(Any views expressed in the below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

In the dark ages before TikTok and Instagram entertained us with duck lips and alphabet luxury brands wearing peacocks, car rides used to be very boring – at least for me. I got car sick when reading, so my many five-to-six hour journeys between Buffalo, New York and Detroit, Michigan were bone-crushingly boring. I listened to a lot of banal radio. One particular show I remember was a cigar aficionado broadcast hosted by Cigar Dave. I don’t smoke – never have – but nonetheless I received an early education on the difference between Cuban and Dominican Republic tobacco wrapping methods.

I sat through these treks in silence, because asking “are we there yet?” was pointless – I knew the kilometre markers on the Canadian QEW and 401 by heart. I’m sure my parents were at least pleased they didn’t have to put up with any whining as they focused on the road.

Us market participants are not so patient with our journeys to amass more financial wealth. In our never-ending search for the next bull market, we routinely find ourselves asking, “are we there yet?”. And in the crypto markets specifically, we often ask when the dogshit we hold in our wallets will once again trade near the pico top of November 2021.

The more savvy traders are looking for leading indicators that might suggest the bull market is nigh, with the goal of identifying exactly when to back up the truck and shovel in crypto. Like a pavlovian dog, we have been trained by our central wanker banker masters to buy financial assets whenever they either cut interest rates or print money in order to expand their balance sheets. We hang on these charlatans’ every word, hoping they will deliver the free money mana that powers risky asset returns.

Fed Balance Sheet (white) and Bitcoin (yellow) indexed at 100

During the COVID Fed money printing bonanza, Bitcoin outperformed the growth of the US Federal Reserve’s (Fed) balance sheet by 129% – confirming that our Pavlovian instinct to invest on the proclamations of the false profit Powell (the Fed chairperson) has been quite profitable.

Since the Fed started raising interest rates in March 2022, a cadre of macroeconomic analysts have been trying to guess when the Fed will stop. I have subjected readers to a number of – in my opinion – beautifully written essays that investigate the many reasons I believe the Fed hiking cycle will ultimately drive some sort of financial calamity that requires them to start cutting rates and expand their balance sheet.

On March 10th of this year, Silicon Valley Bank and Signature Bank limped into the weekend with severely wounded balance sheets, courtesy of Fed policy. By Sunday night, it was clear that these banks were toast, and unless the Fed and US Treasury actually wanted to live the values of free market capitalism and let a poorly run TradFi business fail, some sort of bailout was forthcoming. Unsurprisingly, The Fed and Treasury intervened, and a bailout was offered in the form of the Bank Term Funding Program (BTFP). The BTFP offered an unlimited lifeline to the US banking system, whereby banks could hand their dogshit US Treasuries to the Fed and receive fresh dollars in return. These dollars were then given to depositors, who in turn chose to flee because money market funds (MMF) were offering >5% interest vs. a bank deposit interest rate of near 0%.

This was the moment. I and many others believed the Fed was surely done hiking rates. The Fed’s real number one mandate is to protect banks and other financial institutions from ever failing, and the rot of underwater bonds was spread so wide and far throughout the financial sector that it threatened to take the whole system down. It seemed the Fed’s only option was to cut rates, restore the health of the US banking system, and watch Bitcoin quickly march towards $70,000.

Nope, nope, nope. Instead, the Fed raised rates another three times from March to the present.

When your predictions are consistently wrong, it is time to reexamine what you believe to be true, and explore a few “what if I continue to be wrong” scenarios. In this case, that means starting to work through whether my portfolio can survive a Fed that keeps hiking rates.

I gave a keynote at the Korea Blockchain Week conference last week in which I examined whether Bitcoin could still rise if the Fed and the rest of their central bank sycophants continue to raise rates. For those of you who were not in the audience, or thought I went too quickly through some concepts, here is a short essay – by my standards, at least – exploring this question.

What If?

What if there is no US recession?

What if inflation doesn’t fall?

What if there is no US financial system meltdown?

If these all hold true, then rather than a rate cut, we can expect more rate hikes by the Fed and other major central banks.

Real Yields Past and Present

What is the real yield? Real yield is a fairly amorphous concept, and depending on who you ask, you might get a handful of different definitions. My (slightly oversimplified) definition is that if I lend money to the government, I should at least get a return that matches the nominal GDP growth rate. If I get less than that, the government is earning a profit at my expense.

