(Any views expressed in the below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

The Lord is my shepherd; I shall not want.

He maketh me to lie down in green pastures: he leadeth me beside the still waters.

He restoreth my soul: he leadeth me in the paths of righteousness for his name’s sake.

Yea, though I walk through the valley of the shadow of death, I will fear no evil: for thou art with me; thy rod and thy staff they comfort me.

Thou preparest a table before me in the presence of mine enemies: thou anointest my head with oil; my cup runneth over.

Surely goodness and mercy shall follow me all the days of my life: and I will dwell in the house of the Lord forever.

Changpeng Zhao (CZ), the former CEO of Binance, is a sinner, but not for the reason you are probably thinking, given recent events. CZ and all of us are sinners in the eyes of Lord Satoshi because we profit off of centralisation. Centralisation is the tool of the devil. Satoshi and their love are predicated on decentralisation. Humans – and in the future, maybe AIs – will use decentralised structures to collaborate without coercion to accomplish shared goals. The state powers centralisation, and collaboration is achieved through threats of violence.

In only six years, from 2017 to the present, CZ and the team at Binance grew from nothing into the largest centralised trading venue for crypto currencies in the world. Binance is not only the largest crypto trading venue, but when viewed against all exchanges globally – traditional or otherwise – it would probably be in the top 10 in terms of average daily trading volume.

CZ was a nobody prior to a few years ago. He was a nondescript Canadian of ethnic Chinese descent. His surname wasn’t synonymous with power like, say, a Rothschild, Rockefeller, or a Chinese princeling descendant of one of the immortal eight families. But he rose to become one of the richest humans on earth in less than a decade, and his rise was predicated on allowing millions worldwide to trade crypto. For some, that meant Binance was their way to purchase a coin or token that was a ticket to financial freedom. For others, it was a very efficient way to speculate on a new political, economic, and technological system.

The problem for the financial and political establishment was that the intermediaries facilitating flows into and out of the industrial revolution named blockchain were not run by members of their class. The owners of the intermediaries and the crypto assets themselves were the people themselves. Never before had people been able to own a piece of an industrial revolution in under ten minutes via desktop and mobile trading apps. From a fundamental standpoint, those who owned centralised exchanges used tools of the state, the company, and the legal structure to disintermediate the very institutions that were supposed to run the global financial and political system of Pax Americana. And for this transgression, CZ paid dearly.

How dearly did CZ pay? CZ – and by extension, Binance – paid the largest corporate fine in Pax Americana history … Four Point Three Billion United States Dollars!

That seems a bit strange. Bad Gurl US Treasury Secretary Janet Yellen got up to the podium and excoriated CZ and Binance for all their crimes. Did Former Goldman Sachs CEO Lloyd Blankfein get the same treatment as GS under his reign helped Former Malaysian Prime Minister Najib Razak and financier Jho Loh steal more than $10 billion and saddle a developing country with more expensive international debt? No, Llyod got to retire with his stock options intact, and GS was not deemed criminally responsible. Did any Too Big to Fail bank CEOs get criminally prosecuted for precipitating the worst global financial crisis since the 1930s Great Depression? Nope, they got a free pass because to prosecute them would threaten the banking system. Did HSBC’s CEO spend time in the clinker for his employees physically altering cash deposit points so that Mexican Cartels could launder more money efficiently? Money that they earned selling poison to the American public? Nope, Nope, Nope.

So why the fire and brimstone for a company not even a decade old? Was Binance so big and bad that it committed more crimes than any bank in American history, some of which have existed for centuries? Obviously, the treatment of CZ and Binance is absurd, and only highlights the arbitrary nature of punishment at the hands of the state.

I ain’t no Dostoyevsky, and this is not a philosophical discussion of crime and punishment, but what does this absurdity tell us about our beliefs? It tells me that crypto is one of the most important political, financial, and technological developments in civilised human history. We are attempting to create a parallel financial, political, and economic system that is based on voluntary participation rather than violent coercion. It is so transformative that a man in under ten years can become one of the richest humans in the world, and his company can become more integral to everyday humans’ lives than storied financial institutions that have existed for centuries. For the first time ever, with just a few swipes on a smartphone, we the people can own the bedrock of a new era of digital human society. If you don’t want to get the fuck long Bitcoin and other cryptos after seeing how much energy the state brought to bear on CZ and Binance, I don’t know what else you need to see.

