(Any views expressed in the below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

For those of you who have a Bloomberg terminal, run FARBAST Index <GO>. This is the index that outputs the US Federal Reserve’s balance sheet in millions of USD updated weekly. I keep droning on about this, but this number and its trajectory is the only thing that matters. If you have confidence that the Fed’s balance sheet will rise exponentially from today’s levels, then short term wobbles in the crypto markets become immaterial.

For those of you who have a Bloomberg terminal, run FARBAST Index <GO>. This is the index that outputs the US Federal Reserve’s balance sheet in millions of USD updated weekly. I keep droning on about this, but this number and its trajectory is the only thing that matters. If you have confidence that the Fed’s balance sheet will rise exponentially from today’s levels, then short term wobbles in the crypto markets become immaterial.

To be clear, there are two things that matter to my overall bullishness on the macro cryptocurrency market cap.

-

- The US Government will begin to engage in nominal GDP targeting financed by the Fed purchasing Treasury bills, notes, and bonds. Therefore the Fed’s balance sheet will be higher than today.

- Decentralised finance (DeFi) will aggressively disintermediate many rent-seeking activities performed by centralised financial services institutions. The savings due to cheaper fees and more inclusiveness will flow to the end user and those who hold the tokens.

- The hyper growth of point 1 provides the push to accelerate point 2.

Self-perpetuation and growth are the two universal constants when evaluating the potential actions of organisms or a civilisation which is a collection of humans. Most modern societies have an underlying assumption of infinite growth. Look no further than how we price a stock.

A stock’s value is the discounted stream of all future cash flows. The terminal value assumes the company continues to exist and grow forever. That is obviously empirically false, but we plug it into our fancy model anyway. Therefore, my overarching assumption is that growth is preferred and assumed. The question is cost. There are various ways to pay for growth, and one of the most effective on a national level is nominal GDP targeting paid for with borrowed money.

To fully understand why I am so confident that the Fed’s balance sheet might be 10x higher in short order, I will compare how America dealt with the aftermath of WW2 to how it will deal with the aftermath of the world war on COVID-19. The political and economic conundrum is always, “how does a nation continue to grow after a destructive crisis?”.

This is the Crypto Trader Digest, but I spend a lot of time talking about American monetary policy instead of the fundamental merits of a decentralised monetary and financial system over the current parasitic centralised system that reigns supreme. We live in a USD world. It is plain to anyone who reads Satoshi’s whitepaper that the 2008 financial crisis and the response of all major central banks was one reason why Satoshi believed something better could be created. Therefore, an appreciation of and confidence in the trajectory of the most important financial institution globally, the US Federal Reserve, will allow any speculator to shrug off being down 30% to 50% on the day, because they know that in less than ten years the tsunami of money printing will take the crypto complex’s market cap to unimaginable levels.

Before we go back in time to 1939, check this. Due to the gargantuan US fiscal stimulus enacted to fight COVID, Federal net outlays represented 31% of 2020 GDP. That makes the US government as a stand-alone entity the 3rd largest economy as measured by 2020 GDP globally— just behind the US private sector and China. The great thing about any large centralised government is they collect a lot of statistics. You can’t manage what you don’t measure. Therefore, the richness of statistics during and after WW2 allows anyone with an internet connection to connect the dots.

Let me TL;DR this essay for the TikTok’ers; I know I probably lost you at my first sentence, but I hope by now your attention span can spare 2 minutes:

What Happened Post-WW2

-

- In order to pay for WW2, the US government borrowed money. In order to keep its cost of funds down, the Fed bought bonds in a large enough quantity to fix the price of money. The long end was fixed at no greater than 2.5%.

- As a result, the Fed’s balance sheet rose 11x from 1939 to 1946.

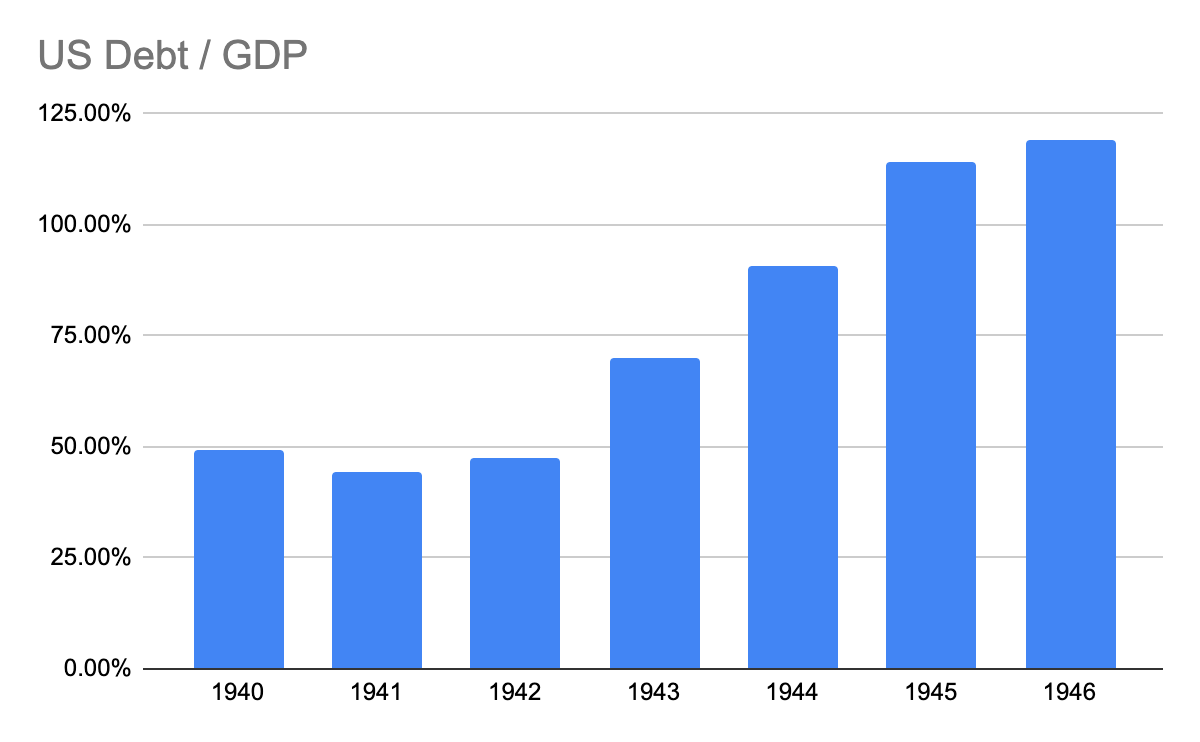

- At its peak, the US debt to GDP ratio reached 110%; in order to inflate away the debt incurred to win the war, the Fed continued fixing the price of the treasury curve until the Monetary Accord of 1951, when the Fed regained its independence from the Treasury.

