Around the Block #5: Downstream Impacts of the Recent Market Crash on Lending, Stablecoins, and DeFi

Coinbase Around the Block, sheds light on key issues in the crypto space. In this edition, Justin Mart analyzes three industries impacted by the recent market crash.

Lending Markets: Behind the Scenes on What Drives Rates

The crypto lending markets have seen strong traction, with an estimated $13B in total loan originations over the past several years from both traditional institutions and crypto-native offerings.

For context, lending markets enable participants to:

- Lend their crypto to others and receive interest rate payments

- Borrow crypto against posted collateral for an interest rate fee

These markets are either offered through central intermediaries or smart contract platforms that seek to ensure against a loss of funds. The primary revenue stream for companies in this space is Net-Interest Margin, where players capture a spread between the interest rate offered to borrowers and the interest paid out to lenders.

But lending activity comes with risk. Borrowers can default on loans, especially when the underlying collateral (crypto) experiences significant volatility. In this piece, we examine how lending markets behaved in the recent crypto crash on March 12. But before diving in, we first need to understand the mechanics behind what drives interest rates, and how this is tied to market conditions.

Why do people take out loans?

Borrowers post some form of collateral and borrow either crypto or cash for:

- Speculation — Going long or short crypto by either borrowing crypto and selling for cash (going short), or borrowing cash and buying crypto (going long). Both are important mechanics for investors to amplify return and/or hedge risk, especially during high volatility periods.

- Working Capital — Liquidity to fund business endeavors or personal matters. Bitcoin as working capital is important for several businesses (e.g., miners, OTC desks, remittance, prop trading firms, etc) who require access to significant capital to facilitate operations. Moreover, borrowing is typically not a taxable event, and thus is an opportunity to keep exposure to crypto without incurring tax penalties.