If you are hodling crypto, make sure you do it in a wallet where you control the private keys. Otherwise, you have accomplished nothing and a slave you shall remain.

With that being said, let’s move on to the real point of this essay. China and the US are kind of sorta friends again. The result of this renewed friendship will be that the Chinese money printer will go brrr. Let’s take a look at how the Middle Kingdom is about to throw gasoline on the raging fire that is the incipient crypto bull market.

Panda Power

Modern world history cannot be fully contextualised and/or understood without a sharp focus on China. Many draw the wrong lessons from the World and Cold Wars because they don’t appreciate China’s contribution to the outcome. As a person who has lived almost half his life in Chinese-administered territories (Hong Kong) and countries run by overseas Chinese (Singapore), I am always on the lookout for situations where the market underappreciates current events in the Middle Kingdom. Keeping this in mind, when I saw that the woke San Francisco politicians decided to clean up their shit-filled city overnight for the arrival of Xi Jinping, the ruler of the Chinese Communist Party (CCP), I knew something momentous would occur.

San Francisco recently hosted the APEC Summit. On the sidelines, Xi and Slow Joe, the US President, met and reset the tense relationship between China and the US. Pippa Malmgren wrote an excellent essay about the meeting and its importance. I’m going to quickly summarise the article so that I can move on to the important thing: how we stack sats given a particular interpretation of the events.

Pippa essentially said:

The Democratic party needs to get re-elected. The first step is to ditch Slow Joe and upgrade Gavin Newsom to the heir apparent. Why is the governor of a state meeting Xi Jinping all on his own … must it be because he is the chosen successor to Biden? Man … Newsom is a fine-looking gentleman (that’s me talking, not her). But having a mentally cognizant silver fox candidate for president is not enough; some serious issues with the economy must be rectified.

Gavin Newsom gifting Xi Jinping a customised Golden State Warriors jersey.

Remember the $105 billion Slow Joe asked the US Congress for a few weeks back? He wanted money to fight wars in Ukraine and Israel, stop dopers dying from fentanyl, and increase defence spending on Taiwan. If China could eliminate these risks, it would keep the price of oil low and the US Treasury market orderly.

Why does the price of oil matter so much to a politician? The higher the price of oil, the less an economy grows because economic activity is just energy transformed. Like all voters, American voters decide at the margin who they will pick based on recent economic performance.

According to statistics from the US’s National Bureau of Economic Research (NBER), since the end of World War I in 2018, the sitting US President has won re-election 11 times out of 11 if the US economy was not in recession within two years of an upcoming election.

However, sitting US presidents who went into a re-election campaign with the economy in recession won only one time out of seven.

– Pg. 62, The New Global Oil Market Order And How To Trade It

How does China remove these four expensive line items?

Let’s start with Ukraine.

By now, it is plain to see the Western media has soured on the Ukraine war. No longer does the Western press celebrate the President of Ukraine Zelensky, instead they constantly highlight how the war is at a stalemate and is unwinnable. The US wants this war to go away, but Russia isn’t going to stand down just because the US elites are tired of lighting money on fire. The only way to bring Russia to the negotiation table is for Putin’s daddy, Xi, to order it. A plausible outcome would be for Russia to keep the territory it holds and the remainder of the rump Ukrainian state to be aligned with the West and potentially be granted membership in NATO. Once a deal is made, the West would likely suddenly drop any Russian sanctions so that commodities can enter the global market. That depresses prices and, along with it, inflation.

“Ukrainian and Russian offensives are struggling for a major breakthrough against strong defensive lines.” – WSJ

Let’s be honest here, Russia never stopped selling commodities to the West. The result of the ineffective Russia sanctions was to route commodities first to places like India, which happily slapped some vig on top and sold it back to the Europeans more expensive.

Moving on to the war in Israel.