Obviously, governments would love to fund themselves at a lower rate than the economic value their debt generates. Using financial repression to ensure that nominal GDP growth is higher than bond yields has been the policy of all the most successful export-led Asian economies since the end of WW2. China, Japan, South Korea, Taiwan, etc. have all used this playbook to export their way out of the destruction their countries experienced during and in the wake of WW2.

To implement this type of financial repression, countries must use their banking systems. Banks are instructed to offer depositors low rates. Depositors then have no choice but to earn a negative real yield on their savings, as the government puts restrictions in place that prevent them from moving money out of the system. The banks are then told to lend to state-backed or large, politically connected heavy industrial firms at low rates.

Deposit Rate < Corporate Loan Rate < Nominal GDP Growth Rate

The result is that these industrial companies – which require a large amount of CAPEX – get cheap funding to quickly build out a modern manufacturing base. Governments then use these manufacturing bases to accrue sovereign wealth, which is recycled into US Treasuries and other dollar-based financial assets. Supposedly, these funds can be tapped into when the economy falters. The plebes all get good-paying, blue-collar manufacturing jobs for life. When compared to their prior lives as agricultural peasants, during which they endured a standard of living only slightly better than that of slaves, working nine to five with full benefits for a large corporation is a major improvement.

This is a major reason why I dismiss folks like Peter Zeihan who believe the Chinese Communist Party’s (CCP) rule is about to come to an abrupt end. Due to the horrendous loss of life and destruction of property experienced after 1911 (fall of the Chinese Qing dynasty) and 1949 (when Mao’s communists bested Chiang Kai-Sek’s nationalists), Chinese comrades put a huge premium on stability. The CCP has delivered that since Mao’s death, and thus, they ain’t going nowhere – even if the economy deflates substantially.

Real Yield = Government Bond Yield – Nominal GDP Growth

This financial repression playbook only works if money cannot leave the banking system. This is why China, Taiwan, South Korea, etc. all have closed capital accounts. Or in the case of Japan, the government makes it nearly impossible for foreign financial firms to advertise and/or accept Japanese savers – and as a result, the average Mrs. Wantanabe is stuck leaving her money with a Japanese bank earning a negative real yield. In our current digital age, however, this strategy becomes harder to execute – particularly given the rise of alternate, decentralised financial systems like Bitcoin. When real yields turn negative for sustained periods of time, depositors can now leave (or at least, they think they can) before the gates are shut.

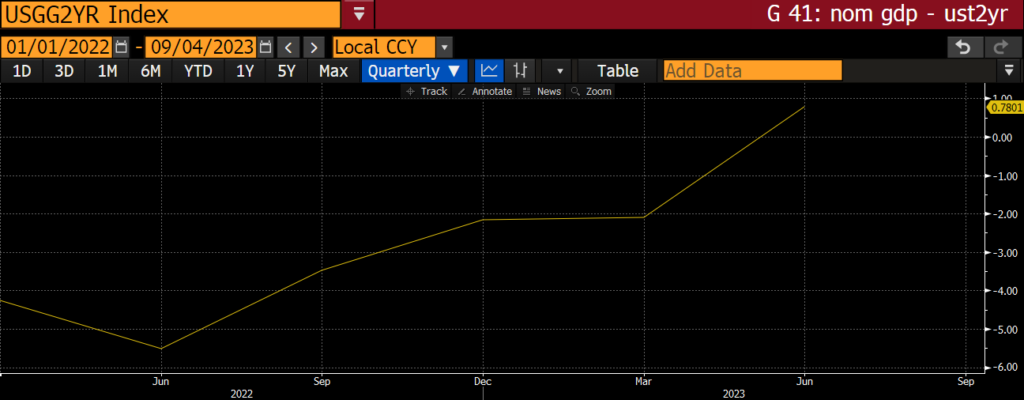

Let’s look at real yields using this construct in the US, starting from 2022 up until the present.

US 2-Year Treasury Yield minus US Nominal GDP Growth

I used the 2-year US Treasury yield to represent government bond rates as this is the most popular and liquid instrument that tracks short-term rates. As you can see, real rates were really negative when the Fed started hiking in March 2022. The Fed raised rates at the fastest pace ever, and yet real rates are now only barely positive. If you replace the 2-year yield with the 10-year or 30-year yield, real rates are still negative. That’s why it is foolish to own the long-end with your own money. Institutions still do, because financial responsibility goes out the window when you are a fiduciary playing with others money and earning a phat management fee for being of average intellect and ability.