- Derivatives arbitrage

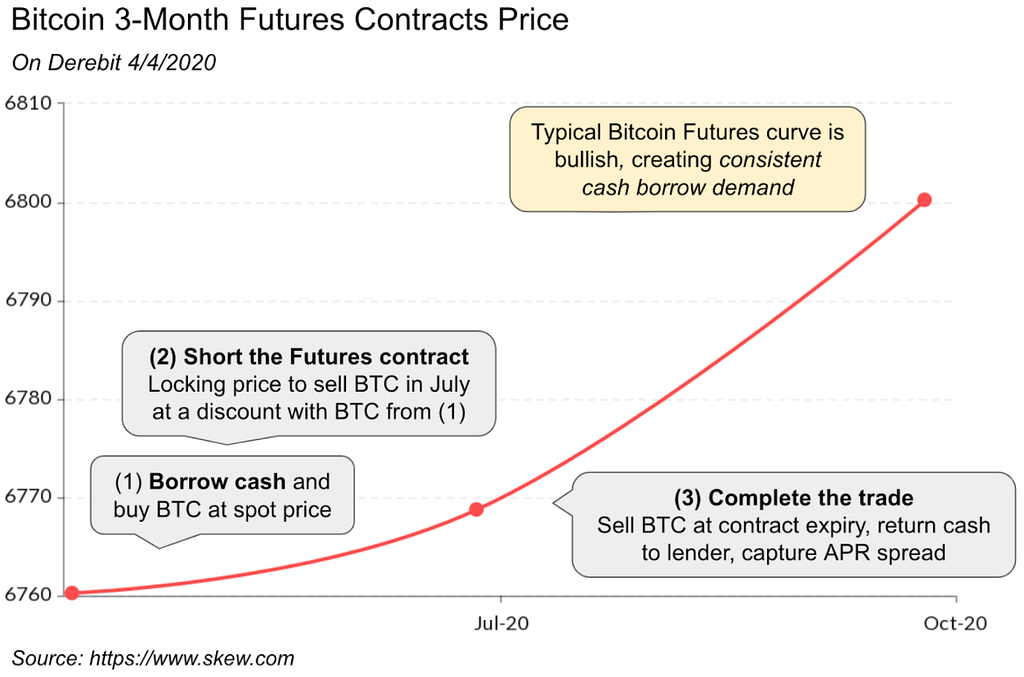

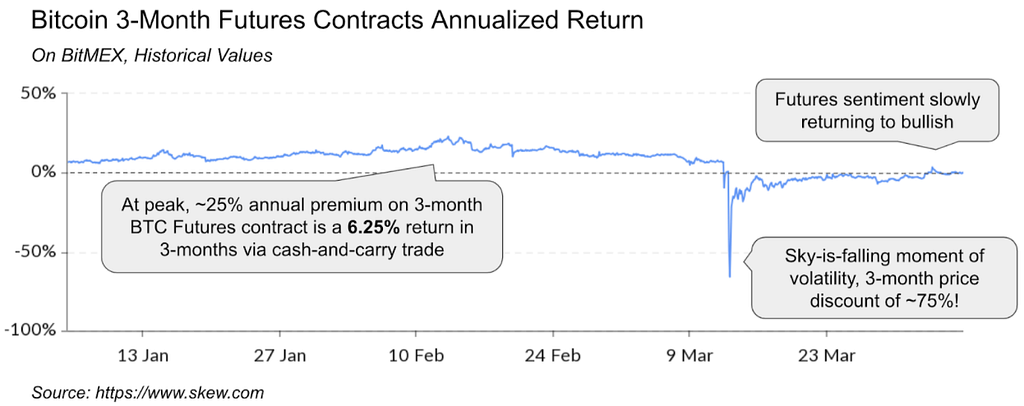

Derivatives arbitrage requires a deeper explanation. Take Bitcoin futures contracts as an example. These contracts are agreements to buy or sell Bitcoin at a specific price at some point in the future, and how these markets are priced reveal investor sentiment. Typically, BTC futures markets are bullish, where the price to buy or sell a Bitcoin 3 months in the future is higher than the spot price today.

The difference between the spot price and the futures price represents an opportunity for arbitrage through a cash-and-carry trade. If the 3-month BTC futures price is 5% higher than today’s spot price, a savvy investor can borrow cash to purchase BTC today, and simultaneously go short on the Futures market (locking in their sale price in 3-months at the 5% premium), effectively capturing a 20% APY over the next three months. If the interest rate charged on borrowing cash over 3-months is less than 20% APR (and any additional fees), you profit on the difference.

Crypto market sentiment is usually net-bullish. The average volume on Coinbase Consumer is 60% buys, borrow demand is net-long from leveraged long traders, and the futures curves are typically bullish. This sentiment drives cash borrow demand, but what happens when the market turns bearish?