Most Middle Eastern leaders pay lip service in supporting the cause of the Palestinians. They talk tough to placate their populace, but are all too willing to take money and gifts from the West and stand aside while Bombardier Bibi runs amok. But it’s harder to do nothing when women and children are slaughtered day after day on live television. How can Iran’s leadership, the supposed financial backer of Hamas, stand by and let this happen? They can’t and won’t unless their state sponsor China orders it. Given that Iran receives so much monetary support from China (China buys a lot of Iranian petrochemical products), if Xi asks for a particular direction on foreign policy, he is likely to get it.

Even if Iran stands down, the real issue is what happens to all those displaced Palestinians. Israel, if the US allows it, will completely flatten Gaza and displace one to two million Palestinians. The hot potato question is, who will accept these refugees into their country? Obviously, Israel doesn’t want them; the whole goal of this exercise is to reduce the population mismatch. Greater Israel (Amman, Zarqa, Irbid, Israel, the Gaza Strip, and the West Bank) is split 50/50 between Palestinians and Israelis. Why would Israel, which has a superior military and economy, accept a solution where their political power would be diluted by half? It’s never gonna happen. The deal might be that Israel’s neighbours sit tight during the slaughter, and the refugees are sent to Western Europe and America. For Western politicians greenlighting this forced migration, today’s refugee is tomorrow’s loyal voter.

Here is a WSJ op-ed where a former Israeli politician argued why the West should take in Palestinian refugees.

This hypothetical solution to the war removes Iran as a threat and allows the Democrats to continue supporting Israel unconditionally. Oil goes down, and the Israel lobby, which can swing an election, continues their support for leading Democrats.

Spending money on stamping out fentanyl and beefing up security in Taiwan is also expensive. Xi agreed to help stop the flow of fentanyl into the US from China and reaffirmed that China has no plans to invade Taiwan.

Wowzers. Xi gave all this, what is he getting in return?