As I considered the chart above, my next question was, “what can we expect real yields to look like moving forward?” The Atlanta Fed publishes a “GDPNow” cast, which is a real-time guestimate of what the current quarter’s real GDP growth will be. As of September 8th, the Fed is predicting that third quarter growth will be a mind-bogglingly massive +5.7% – I bet China wishes they could grow like this! To arrive at a nominal growth rate, I added another 3.7%, which I calculated by looking at the average differential between nominal and real growth over the last six quarters.

Nowcast Real GDP of 5.7% + Real GDP Deflator of 3.7% = Nominal 3Q GDP Growth of 9.4%

Forecasted Third Quarter Real Yield = 2-year US Treasury Yield 5% – Nominal 3Q GDP Growth of 9.4% = -4.4% Real Yield

What the actual fuck!!!! Conventional economics says, as the Fed raised rates, growth in a very credit sensitive economy would falter. Common sense tells us that in these conditions, nominal GDP growth should be falling and real rates rising. But that is not happening.

Let’s examine why.

No Money, No Honey

Governments earn money through taxation, and then spend it on stuff. If spending is greater than tax receipts, then they issue debt to fund the deficit.

America’s chief export is finance. As such, the government earns a large slug of revenue from capital gains taxes levied on rich people making money in the stock and bond markets.

The COVID bull market of 2020- 2021 produced a big-ass tax haul from rich people. However, from the beginning of 2022 onwards, the Fed began raising interest rates. Higher rates visited a swift death upon financial asset markets. It is the chief reason why do-good scammers such as Sam Bankman-Fried and crypto Zhupercycle muppets like Su Zhu and Kyle Davies bit the dust.

Below is a chart showing the return indexed at 100 of the S&P 500 (yellow), the Nasdaq 100 (white), the Russell 2000 (green), and the Bloomberg US Aggregate Total Return Bond Index (magenta) from 2022 to the present.

As you can see, since the beginning of 2022, nobody made money. And as a result, capital gains tax receipts have plummeted. The US Congressional Budget Office estimates that in 2021, realised capital gains represented ~9% of GDP. Taxes on that booty withered quickly as the Fed embarked on its mission to fight inflation.

“Processing data from the Internal Revenue Service (IRS) indicate that realized gains increased sharply in 2021, to 8.7 percent of GDP in CBO’s estimate—the highest level in more than 40 years.”

Additionally, remember that the number one job of any politician is to get re-elected. Old boomers were promised free-ish healthcare, and the US general public loves consuming energy at a per-capita rate well above the rest of the world. Given these two facts, it’s safe to assume that politicians who campaign on reducing healthcare spending and/or the defence budget (the US loves bombs over Baghdad as long as the oil flows back home) will not be re-elected. Instead, the government will continue to spend more and more on both sectors as the population ages and the world becomes more multipolar.

If spending is increasing but revenue is declining, deficits must rise. Since GDP is just a snapshot of economic activity, when the government spends money, it by definition increases GDP – regardless of whether the spending is actually productive or not.

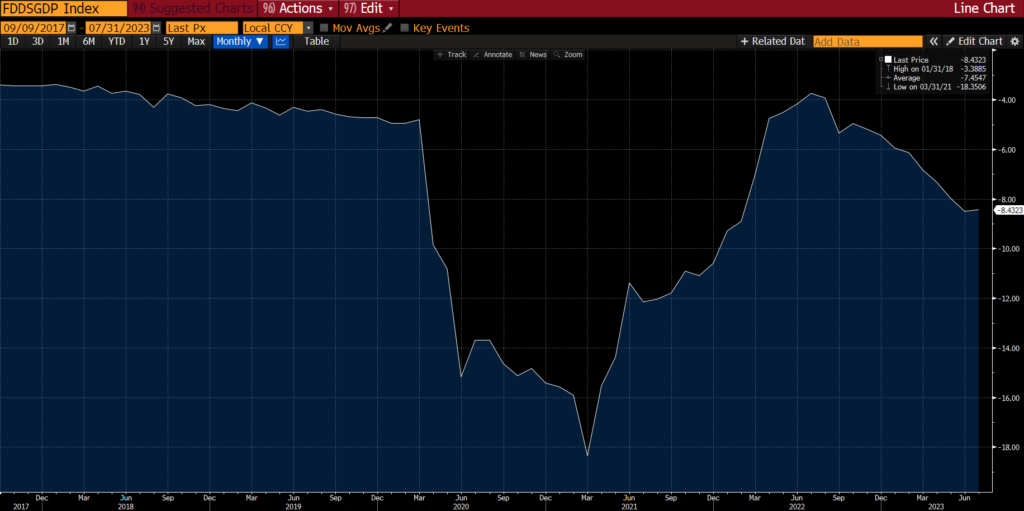

US Government Deficit as a Percentage of Nominal GDP

The last reading is a mind boggling 8% of nominal GDP.

