Felix Zulauf in his 24 September 2024 Webinar.

Related

The post appeared first on Blog BitMex