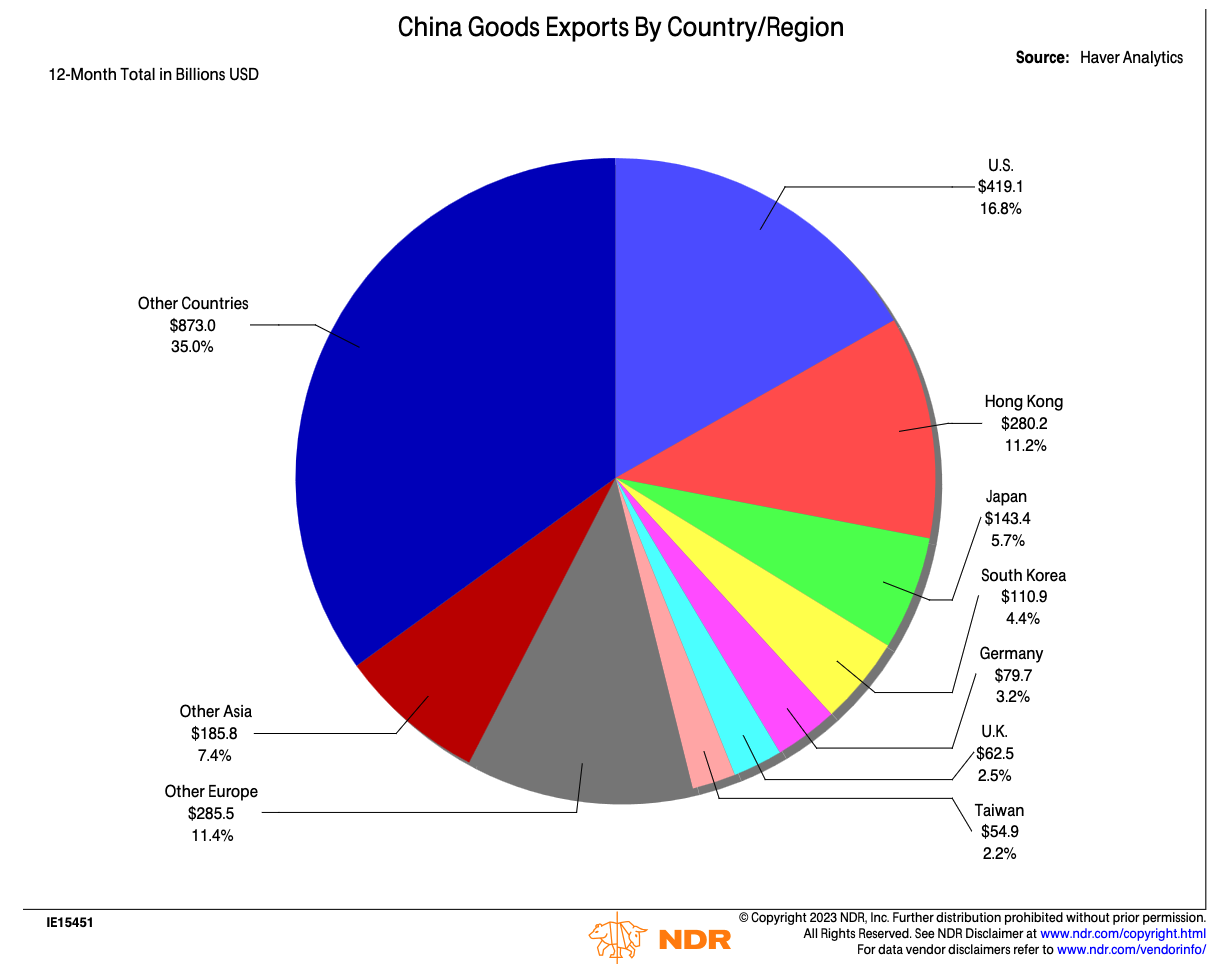

Access to markets:

The China economic model is predicated on selling stuff to wealthy Americans and Europeans. As all parties turned inwards to support their economics, the West implemented tariffs and other policies that reduced certain Chinese imports. A new tone will be set that messages to the market that some of these tariffs will be reduced or removed in the immediate future. As a signal of a new relationship, the Biden team announced the Presidential campaign will now use TikTok. That’s quite a development; I thought TikTok was a corrosive piece of commie tech that was destroying democracy in America. I guess not in an election year.

Foreign Capital Injections:

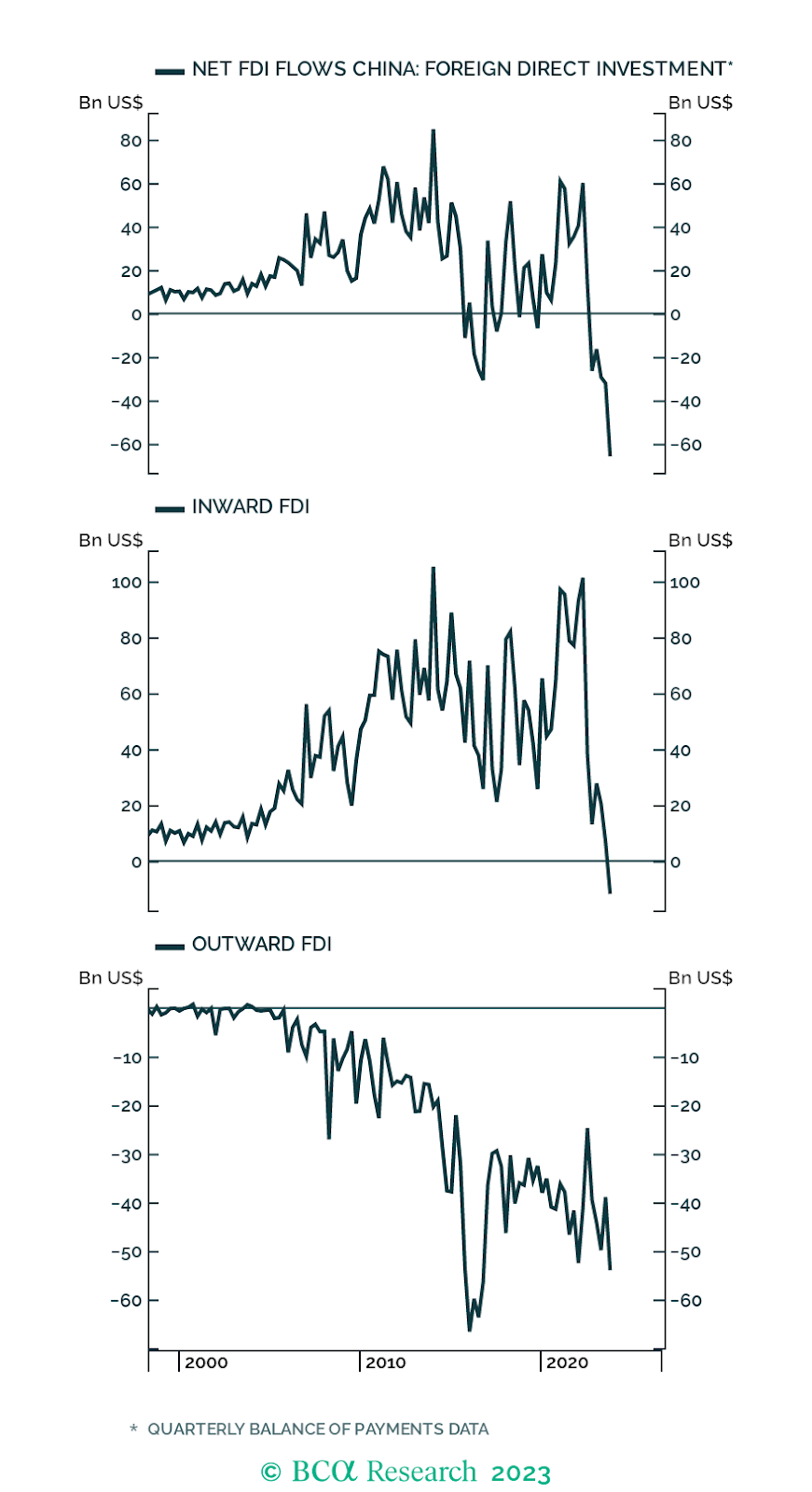

Foreign Direct Investment (FDI) recently turned negative. This is very bad for China. Foreign capital is great because technology transfer, or intellectual property theft as American politicians describe it, to local firms comes with it. That is how China went from a low-cost manufacturing hub that just copied Western designs to a leader in many new technological fields. Foreign capital also means that China’s infrastructure buildout is financed with other people’s money and not debt issued by the local banking system.

It is also bad for the sentiment of onshore retail investors if all the supposed smart foreigners are dumping their holdings indiscriminately to get out ASAP. If the rhetoric from Washington was positive on the future economic collaboration between the US and China, foreign capital would feel safe returning. The last thing a New York or London hedge fund manager wants to happen is for the US to slap financial sanctions on China and trap their money in the Mainland indefinitely. If these sorts of actions are taken off the table, then China once again presents a great market for growth, and capital will flood back into projects and financial markets.

As these charts show, FDI turned negative very quickly in 2023.

Weak dollar:

China desperately needs to engage in a massive round of stimulus to pump up the property market, and increase infrastructure spending to get people back to work. However, as long as the Federal Reserve (Fed) is tightening monetary conditions, if China issues a significant amount of credit, the yuan gets torched. As the yuan weakens, capital flight intensifies and harms the broader economy. China needs the Fed to, at the very minimum, hold conditions steady and hopefully start cutting rates so that the dollar weakens. Then, even though China is going nuts with money printer go brrr, relative to the dollar, the yuan will at the very least be flat, and it might even appreciate.