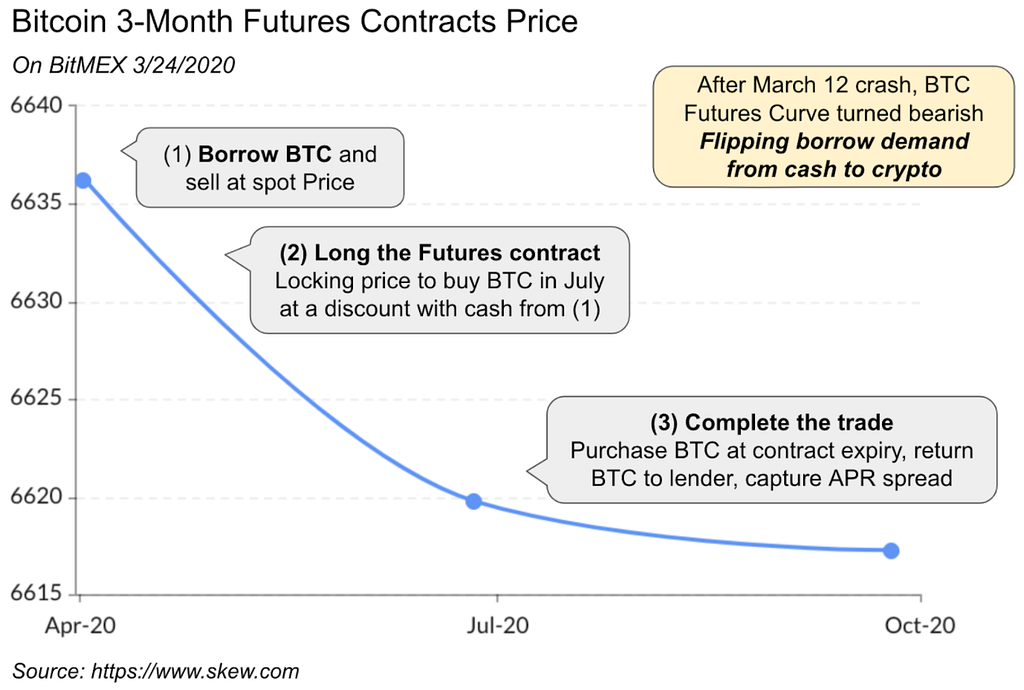

For one, the cash-and-carry trade turns to a crypto-and-carry trade, where you would borrow BTC instead of cash to capture the Futures arbitrage, and immediately sell on the spot market and go long on the Futures contract.

When futures curves turn bearish, lending markets flip to crypto-borrow, and cash borrow demand dries up.

Given the volume in derivatives markets (often > $5 B / day) and sometimes substantial differences between futures and spot prices, derivatives arbitrage is typically a significant source of borrow demand.

What drives rates? Why are DeFi interest rates typically so high?

Like any market, rates are ultimately a function of supply and demand, but there are deeper mechanics at play:

- Crypto lending markets accept crypto as collateral…: For many crypto institutions and individuals, their deepest pool of capital is crypto, and this is the only viable path to collateralizing loans.

- … And using crypto as collateral is generally higher-risk: Crypto is more volatile making it more difficult to fit into lending risk models. This both restricts the number of companies who accept crypto as collateral (diminished supply), and they demand a higher interest rate to account for the risk.

- Stablecoins are preferred over cash due to increased efficiency: It takes time to upload cash into crypto. Many borrow use-cases require immediate action, and thus restrict options to crypto-native solutions where stablecoins are ready to deploy. This increases demand for stablecoins.

- DeFi Lending desks are still niche and challenging to access…: Only those deeply involved know how to access DeFi services like Compound and think through the risks. This will change, but it still restricts supply today.

- … and carry smart contract risk: DeFi platforms are a collection of smart contracts and potentially vulnerable to exploits. More risk demands a higher interest rate.

Collectively these effects result in typically higher stablecoin and crypto borrow/lend rates, especially in DeFi.

We expect these rates to ultimately compress over time as crypto adoption grows. More lending desks will accept crypto as collateral, stablecoins will grow in adoption, crypto to fiat bridges will be more efficient, and DeFi will become more mainstream and have better protections against smart contract risk. Until then, we can enjoy higher APY on stablecoin lending rates on places like Compound, Dharma, and Dy/Dx.

What happened when the markets crashed, and what should we expect in the future?

The status quo is heavy stablecoin borrow demand from speculation, working capital, and derivatives arbitrage. But when market sentiment flips:

- Borrowing crypto increases: In order to hedge risk (going short)

- Borrowing cash to go long decreases amidst increased risk: Even if you believe markets will go up in the long-term, significant volatility can quickly wipe out your position