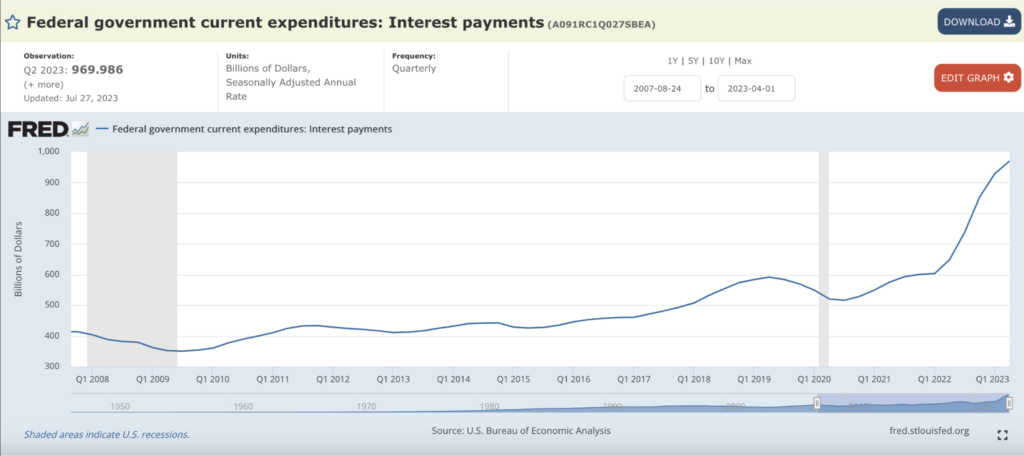

Rising deficits must be funded by selling more and more bonds. By the end of the year, the US Treasury must sell an additional $1.85 trillion worth of bonds to repay old debt and cover the budget deficit. And in addition to having to issue these bonds, the Fed is raising rates – which in turn increases the amount of interest the US Treasury must pay.

As of the end of the second quarter, the US Treasury is spending an annualised $1 trillion on interest payments to debt holders. Given that most wealth is concentrated in the top 10% of households (meaning that those households are the ones holding the bulk of the government’s debt), the US Treasury is essentially handing out stimmies to rich folks in the form of interest payments.

What do patricians buy when they’ve already accrued enough money to cover the most important shorts in life (housing and food)? They spend money on services. Roughly 77% of the US economy is services related. To sum up: when rates rise, the government increases interest payments to the rich, the rich spend more on services, and GDP pumps even more.

Circle Jerk

Let’s put all of this together and do a quick step-by-step walkthrough of how the Fed raising rates increases nominal GDP, which in turn begets more Fed monetary tightening.

The Fed must raise rates to fight inflation.

I never get tired of this photo. Powell looks like a beta simp cuck as Biden points his pen at him and instructs the Fed to deal with inflation.

Financial asset prices fall, and then so does tax revenue.

Apart from a few standout tech stocks like Nvidia, most companies who make real stuff are struggling due to the rising cost and declining availability of credit, which has in turn driven down their stock prices. When it comes to the largest asset market in the world, bonds are poised to notch their 2nd straight year of losses on a total return basis. With the broader stock and bond market still below 2021 highs, the government’s capital gains tax revenues are down sharply.

While tax revenues are falling, government spending increases, resulting in higher deficits. The more the government spends above its means, the greater its deficit. If more spending = higher deficit, and more spending also = higher nominal GDP growth, then ipso facto, higher deficit = higher nominal GDP growth.

The US Treasury must issue more bonds at a higher rate of interest due to higher Fed policy rates.

Rich savers haven’t had this much interest income in over 20 years.

Rich savers consume more services with their interest income, which further boosts nominal GDP growth.

Roughly 77% of US GDP is made up of services.

Inflation becomes sticky because nominal GDP growth > government bond yields.

Higher bond yields are not putting a damper on US government spending because the US government is net-net profiting from this situation. When the government funds itself at a rate lower than the growth generated by its debt, debt-to-GDP actually declines. This is the exact same playbook the US government used after WW2 in order to pay down its massive domestic war debts.

The Fed must raise rates to fight inflation.