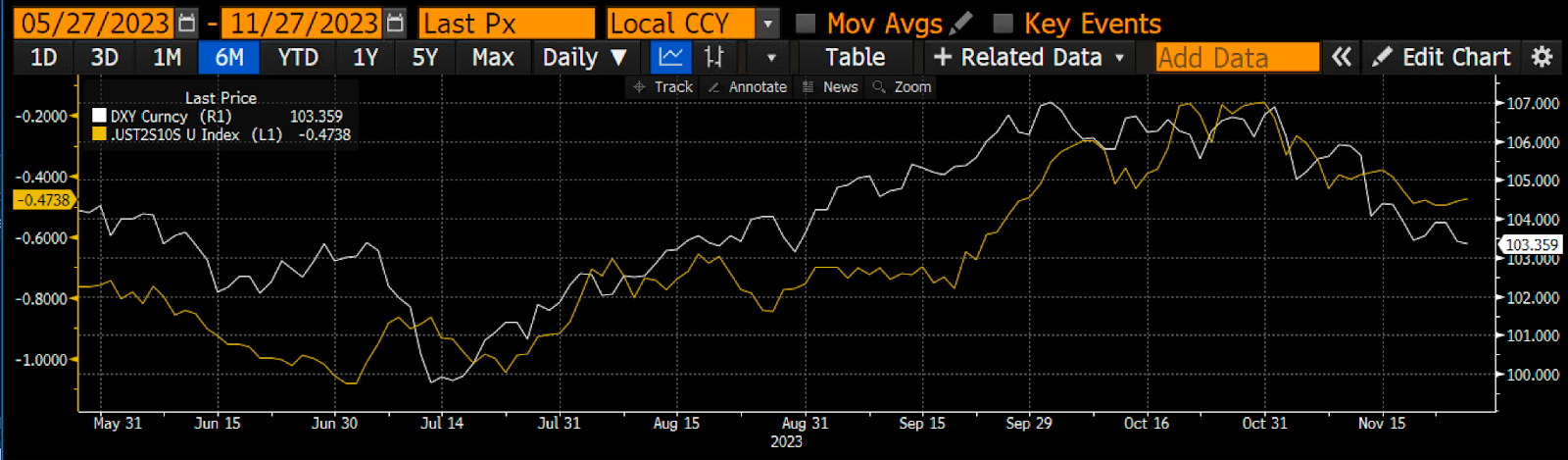

Bad Gurl Yellen is already hard at work weakening the dollar by issuing more Treasury bills, which causes the Fed’s Reverse Repo Program (RRP) balances to fall. I spoke about this in my previous essay, “Bad Gurl”. Since early November, the dollar index DXY has fallen. The weak dollar strategy is already bearing fruit.

As the dollar (DXY Index in white) strengthened, it caused the bear steepener (2s10s spread in yellow) to rise which increased stress on the US Treasury market and US banking system. That is why starting in late October Yellen had to institute a weak dollar policy to save the system.

Before I move on, I want to briefly present another viewpoint on the same US / China jamboree from my macro daddy Felix Zulauf. I’ll preface this with the statement: you don’t always agree with your parents.

In a recent newsletter entitled “FOMO Fever,” Felix espoused a view that nothing of consequence was actually agreed upon at this meeting. Furthermore, the structural issues of the post-WW2 trade and financial architecture, which invariably led to the current situation, were not resolved.

Remember this chart: whatever the new global economic structure is, it will have to address these imbalances.

I agree and disagree with that viewpoint. I agree that the overarching global trade architecture has not been altered. If anything, the imbalances are set to worsen as China is temporarily allowed to export more into the West so that officials can raise the confidence level of the Chinese proletariat.

I disagree that it will not have a short-run impact, however. In the short run, let’s say that in two to three years, the Democrats need to win an election. If the threat of four wars on the periphery is removed, which causes energy inflation and bond yields to fall, that helps Newsom win a 2024 election. On the Chinese side, Xi just took over his third term as Party Chairman in 2022. He needs to show his constituents that by giving him the most power since Chairman Mao, he can bring home the bacon and rejuvenate the economy immediately. Both sides need short-term wins to appease their domestic power bases. Near the end of the decade, all the real issues will resurface, and at that point, a rewrite of the global trade, security, and economic architecture will be unavoidable. This may lead to a hot or cold war between the two global hegemons.

Now that I have given both viewpoints some airtime, let’s not become too obsessed with the medium-term future dystopia and miss profiting from the near-term utopia.

China is Uninvestable

Everyone knows that everyone knows the Chinese economy is in big trouble. The Western money managers know it, and the Chinese officials know it too.