- Futures curve turns bearish: Flipping stablecoin demand to crypto demand

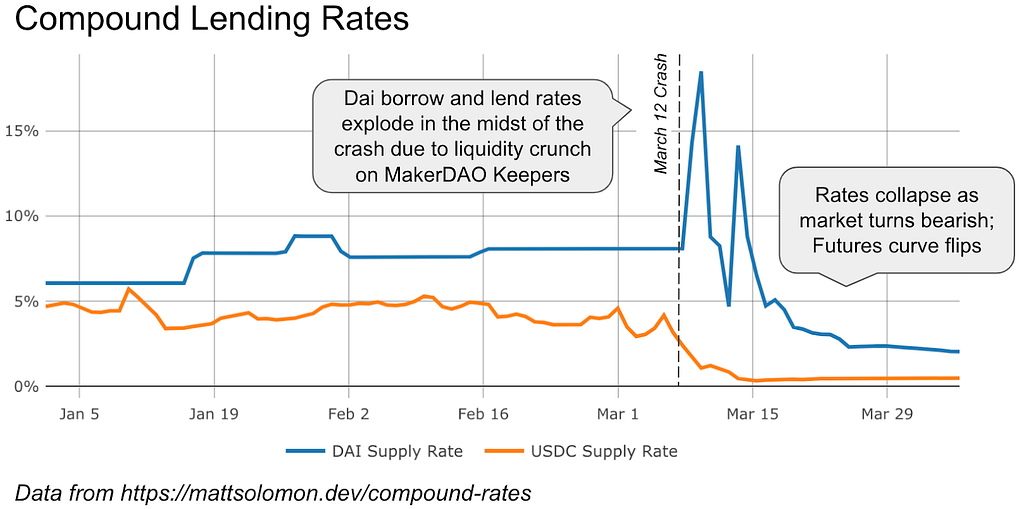

Compound’s Lending rates shows the magnitude of this switch:

As market sentiment returns to bullish and volatility decreases, we should expect stablecoin borrow demand to rise, likely to previous levels. This will be an important development, as many crypto companies rely on high stablecoin APY rates to subsidize growth. These are crypto neo-banks like Dharma, Linen, and Multis.

Overall, crypto borrow/lend is a significant business today, and likely to grow in the future. Market sentiment specifies demand preference, but overall demand remains high in both bullish and bearish markets. Coinbase will look to expand borrow / lend services where possible with the goal of increasing borrow / lend liquidity and helping the crypto market mature.

Stablecoins: Volatility Brings Opportunity for Growth

Before diving in, let’s recap how they are used in crypto today:

- Synthetic dollars for trading and speculation: Many exchanges do not have regulatory approval to offer true fiat services. However the dominant trading and speculative activity occurs between fiat and crypto, and stablecoins enable the long-tail of exchanges to offer synthetic fiat books.

- Settlement: Stablecoins offer the benefits of crypto (fast, global, cheap settlement) without the downsides (price volatility), and are increasingly being used as settlement for goods and services. Anecdotally, Asia appears to be naturally adopting stablecoins in some crypto-adjacent sectors, and Coinbase Commerce is seeing strong but nascent growth in stablecoin adoption.

- Capital flight: Stablecoins like USDC are global and open ecosystems, making them an attractive option for capital flight and USD exposure.

Today, in response to COVID-19 uncertainty the US government has issued a $2 Trillion stimulus package (16x the entire Bitcoin market cap), cut bank reserve requirements to zero, and lowered federal interest rates to record low levels. Meanwhile, the financial markets were gripped with fear where investors sold assets en masse to manage leveraged positions, hedge risk, and seek stability.

So what happened in the Stablecoin markets?

As the markets collapsed, we saw several downstream effects:

- Stablecoins traded at a premium due to increased demand from the broad flight to safety

- Stablecoin issuance increased as arbitrageurs mint stablecoins to sell at a premium and meet demand

- On-chain activity exploded with investors shuffling their holdings between exchanges to manage their positions or capture arbitrage opportunities

The severity and duration of price shocks in stablecoins is directly correlated to the efficiency of the on/off ramps. If it’s dead simple for anyone to mint and redeem a stablecoin for real USD, any shock should be short lived as arbitrageurs quickly step in to maintain price parity.