- Unfortunately, the plebs were forbidden to privately own gold, so they suffered severe negative interest rates and high inflation. They had nowhere to go but government bonds and equities.

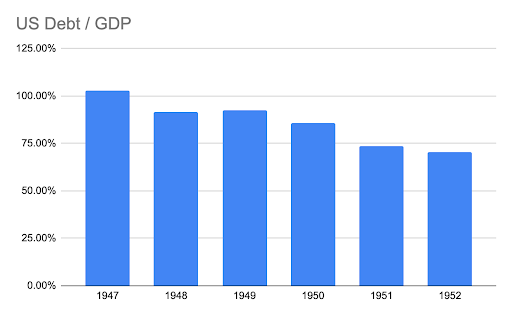

- By 1951, the US government successfully delivered its balance sheet, dropping the debt / GDP ratio from 110% to 70%. Now the Fed could allow the free market to operate once more in the US treasury market.

What is Happening Post-COVID

-

- In 2020, the war on COVID caused US GDP to drop the most since WW2.

-

In response, the USG, run by the Republicans, spent the most money in aggregate terms in US history.

- The Fed, while not engaging explicit price fixing of the treasury curve, bought 55% of all treasuries issued in 2020. This resulted in their balance sheet growing 76% in 2020.

- US debt to GDP reached an all-time high of 130% by the end of 2020.

- The Democrats were elected, and just like the Republicans, swiftly enacted a few trillion-dollar spending bills and promised to do much, much more.

- The US is now a dual deficit country; it spends more than it receives in taxes (fiscal deficit), and it imports more than it exports (negative capital account).

- US politicians in both parties are vocal that the government must aggressively expand fiscal spending to right the wrongs of the past, and ensure labour is protected in the aftermath of COVID.

- Foreigners are not waiting around to watch their $7 trillion worth of US treasuries get decimated, and on a net basis only bought 8% of treasuries issued in 2020 vs. 42% of all treasuries issued from 2002 to 2019.

- The only politically acceptable option is aggressive fiscal spending paid for by Fed money printing.

- Thankfully, in 2021 we have the crypto capital markets, which are not a target for some government agency or central bank.

- While the tens of trillions of dollars created by the Fed will not all flow into crypto, some of it will – and because crypto is unencumbered it can rise to a level that allows holders to maintain purchasing power in the face of monetary inflation.

My research assistant and I have worked diligently to create informative charts to bring life to this hypothesis. Strap in, have your drank or mug of kombucha handy, and let’s fall in love with macro-economic statistics. When you finish, I hope you have more confidence in your crypto portfolio, and maybe you buy the dip, the dip, the dip, the dip…

War = Inflation

War is a terrible thing. It’s even worse when you, as a taxpayer, have to pay for it directly. That is why governments would rather resort to the stealth tax of inflation than aggressively raise taxes to pay for war. The population might turn out to be a bit too pacifist, leading to a chorus of objections regarding the use of their tax dollars.

While certain taxes were raised to pay for America’s participation in WW2, like all governments before them and after, they chose to borrow money to pay for the war. I will draw heavily on a Federal Bank of New York staff report entitled “Managing the Treasury Yield Curve in the 1940s”, published in February 2020 (and italicized paragraphs below are sourced from this report).

When the US decided to formally enter the war after Pearl Harbor in 1941, they had to figure out how to pay for the massive expenditures needed to fight. Remember – the government spends, and the treasury pays for it by selling bonds. As always, you want to pay as little interest as possible when borrowing money. The Treasury politely requested that the Fed create excess banking reserves for the sole purpose of supporting their bond issuance.

Prior to the war:

The FOMC (Federal Open Market Committee) made no attempt to manage either the level of reserves or the level of interest rates. Open market operations were limited to maintaining an “orderly market” for Treasury securities and typically involved maturity switches rather than outright purchases or sales.

But then, the Treasury dictated the Fed help them fix the price of money because gen pop wasn’t hip to receive such low rates to help the US government finance the war effort:

The ⅜ percent bill rate did not command similarly widespread support. Prior to the first big wartime financing – the May 1942 offering of $900 million of 2½ percent 25-year bonds – Treasury officials pressed for a commitment from the Federal Open Market Committee to maintain an ample quantity of excess reserves. They wanted to be able to rely on the pressure of excess reserves to bolster demand for the bonds. [Ed. VERY IMPORTANT]

Footnote:

Marriner Eccles, the chairman of the Board of Governors, had noted several months earlier that “If substantially the present methods of financing were continued, … it would be necessary to create a large volume of excess reserves for the purpose of placing the banks under pressure to purchase Government securities.” Minutes of the Federal Open Market Committee, March 2, 1942, p.4.

Translation: The Treasury wants to borrow money too cheap. And you are dragging us, The Fed, kicking and screaming into a policy where we have to buy an unlimited amount of bonds to fix the price to where you, the Treasury, desire. The result is that our balance sheet will explode.

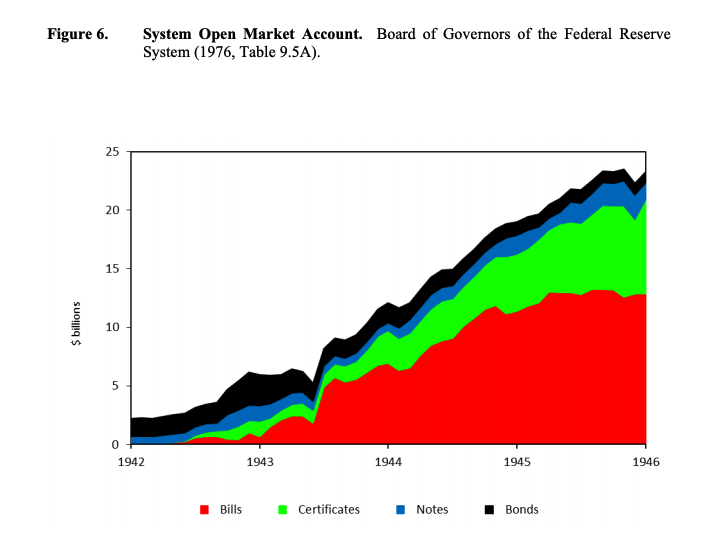

The Fed’s SOMA account balance ballooned over 10x from 1939 to 1946 as it performed its patriotic duty to fix the price of money at the behest of the Treasury. Most importantly the long bond’s rate was fixed at 2.5%.