As GDP growth continues to outpace bond yields, inflation will rise from its current “depressed” levels and be sticky in the high single digits. As long as inflation is much higher than the Fed’s 2% target, they must continue to raise rates.

Chink In The Armour

Sir Powell can continue raising rates so long as the market is willing to accept a rate of interest lower than the nominal GDP growth. But Lord Satoshi gave the world an alternative financial system, complete with a fixed supply currency and a decentralised, near instantaneous payments network called Bitcoin. The banks have competition that they’ve never faced before. (Of course, you could previously pull your money out of the bank and buy gold, but it’s impractical to use heavy gold in everyday life.)

If/when the market demands to receive at least a 9.4% yield (equal to the forecasted nominal GDP growth rate) on their US Treasuries, then the jig will be up. The Fed must then either forbid banks from allowing transfers to digital Fintechs offering physical cryptocurrencies, or it must restart quantitative easing (aka money printing) and buy bonds to ensure their yield is less than nominal GDP growth. I will continue to remind you that purchasing an ETF does not get your money outside of the TradFi system. Escape only comes through buying Bitcoin and withdrawing it to your own wallet, where you hold the private keys.

It is logical to assume the market will tire of handing profit to the government when there are financial escape hatches like Bitcoin readily available. But for the rest of this analysis, I will assume the Fed will be able to continue down this path of raising rates without too much money fleeing the US banking system.

Climate Change

We have been conditioned to believe that when interest rates go up, the price of risky financial assets like Bitcoin, stocks, gold, etc. should fall. But, because the government has continued its spending bonanza and driven GDP sky high, the real yield that folks are earning on seemingly valuable ~5% government bonds may actually be closer to -4% – meaning that risky assets are still a very attractive proposition for investors.

Investors’ search for positive real yields kickstarted a Bitcoin bull market, which began in earnest on the fateful weekend of March 10. Bitcoin is up by close to 29% since then. And even though the price has tested $30,000 and failed multiple times, Bitcoin is still trading well above its pre-BTFP bailout level of $20,000.

The market is quietly telling us it believes that, if the Fed continues to hike interest rates, real rates will go even more negative and stay that way for the foreseeable future. If this weren’t the case, then shouldn’t Bitcoin be languishing close to the FTX lows of $16,000? The reason why we aren’t at $70,000 is that everyone is focused on the nominal Fed rate, and not on the real rate when compared to the U.S.’s eye-poppingly high nominal GDP growth. But, this knowledge is slowly trickling out via various mainstream media government propaganda mouthpieces, such as the Washington Post:

“To see this in an economy with low unemployment is truly stunning. There’s never been anything like it,” Furman said. “A good and strong economy, with no new emergency spending — and yet a deficit like this. The fact that it is so big in one year makes you think it must be some weird freakish thing going on.”

As it becomes clear that, even with short-term nominal rates at 5.5%, sitting in bonds is a mug’s game, capital at the margin will begin seeking hard financial assets. Certain assets such as Bitcoin, big tech / AI stocks, productive farmland, etc. will continue rising and confound the majority of financial analyst muppets. It won’t make sense to them that Bitcoin is holding firm because they look at manipulated markets controlled by Fed asset purchases, such as yields on TIPS (US Treasury Inflation Protected Securities) – which are (seemingly) positive and rising.

Setting aside the flawed analysis we are certain to read in the mainstream financial press, I believe I have demonstrated that Bitcoin can survive a Fed that must continue to raise rates. It gives me comfort because, while I still believe the base case scenario is that the Fed is forced to cut rates close to zero and restart the QE money printer, even if I’m wrong, I’m confident that crypto can rise quite substantially regardless.

The reason why Bitcoin has such a positive convex relationship with Fed policy is that debt-to-GDP levels are so high that traditional economic relationships break down. It is analogous to how, as you raise the temperature of water to 100 degrees C, it will remain a liquid right up until it suddenly boils, becoming a gas. Things become non-linear – and sometimes binary – at the extremes.

The US and the global economy is at such an extreme. Central banks and governments are flailing about trying to use the economic theories of yesteryear to combat the novel situations of the present; meanwhile, the 360% global debt-to-GDP ratio is creating bass-ackwards situations that require a complete re-thinking of how assets correlate with each other.

You can definitely teach an old dog new tricks, but the dog has to want to learn those tricks in the first place. The scallywags we allow to rule in our name have no such desire to learn – and as such, Lord Satoshi shall punish them with a strong Bitcoin.

Related

The post appeared first on Blog BitMex