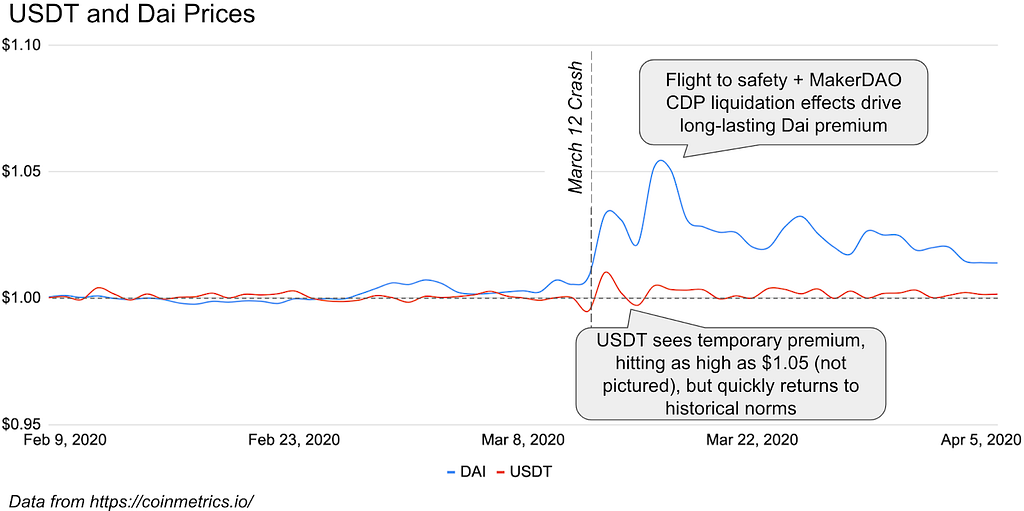

Let’s look at what happened to Tether. USDT’s rails are not the best, and traded as high as $1.05 on March 12th as demand peaked. However arbitrage drove the price back to historical averages in a couple days.

Meanwhile, Dai traded at a more significant premium, and still trades at a slight premium as of April 6th 2020. This is a direct consequence of some deeper mechanics behind the Dai ecosystem, including a failure to keep their liquidation engine running smoothly which resulted in a $4M capital loss on the MKR token (see below for a deeper analysis).

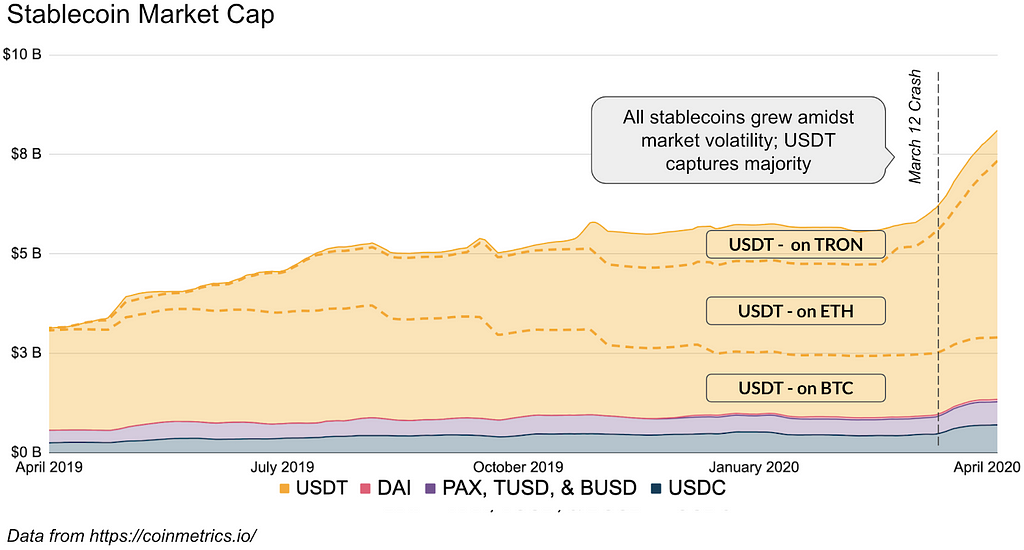

As for market cap, USDT extended its position as the dominant stablecoin, largely due to its existing status as the most liquid stablecoin, especially in Asia.