This chart clearly shows that the general public did not want to lend to the US government at artificially depressed prices. Unfortunately, earlier in the 1930s, President Roosevelt outlawed the private ownership of gold. The traditional inflation hedge of thousands of millennia was not available.

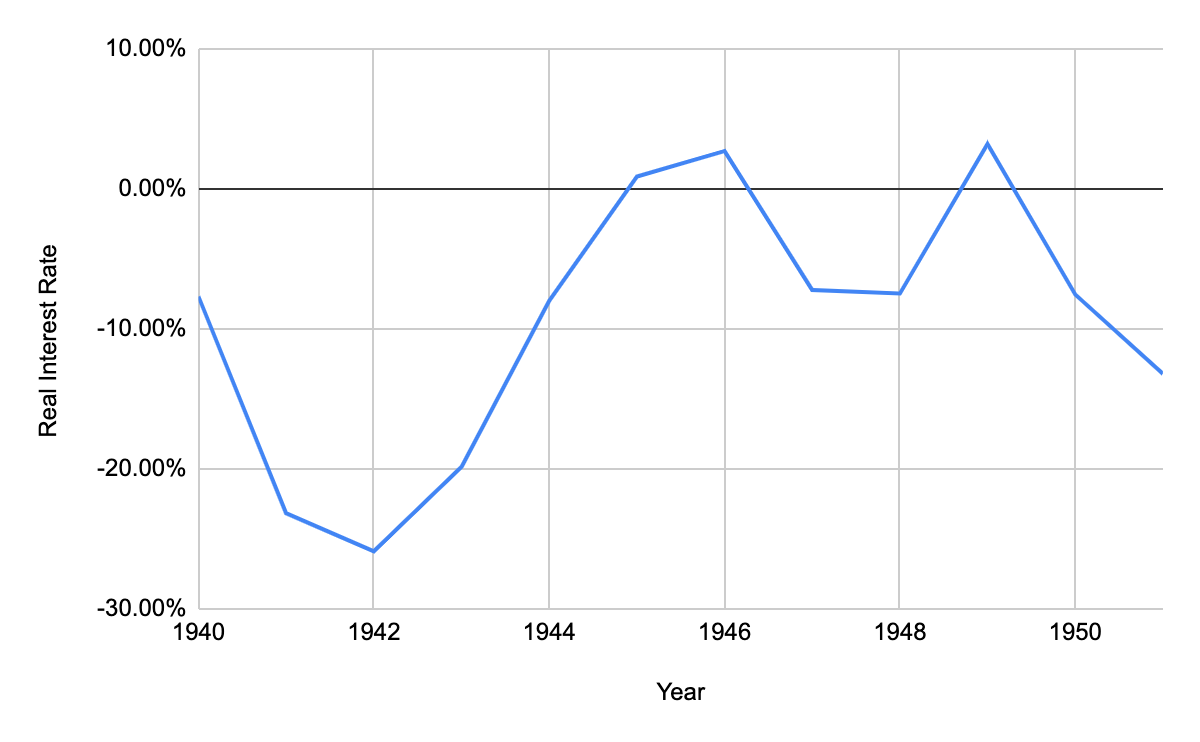

I crudely define the real interest rate as the long bond rate minus YoY nominal GDP growth. Any government can juice economic activity by printing money. If it pays a lower interest rate than the GDP growth created via debt financing, then it profits, while holders of its public debt suffer. Every single “economic miracle” of the Asian Tigers in the post-WW2 era owes its success to financially repressing savers and redirecting cheap financing to heavy industry. That is how China was able to grow so quickly from 1980 to the present. The tough part is weaning yourself off the performance enhancer of national debt.

As we can see, anyone saving money via deposits in the banking system or holding US Treasuries got eviscerated with deeply negative rates so that the US could afford war. There really wasn’t much you could do —either you put your savings in the bank or bought bonds. The equities market was still recovering from the Great Depression. From 1939 to 1951, the Dow Jones Industrial Average declined 4.6%. There was no way to escape the financial repression inflicted on savers.

This monetary inflation did bleed over into real goods and services. The CPI index nearly doubled from 1939 to 1951. Again, there was no escape.

I detest a stock to flow ratio, but it’s popular so I will STFU and use it in my analysis. The chart illustrates that America’s balance sheet was sacrificed in order to participate in the war.

Even after hostilities ended, the Fed continued to fix the price of money. The US emerged with its physical infrastructure unscathed, and rebuilt Europe. GDP growth surged. But rates did not. The result was a deleveraging of the government’s balance sheet.

The Fed finally regained its independence in 1951. They did their patriotic duty, and were then allowed to pursue an independent monetary policy.

The impasse continued until mid-February 1951, when Snyder went into the hospital and left Assistant Secretary William McChesney Martin to negotiate what has become known as the “Treasury-Federal Reserve Accord.” Late on Saturday, March 3, 1951, Treasury and Federal Reserve officials announced that they had “reached full accord with respect to debt management and monetary policies to be pursued in furthering their common purpose to assure the successful financing of the Government’s requirements and, at the same time, to minimize monetization of the public debt.” 51 Alan Meltzer (2003, p. 712) concludes that the Accord “ended ten years of inflexible [interest] rates” and was “a major achievement for the country.”

I quite love this quote:

Alan Meltzer (2003, p. 712) concludes that the Accord “ended ten years of inflexible [interest] rates” and was “a major achievement for the country.”

Translation: We artificially depressed the price of money to help the government pay for the war using a stealth inflation tax.

Luckily, America possessed the innate physical and natural capital to pursue such a blatantly inflationary monetary policy without any social upheavals. That is because America had a very robust domestic manufacturing base, could feed itself, and had the industrial commodities necessary domestically to produce real goods. Most countries that pursue similar war payment policies devolve into social chaos as the expansion of the money supply leads to crippling inflation in real goods and services. That is because most nations are not so well endowed by Mother Nature.

The United Kingdom only just paid off its WW2 debt to America in 2006. It took them almost 6 decades to fully discharge the cost of the war. It took America only 5 years – from 1946 to 195 – to significantly inflate away the cost of the war. That is the beauty of being the world’s reserve currency.