For many, this is a curious trend given Tether’s seemingly dubious history, close ties to Bitfinex and their apparent use of shadow banks, and repeated concerns that they may be running a fractional reserve. Opinions on this are mixed within the industry, as it seems likely Tether is currently backed by at least 70%, but the market does not seem to mind in either case with Tether continuing to trade at $1 and expanding their lead.

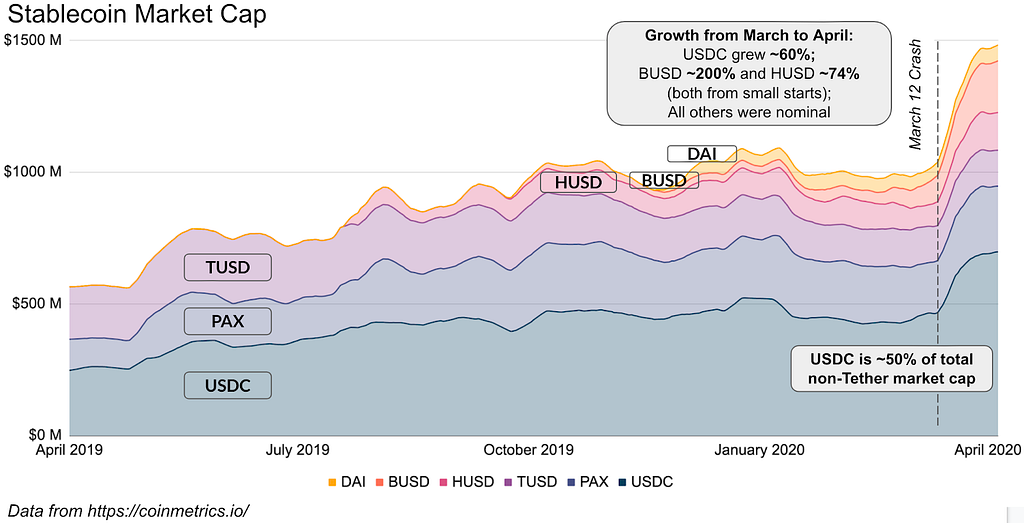

For USDC, these are also opportunities to continue building adoption. While challenging Tether for liquidity may take longer, gaining traction in other areas has seen success. Specifically with Coinbase Commerce, within DeFi with the help of Coinbase’s USDC Bootstrap Fund, and potentially across a number of emerging Neo-Bank and remittance applications. USDC’s status as the regulated, fully-backed stablecoin with smooth fiat on-off ramps has helped it achieve ~50% market cap dominance outside of Tether.

Stablecoins are here to stay and they grow in adoption every day. Additionally, large turmoil in markets are opportunities for stablecoin growth.

Note that stablecoin adoption does not represent capital leaving crypto. More the opposite, it represents capital waiting to re-enter the broader crypto market, a promising signal for stablecoin adoption.

DeFi: MakerDAO Liquidation Engine Breaks Amidst Market Crash

MakerDAO is the smart-contract DeFi platform behind the synthetic stablecoin Dai.

Some context on how MakerDAO functions

MakerDAO functions by users posting collateral (mainly ETH) into a smart contract “Vault”, and printing DAI against their vault’s collateral. If their collateralization ratio drops below 150%, their Vault is in jeopardy of being in default, and anyone can issue an on-chain transaction that closes their vault and auctions off their collateral. This ensures DAI remains backed by sufficient capital, or in a worst case scenario could always be redeemed for $1 of crypto.