The key lessons to remember as we transition into the present are the following:

-

- To participate in a war is expensive, and governments would rather tax indirectly via inflation than directly via taxes on wages and capital.

- The central bank’s independence is a chimera. When domestic agendas require central banks to print money to cheapen borrowing costs of their government, the central bank will always follow orders.

- In order to de-lever the government’s balance sheet, the government must be able to borrow cheaper than the nominal GDP growth the expansion of debt creates.

- The release valve is the balance sheet of the central bank, because it must rise as high as needed in order to absorb the amount of government debt the public refuses to purchase at the government’s artificially depressed interest rate on offer.

- This monetary inflation will manifest itself in financial assets and real goods.

The COVID-19 Forever War

According to official statistics, approx. 600,000 Americans have died in the past two years with a cause of death attributed to COVID-19. Approx. 400,000 Americans died during WW2. All human lives are precious, but to a domestically elected politician those who die within your squiggly line domain are the most important.

COVID-19 is already more destructive in terms of lives lost than WW2. This is further proof that pandemics inflict more misery and carnage upon the human condition than war. Which is why the policy response to a pandemic can easily surpass that of a war.

The modern city is a testament to the impact of infectious disease. Running water, sewer systems, and building codes were all changed dramatically or introduced in the 19th and 20th centuries to defeat various infectious diseases that run rampant when humans live in close quarters.

US 2020 GDP declined the most since WW2, and the budget deficit enacted to fight COVID also set a post-WW2 record. All things are now possible in the name of COVID especially since the onset of the pandemic accelerated trends already in motion.

Pay to Play

Let’s first analyse how the USG paid for the massive fiscal spending enacted in 2020.

Owing to its status as the issuer of the global reserve currency, America is in a unique position vis-à-vis its funding options. The majority of trade is priced in dollars, and therefore countries that are net exporters receive dollars for their goods. Unless they want to push up the value of their currency by selling USD and buying their domestic currency, a surplus country must buy a USD-denominated financial asset. America must run an open capital account to fulfill its role as the global reserve currency issuer. Most countries don’t want to allow pesky foreigners to buy any type of financial asset, especially domestic property. This is why major economic powerhouses like China and Japan would refuse to take the mantle of the reserve currency issuer if it were on offer. They are perfectly happy with closed or semi-closed capital markets.

Traditionally, due to their liquidity and perceived risk-free nature, surplus countries recycled their exporting revenue into US treasuries. The US Treasury publishes monthly Treasury International Capital (TIC) Data. It details in aggregate who holds which types of USD financial assets.

From 2002 to 2019, foreigners purchased 42% of all net US Treasury issuance. The Fed purchased 13%. At the margin, the purchases by foreigners helped the USG finance its budget deficit at reasonable interest rates.

That all changed in 2020. COVID destroyed global trade and laid bare the ineffectiveness and underinvestment in public health globally. Governments around the world are scrambling to figure out how to pay for shutting down their economies to halt virus transmission, securing PPE and vaccine supplies, and upgrades to their public health system. They need all the money they can beg, borrow, or print.

Unfortunately, most countries cannot be as generous with the expansion of government spending as America. If countries level up their fiscal spending by printing money, it will likely trash their currency and lead to commodity price inflation (followed by social unrest). If the plebs don’t get their bread, you won’t have a head.

The “America First” mantra comes in different flavours but both Democrats and Republicans promote it. There is a general consensus that policies that help wage earners, like onshoring manufacturing, infrastructure spending, and import tariffs, are the right thing to do for the first time in 50 years. Unfortunately, these policies are inflationary, and if you are a holder of US paper you are shaking in your Virgin Galactic space boots.

I did a quick and dirty estimation of the amount of interest rate risk held by foreign holders of US treasuries. SIFMA provides a table that breaks down the US Treasury issuance by maturity. I looked at the current composition of the outstanding treasuries and used those ratios to compute an estimated portfolio of foreign holders. I then used the <DURA> function on Bloomberg to calculate the modified duration of each type of note or bond. A Treasury Note has a maturity of between 2 and 10 years. This also includes Floating Rate Notes. A Treasury Bond is anything over 10 years, which is 20 and 30-year bonds and TIPS.

I calculated a weighted average duration of 17.08 years for foreign holders.

Dollar Value of One Basis Point (DV01) = USD Face Value * Duration * 0.0001

DV01 = 6.461 USD Trillion * 17.08 * 0.0001 = $12.08 billion

That number might not mean much, but it’s a fucking enormous amount of interest rate risk. If interest rates rise by 1% or 100 basis points, I very loosely estimate foreigners will have mark to market losses of $1.208 trillion. Given that the notional as of March 2021 was $6.461 trillion, a 100 basis point rise in interest rates results in close to a 20% loss. Can I get a NEGATIVE CONVEXITY!!!

Remember, if you are long bonds, you are short interest rates. Rising interest rates are bad news bears for bond holders.

If you are a large foreign holder of US treasuries and the government tells you that it prefers a policy of inflation to support its domestic middle class, you run for the exits. That is why in 2020, when the USG made it rain, foreigners went on strike and only purchased 8.39% of issued treasuries. Who made up the difference?

This whodunnit is quite easy. What happened in 1939 when the Treasury needed a sucker to buy bonds that were too expensive? They called the “independent” central bank and told them to step the fuck up. In 2020 the Treasury didn’t even have to ask – the Fed purchased 55% of all treasuries issued. This is why the Fed’s balance sheet grew 76% in 2020.

Don’t forget about the foreign bond bag holders. We will come back to their predicament later when we talk about policy options for the USG for the rest of the decade.

There are a few technicalities that help the Fed maintain the narrative that it’s not just running a money printer to pay for the government’s bills:

-

- The Fed has not set an explicit target for government bond yields. It appears they prefer an orderly, non-volatile rise in yields to some level that we don’t know yet. Because they haven’t set a target, they can say with a straight face they are not engaged in Yield Curve Control (YCC). That is important because, remember what Governor Eccles said earlier – if the Fed is doing YCC their balance sheet will expand to whatever level is necessary to keep yields at or below their target. As the balance sheet expands, so does the money supply, and that creates the environment for inflation.

- The Fed’s liabilities are not legal tender. In English, the Fed doesn’t just print money and spend it directly from their account. Instead, they engage in a little game of ring around the primary dealer desk. The Treasury has a treasury auction, the primary dealers bid on bonds, and the Fed immediately buys the bonds from the dealers at a small markup. Everybody wins. The USG gets their wampum, the banks get paid to take zero risk, and the Fed gets to claim they are not directly financing the government.

2020 was a blow-out year. Crypto went to the moon and is currently reeling under the awesome effects of Earth’s gravitational pull. Are we done yet? Will the Fed’s balance sheet continue to rise taking all types of financial assets with it? Let’s peer into Pepe’s crystal ball.

Taper Tantrum

Monetary inflation is only a problem when it manifests in politically unacceptable ways. The prices that concern politicians the most are the price for labour (wages), and the price of food and energy.

The USG kinda shut down the economy when COVID-19 hit and sent out cheques for everyone’s troubles – 1, 2, buckle my shoe, 3, 4 out the door to punt stonks on Robinhood with stimmie cheques. The minimum wage in most states when you add up all the various government cheques is now $15 to $20 per hour, whereas pre-COVID many states had statutory minimum wage below $10.

Businesses are now complaining that the generosity of the government prevents them from hiring enough workers. Stimmie cheques absolutely prevent businesses from hiring workers at the old low wage level, but the solution is to pay more. After 50 years of losing out to capital, labour isn’t going to accept anything other than continuing real wage growth. There is an election coming up in 2022, red or blue, if you don’t hand out the goodies, someone else will run on a Made-in-America, pro-Union, high-wage platform and trounce the pro-business candidate who would rather prioritise capital returns. The zeitgeist has changed.

The fact that memes on social media are poking fun at the ridiculous prices paid for lumber in America tells you that inflation is here, and more importantly, people know it’s here.

As a result of wage and raw materials inflation, there is a part of the establishment hooting and hollering that the Fed needs to slow down and raise interest rates, or at the very least reduce the pace of its balance sheet growth. It doesn’t help that the April Consumer Price Index (CPI) print was the highest in decades. CPI is a government calculated index that is supposed to measure inflation in the real economy. If the Fed cares about fighting inflation, then all the signs are there – and now they need to change course.

At the same time, The White House is having trouble getting crucial votes in the Senate to approve the next multi-trillion-dollar infrastructure deal that comes with tax hikes. It appears that the urgency of the COVID pandemic waned enough for the usual partisan politics to re-appear.

Two things need to happen for the Fed’s balance sheet to continue growing:

-

- The USG needs to continue spending aggressively.

- The Fed needs to buy the majority of the bonds issued so that interest rates remain at affordable levels for the USG.

It appears that both of those conditions are being questioned by policymakers. That is no bueno for my investment thesis. Now, I will explain why this Taper Tantrum will fade and the USG and the Fed will get back to business as usual – with the USG swiping the Fed’s USD credit card and providing the fiscal goodies necessary.

Risks of a Declining Fed Balance Sheet

Foreign Bag Holders

Remember those foreign treasury holders who decided to purchase 80% fewer newly issued Treasuries? What can they do with their dollars?

The Bloomberg-compiled US GDP Economic Forecast for 2021 stands at 6.50%. If that comes to pass, it will be the fastest growth since the early 1980’s. While politicians prefer supply chains to be on-shored, this doesn’t happen overnight.

![[Source: The World Bank]](https://blog.bitmex.com/wp-content/uploads/2021/05/EIGHT.png)

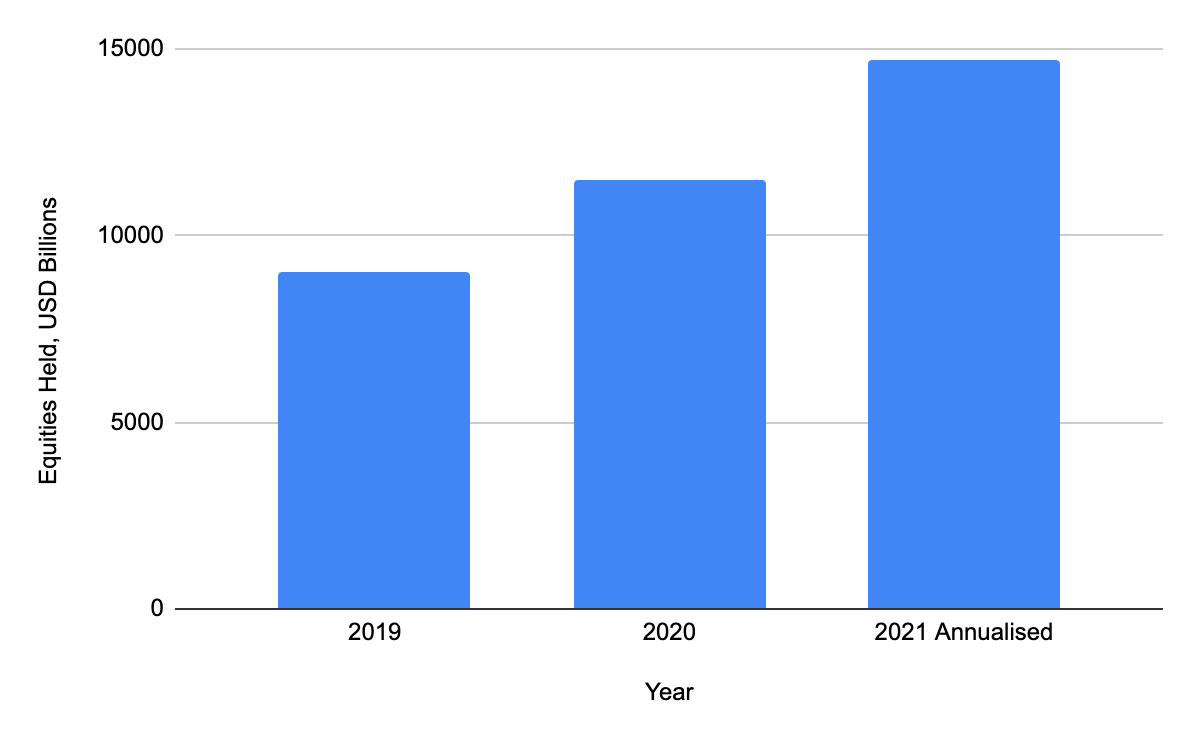

China, Germany, and Japan are going to earn beaucoup USD by producing knick-knacks for the American consumer, who is binge spending courtesy of their stimmie cheques. Japan and China are also the number one and two largest holders of US Treasuries, respectively. They earn the most amount of dollars, and therefore hold the most amount of US Treasuries.