What happened when the markets crashed

March 12 saw the price of Ethereum collapse over 50%, briefly dropping below $100 for the first time since 2018. This resulted in two things:

- Several MakerDAO vaults became under-collateralized

- The Ethereum network experienced significant congestion as people moved funds to exchanges, or adjusted open positions (with transaction fees spiking to ~$2)

These two effects had downstream implications for MakerDAO. Usually, when Vault’s are closed and collateral is auctioned off, there are multiple bidders which generally ensures the collateral is auctioned for a fair price. But the price crash also impacted the entities participating in these auctions (called “Keepers”):

- Keepers closed so many Vaults that many ran out of Dai and couldn’t replenish their balance sheet fast enough

- Many Keepers were not prepared for spiking transaction fees, and couldn’t get their auction bids mined quickly

This resulted in only one Keeper bidding on auctions for a 3 hour period. During which, this lone Keeper bid $1 for the collateral, essentially buying ETH almost for free.

The Result and Recovery

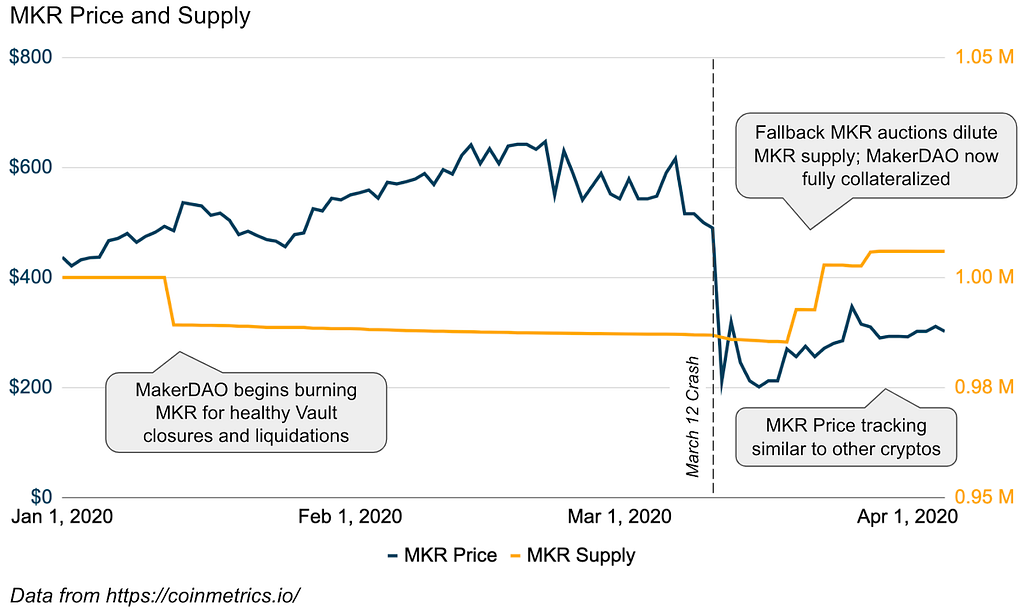

The end result: One Keeper ran away with $4M in ETH almost for free, and the MakerDAO system did not receive sufficient capital to ensure Dai remains fully over-collateralized.

Thankfully, MakerDAO planned for unexpected events like this, adding a secondary auction process that calls for MKR tokens to be minted and sold to cover any bad debts.

This auction recently took place with Paradigm winning most of the auctions at market rates — a solid vote of confidence. This effectively means the MKR token holders experience $4M of dilution, but the Dai is back to sufficient over-collateralization.

Ethereum’s DeFi ecosystem is still early and has a large number of moving parts, so we should expect significant market volatility to bring downstream effects and stress the system in surprising ways. In this case, giving rise to an opportunistic attack on MakerDAO. This is part of the evolutionary process in DeFi, where significant stress tests occur, we learn from failings, and the whole ecosystem becomes progressively hardened.