In order to stand still on their stock of Treasuries, they’ll need to buy a different set of USD assets that aren’t being explicitly devalued via inflationary government policies. The US stock market, and specifically, the post-COVID behaviour beneficiary tech stonks blew the doors off in 2020. Instead of buying bonds, foreigners got smart and went into equities bigly.

In 2020, foreigners purchased $2.454 trillion worth of stonks. That’s approx. 57% of the amount of US Treasuries issued. Using the January to March 2021 data and a straight-line extrapolation, in 2021 foreigners are on track to purchase another $3.224 trillion worth of stonks.

Instead of recycling their export income into Treasuries, foreigners bought stock instead – which benefits from low interest rates and an expanding Fed balance sheet. Foreigners still hold $7.07 trillion worth of Treasuries.

Interest rate number go up is bad juju for long bond and equity holders. Should the Fed even hint that it will bring forward the date at which it raises short term rates, and/or reduces the monthly purchases of bonds two things will happen. One, the equity market will tank as foreigners dump stocks. The fastest human in the world is a Fed governor backtracking their policy if the S&P 500 goes down 20%. Two, Treasury yields will scream higher. And let’s put scream higher into context – a 100 basis point increase in rates is enough to tattoo the word REKT on all financial ASSet classes.

The Almighty USG

Every regime implicitly or explicitly promises its subjects something in return for their support. The architects of the modern US kinda-sorta welfare state were Presidents FDR and LBJ.

If the population saves, it doesn’t spend. The primary big lumpy expenses that modern governments attempt to smooth out / outright pay for are primarily healthcare-related. While US healthcare is not completely free, the US does provide free or heavily subsidised care for the young, old, and poor. The most important cohort to politicians is ageing workers. The Boomers are the largest and wealthiest cohort in America. Old rich people vote. Therefore, if you are a politician you always support things they care about. Old rich people care about healthcare.

As they grew into productive adults, the Boomers were promised affordable / almost free healthcare as they aged (Medicare). In addition, they were promised a dignified retirement paid for by Social Security.

In return, they spent most of what they earned in pursuit of the American dream. A McMansion filled with knick-knacks, a pantry stocked full of cheap processed food, and a two-car garage with a pick-up truck and SUV filled with cheap gas. This is how the American consumer powers 60% to 70% of annual GDP. Contrast this with China, which does not provide healthcare nor guaranteed retirement income for most comrades. The population saves aggressively, and it’s one reason why Chinese consumers only account for 30% to 40% of annual GDP.

The USG spending line items of Medicare, Medicaid, and Social Security are together called entitlements. The population feels they are entitled to healthcare and retirement paid for by the government. Any politician that attempts to reform these “third-rails” faces electrocution at the ballot box.

Defence spending almost never declines because being the world’s policemen is expensive. Especially when the goal is to ensure cheap energy commodities produced in socially unstable regions make their way to America all day, every day.

The problem with entitlements and defence spending is that these are real, not monetary goods. No matter how hard the Fed tries, it can’t print more nurses, hospitals, or aircraft carriers. As the population gets progressively sicker and older, the already expensive healthcare system will phase shift into another universe of expensiveness.

Check this – according to the US Census Bureau, from 2010 to 2019, the 65 and older population increased 7.74%. Over the same period, Medicare and Social Security expenses grew 48.52%. For each 1% increase in old folks, their expense to the government grew 6%. Over the next decade, approx. 42 million individuals aged 55 – 64 will become 65 and above. Assuming no one dies, that’s 13% of the population who will begin aggressively drawing on government support between now and 2030. That would necessitate another 78% increase in healthcare and retirement spending, assuming the current trend holds.

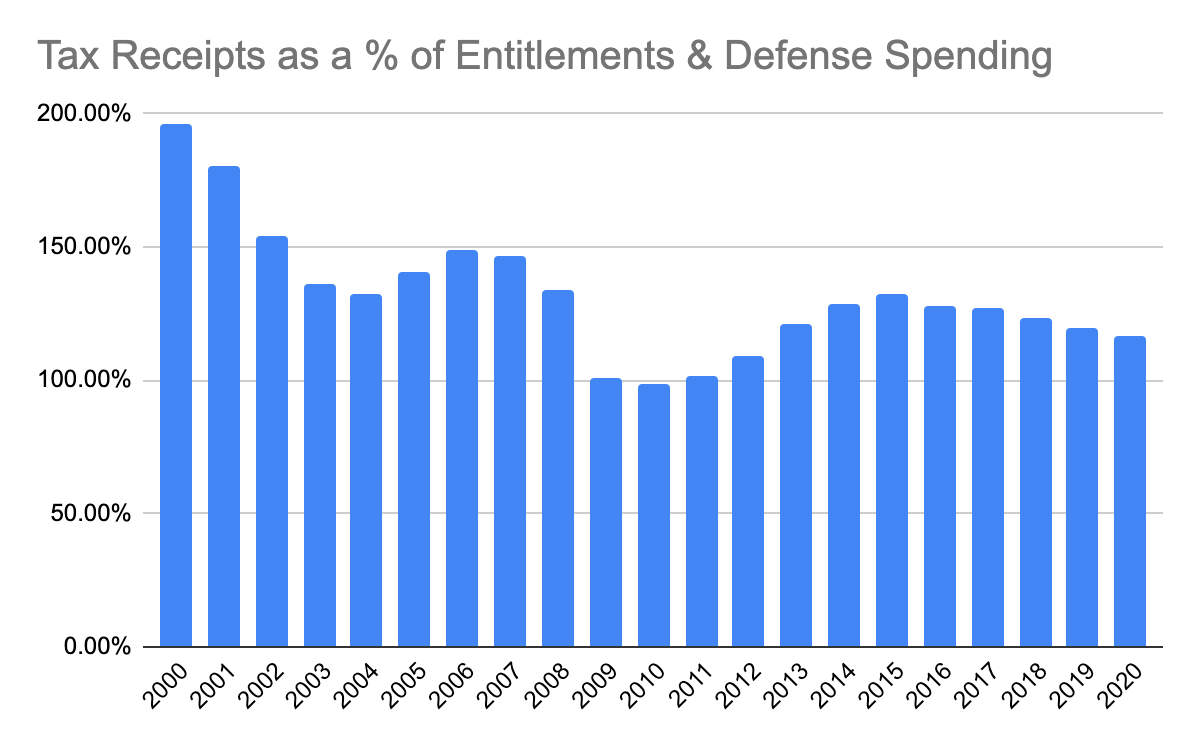

Appreciating the magnitude of healthcare, retirement, and defence spending is the goal of this exercise, the next issue is how the USG will pay for increasing costs of programmes essential to the compact with the people. Given the immense amount of fiscal spending that is already happening, many believe that now the USG will resort to aggressively raising taxes on capital to pay increasing expenditures.

This chart displays what percentage of the total spend on Medicare, Medicaid, Social Security, and Defense is covered by annual tax receipts. The takeaway is that taxes now barely cover 100% of the cost, down from 200% of the cost 20 years ago. Of the last 20 years, the presidency was held by a Republican 60% of the time, and a Democrat 40% of the time. Regardless of which party was in power, expenses rose faster than income.

These programs’ costs increased 207% from 2000 to 2020, while tax receipts grew by 83%. If we extrapolate this trend out another decade, tax receipts would only cover 90%. The government still has roughly 30% to 40% in additional budgetary items that need to be paid for over and above entitlements and defence spending. This assumes that productivity and economic activity will not be affected by higher tax rates. It is a spurious assumption that humans will produce the same or more when they take home less and less from their efforts.

Taxes are never able to cover all the goodies the government promises. The USG, like all governments, will borrow to meet their societal obligations. This is especially true when the cost of doing so is comparatively cheap, in this case because the USG possesses the printing press to the world’s reserve currency.

No Choice But Up

Slowing the pace of the Fed’s balance sheet growth is the same thing as raising interest rates. Without the Fed stomping on interest rates, they would be markedly higher because foreigners are not recycling as much of their trade dollar earnings into the Treasury markets.

There is no politically important stakeholder that benefits from higher interest rates.

Bond holders, both foreign and domestic, suffer mark to market losses on their portfolios.

Equity holders suffer as a rise in the discount rate applied to a future stream of dividends means that valuations get crunched. Economic dogma holds that if the stock market is rising, the real economy must be doing better. Therefore, if the stock market is falling, the real economy is doing worse. TL;DR: don’t let the S&P fall.

The USG must borrow more and more each year in order to provide healthcare, retirement, and defence goods that get progressively more expensive as the population ages and the world order becomes more multi-polar. Jacking up tax rates is both unpopular at the extremes, and insufficient to generate the revenue needed. The USG needs the Fed to play ball and ensure that rates remain low while it pumps debt into the economy to generate above-trend growth.

The only winner of austere monetary and fiscal policies are those who benefit from a strong and stable USD. If the US had a debt to GDP ratio substantially below 100%, then it could be argued that the US can afford domestically to continue bearing the cost of the global reserve currency. But now that it is a twin deficit country with a domestic middle and lower class that have borne the cost of the fiat USD regime for 50 years, the ability to sell austerity as a palatable policy is gone.

Try Try

All these nice words and charts are great, but the Fed still wants to believe it has options. Therefore, they will try to reduce the pace of bond buying – likely to disastrous effect. In 2013, the acting Fed governor spoke about possibly tapering bond purchases in the future and the market threw a fit. Stonks and bonds got the stick, and Bernanke got with the programme right quick. JK y’all, bond buying will continue on schedule.

Every time the Fed attempts to extricate themselves from QE 4 EVA, the market says NYET. The stakes are even higher this time, because the stated policy of the USG is that we are at war with COVID and will therefore spend whatever it takes because we can. Similar to the 1939 – 1951 period, the Fed will implicitly or explicitly be called upon to buy bonds to engineer a Treasury yield curve that is below the rate of yearly economic growth.

Right now there are two problems – the Fed is thinking about thinking about reducing monthly bond purchases, and US government elected officials haven’t passed any new massive spending bills. The crypto markets gave a prelude to what will happen to the equity and bond markets if the Fed and the USG don’t work together to spend more money.

I fully expect cross-asset-class carnage to continue into the early fall. The Fed has two policy meetings in June and July. If they start to seriously talk about tapering balance sheet growth, watch out.

The Democrats need to figure out a way to pass their infrastructure bill. Who knows what sorts of compromises they will make to get it over the finish line, but we need more stimmie cheques. The expanded $3,600 child credit for 2021 is a good step towards keeping the mana from Washington D.C. flowing and Robinhood accounts filled to the brim.

All this to say, if the Fed’s balance sheet is going to grow 10x, a lot more borrowing needs to happen quickly. Nothing goes up or down in a straight line. Without falling equity prices and rising interest rates, the inertia of a large bureaucratic organisation will subsume the efforts to fiscally expand aggressively. Again, I believe we will see a global negative market reaction this summer and fall.

How High?

The point of this essay is to argue that, in order to fight the war with COVID and avoid exacerbating social unrest, the only politically acceptable course of action is nominal GDP targeting paid for with borrowed money. In order to keep the cost of borrowing lower than achieved growth, the Fed will expand its balance sheet to whatever level is necessary.

The nominal GDP growth-targeting policy works – the only issue is preventing out of control inflation in wages and goods. But sometimes, it’s a politically acceptable outcome. During and after a war a government always accepts this type of pernicious inflation, as it’s the only way they can pay for the endeavour.

The trick is to spend the money on endeavours whose real economic value yields more than the interest on the debt issued. China has pursued such a strategy with great success from the late 1970’s until today. Michael Pettis argues that the true cost of debt outpaced economic growth sometime after 2008. China amassed the largest stock of debt ever in human history because it adopted the nominal GDP targeting policy with a supreme gusto, and it doesn’t issue the global reserve currency. If the US dedicates itself as well, the sky’s the limit to how much debt the Fed can warehouse.

I cannot predict with any certainty how large the Fed’s balance sheet will grow. I only know that if such a policy is pursued, the only way to pay for it is through money printing. The question for us traders and investors is what financial asset we can own that rises at least at the same pace as the Fed’s balance sheet.

The US has already begun the process. Let’s assume by the end of 2021 the US 10-year note yields 2% and GDP grows by 6.5%, which is the current estimate by the Fed and “respected” economists. That is a negative 4% real yield.

You Have One Fucking Job

Water, water, every where,

And all the boards did shrink;

Water, water, every where,

Nor any drop to drink.

– The Rime of the Ancient Mariner

This is one of my favourite verses of poetry, and it is so apropos of the current liquidity situation. There is so much apparent liquidity due to the Fed’s monthly bond buying; however, the actual water we need can only come from the USG and Treasury passing massive spending bills which necessitate issuance of a lot more bills, notes, and bonds.