The industry should not be scared of Dai, it’s deeply ingrained in the ecosystem and is a critical component to DeFi. MakerDAO’s fallback auctions successfully recovered from the bad debt and is sufficiently over-collateralized once again. However, it does mean that DeFi builders should think carefully about how best to mitigate downstream risks and consider the broader implications behind significant market volatility.

Relevant Crypto News Over the Past Few Weeks

Coinbase News

- Techcrunch: Coinbase Wallet lets you earn interest with deeper DeFi integration

- Coinbase: USDC Bootstrap Fund invests $1.1M in Uniswap and PoolTogether

- The Block: Coinbase Card can now be linked to Google Pay

- Techcrunch: Coinbase Exec tapped to be COO and First Deputy Comptroller for U.S. Office of the Comptroller

News from the Crypto Industry

- The Block: Revolut launches in the US

- Circle: Circle announces set of APIs focused on expanding USDC adoption

- Coindesk/CoinMarketCap: Binance acquires CoinMarketCap for reported $400M; CMC will continue to be run as an independent operation

- Binance/The Block/Techcrunch: Binance introduces crypto debit card and later removes all mention of Visa from promotional material; also announces partnership with Brave for in-browser trading

- Decrypt: Huobi launches Coinbase-Like mobile app for Asia

- Kraken/The Block: Kraken launches FX trading; and hires Marco Santori as Chief Legal Officer

- Arthur Hayes: BitMEX knocked offline at height of crypto volatility on March 12 from DDoS attack

- Blockchain.com: Blockchain.com expands with retail borrow/loan product

- The Block: Poloniex adds Token Sale platform, staring with TRON stablecoin project

- The Block: Several exchanges named in series of lawsuits alleging unregistered Securities violations

- The Block: Crypto custodian Anchorage adds support for XRP

- Baakt: Baakt raises $300M series B from ICE, Microsoft, and others

- Brendan Eich: Brave hits 13.5M MAU / 4.5M DAU ?

News from Emerging Crypto Businesses

- MakerDao: USDC added as collateral option in MakerDAO

- The Block: Uniswap competitor Balancer launches; sees solid initial traction

- The Block: Keep raises $7.7M in preparation for April launch of tBTC on Ethereum

- The Block: Decentralized Exchange volume hits all time high in March with >$600M volume

- The Block: ETH 2.0 clients plan to launch testnet in April

- The Block: Synthetix to offer derivatives trading on ETH

Tweets

- Eric Voorhees: On Bitcoin and Coronavirus

- Cuy Sheffield: Head of Crypto at Visa highlights key trends to be mindful of

- Coindesk: Nic Carter’s commentary on the long-term effects of corporate bailouts

- Adam Draper: Adam Draper tweets about the scariest thing he’s ever seen

This website contains links to third-party websites or other content for information purposes only (“Third-Party Sites”). The Third-Party Sites are not under the control of Coinbase, Inc., or its affiliates (“Coinbase”), and Coinbase is not responsible for the content of any Third-Party Site, including without limitation any link contained in a Third-Party Site, or any changes or updates to a Third-Party Site. Coinbase is not responsible for webcasting or any other form of transmission received from any Third-Party Site. Coinbase is providing these links to you only as a convenience, and the inclusion of any link does not imply endorsement, approval or recommendation by Coinbase of the site or any association with its operators.

The opinions expressed on this website are those of the authors who may be associated persons of Coinbase and who do not represent the views, opinions and positions of Coinbase. Information is provided for general educational purposes only and is not intended to constitute investment or other advice on financial products. Coinbase makes no representations as to the accuracy, completeness, timeliness, suitability, or validity of any information on this website and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. Unless otherwise noted, all images provided herein are the property of Coinbase.

Around the Block #5: Downstream Impacts of the Recent Market Crash on Lending, Stablecoins, and… was originally published in The Coinbase Blog on Medium, where people are continuing the conversation by highlighting and responding to this story.

The post appeared first on The Coinbase Blog