Unfortunately, this essay is too long already so I cannot go too deep into how exactly the transmission channel of quantitative easing works. But essentially, when the Fed buys Treasuries from the Too Big to Fail banks, it credits them with bank reserves which are held at the Fed. Due to capital adequacy ratio rules, banks must hold additional capital against these reserves. However, if they hold Treasuries they need to hold much less, or none at all.

When the Fed conducts open market operations and purchases Treasuries from the banks, it takes a superior form of collateral and replaces it with an inferior one. The banks then need to come up with capital to backstop these reserves. This basically hampers the banks’ ability to extend more credit as they need to tie up capital to backstop their large and increasing reserves held at the Fed.

The Fed is hip to this problem, so they conduct reverse repos. This means that the Fed swaps reserves for Treasuries. With one hand, the Fed increases liquidity via purchasing Treasuries from the banks, and with the other it decreases liquidity by swapping them back to the banks. So the net effect is that the overall liquidity conditions in the fixed income markets is unchanged in extremis.

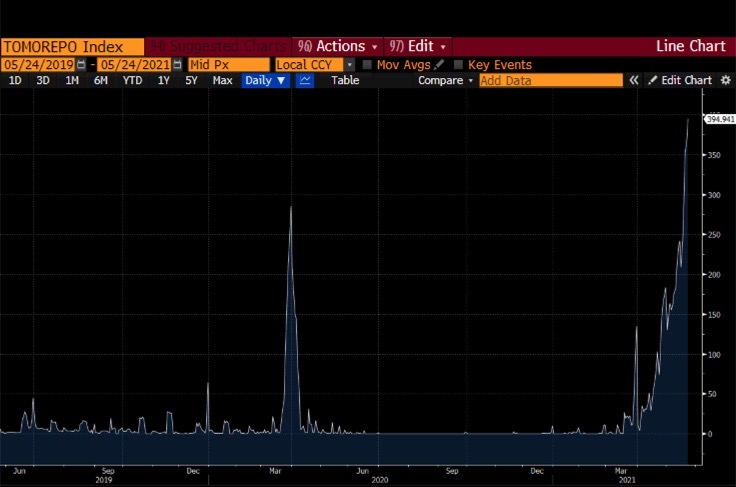

The use of the facility at the New York Fed has surged to all-time highs recently because the market is running out of Treasury collateral. The Treasury / USG needs to spend more money so it can borrow more money. Because if the Fed sticks to their $120 billion per month purchases, of which approx. 70% are Treasuries, there won’t be enough collateral to go around so that the banking system functions, and short-term rates are higher than 0%. There are various structural and legal reasons why the short end of the Treasury curve cannot go negative without causing severe disruption to how the US money markets function.

In 2008, the Fed switched into high-gear money-printing mode. However, every single Fed governor has lamented that they can only do so much. If the USG does not spend more money and thus create more Treasury collateral, their quantitative easing measures are ineffectual. QE only transforms the balance sheets of banks and other financial institutions from those that hold Treasuries to those that hold riskier corporate debt and equities. It does not mean banks will take risks lending to the real economy. It does not put stimmie cheques in the hands of GameStop warriors. It, in essence, does nothing to correct labour’s underperformance vs. capital since the 1970s.

The Treasury is well aware of this fundamental problem. It’s time for it to spend dosh and take us to Valhalla.

Crypto as The Release Valve

When a measure becomes a target, it ceases to be a good measure.

– Marilyn Strathern

The financial markets are a collection of various measures that are supposed to tell us things about different aspects of the real economy. However, these measures cease to have any meaning when central banks turn them into targets. Then, they only tell us the degree to which the central bank will engage in buying or selling an asset to achieve a desired politically acceptable outcome.

Thankfully, unlike our human counterparts in the 1940s and 1950s, we have crypto. Even if they were forbidden by their domestic government from holding gold, the ability to express yourself financially was only really available to the extremely rich. Everyone else just ate their humble pie and grumbled while their savings were eviscerated to pay for the world’s second iteration of total war.

Here are the various measures and how they have become targets:

Government Bonds – Almost every central bank globally distorts their domestic bond market via aggressive purchase schedules. Therefore, government bond yields only tell us how much a central bank is willing to expand its balance sheet – it tells us nothing about the true and appropriate cost of money.

Equities – Almost every central bank globally is active in their respective domestic equity markets. The Fed isn’t yet, but all it would take is a sustained fall in the S&P 500 and they would find a way to support the equities market. Central bankers and most politicians believe their scorecard is the performance of the equities market, and that it somehow means the real economy is healthy. But if you can target any level of equities via printing money to purchase them in the necessary amounts, then stock market performance tells you nothing about the actual health of the domestic public corporate sector.

Housing – Almost every central bank globally is active in their respective domestic housing financing markets. The US is an anomaly in how developed its mortgage-backed asset markets are, but central banks and federal governments set stamp duty rates, mortgage rates, and other affordability measures to encourage or discourage the purchase of houses. It is not a great measure, because there are so many idiosyncratic policies that distort the price of a house representing materials and imputed owner-occupied rent.

Gold – The interesting thing about gold is that it might just get its mojo back. The large bullion banks, starting in June this year, will face changes to how they account for and fund unallocated gold on their balance sheets. Basel III’s new rules might make it impossible to suppress the gold markets via creation of unlimited paper shorts. If this actually comes to pass, then gold might once again be a measure of monetary inflation rather than a sleepy rock that sits in vaults around the world.

This is a chart of Bitcoin and Ether indexed against the Fed’s balance sheet in the post-COVID era. The data is indexed at 100 starting 1 Jan 2020. Even with the most recent vicious sell-off, both have done exceptionally well at growing purchasing power. Bitcoin and Ether have outperformed the Fed’s balance sheet by 2.3x and 15x respectively.

No organisation with a printing press has a target price for any crypto. Quite the opposite, they believe crypto just represents the madness of electronically connected crowds. That’s perfect because crypto can function as the only working smoke alarm for the monetary inflation that is sure to come if / when the issuer of the global reserve currency resorts to nominal GDP targeting funded by their captive printing press.

If after all these words you agree with me, then the fluctuations in the total crypto market cap are immaterial. As the Fed balance sheet grows, the crypto market cap will grow along with it. The relative performance of the coins within the crypto firmament is up to narrative, technology, and adoption. Now that I have laid out my global macro thesis for why it is foolish to be short the crypto market as a whole, I can get back to in-depth analysis of the crypto micro-market structure and how DeFi will render most of the current financial institutions useful only to those who refuse to use digital payments.

Related

The post appeared first on Blog BitMex