MSCI World (yellow) CSI300 (white) indexed at 100

China’s stock market is in the shitter because it is down 8% vs. MSCI World, which is up 14%. China was supposed to rock ‘em sock ‘em robots as they emerged from Zero COVID earlier this year. But China, absent a truly immense amount of printed money, cannot jump-start its economy.

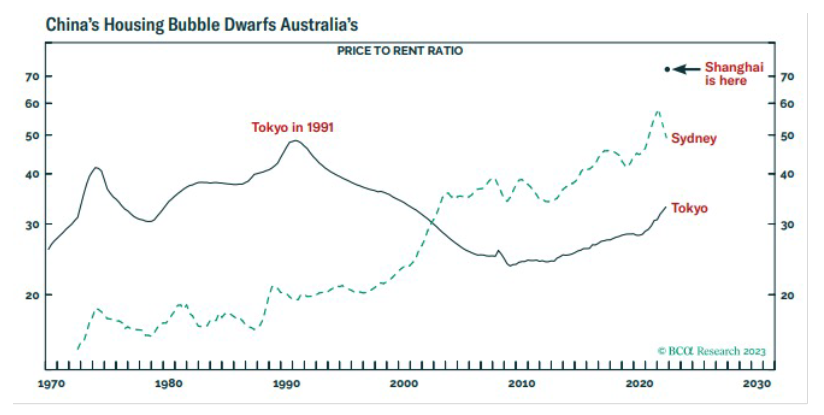

The property market is figgity fucked. It is a bigger bubble than even Tokyo in 1989. The big problem with the property market bubble popping is that ordinary Chinese people will be the most affected. They were heavily incentivized to save in the form of owning overvalued apartments. Given that the government is seen to direct all economic matters, if prices fall, the average Zhou will express anger towards the government.

This puts the Party in a tough spot. The losses must be recognised, but who should pay, individuals, local governments, banks, or the central government? This is a complicated political issue because each constituent is powerful in its own right and can disrupt social harmony. After over a century of civil wars and foreign occupations, social harmony is the most important good the Party must deliver to the people. Their rule depends on it.

Xi tried to do the right thing by attempting to deflate the bubble by restricting the credit to developers, which is called the “Three Lines” policy. The result was a swath of defaults that have been so disruptive Beijing has instructed the banks to lend free again to developers in hopes this will spur comrades to place faith again in the property market.

“Chinese authorities are putting pressure on state banks to accelerate lending to private property developers, as they strengthen efforts to revive the country’s debt-stricken real estate market by supporting some of its biggest and most precarious companies.” – FT

While Beijing has reaffirmed its commitment to supporting the property sector and the economy in general, the rate of credit growth is not large enough to right the ship.

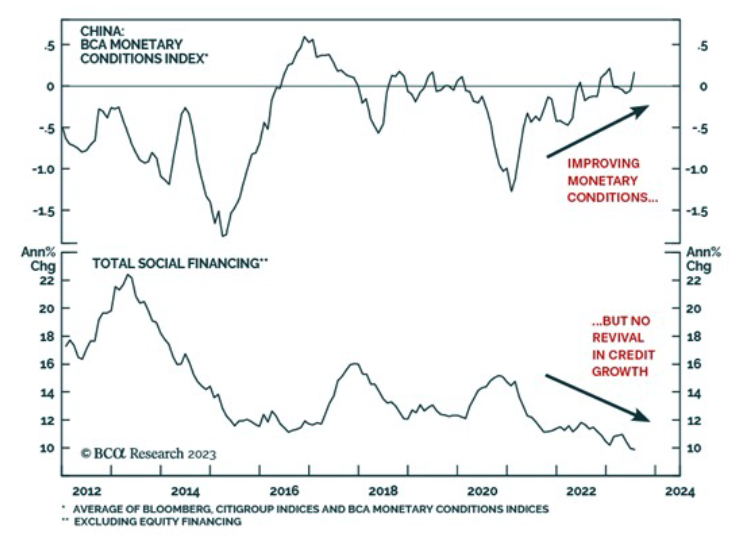

Total Social Financing (TSF) is the catch-all term for Chinese credit growth. China is so large and unwieldy that no one knows exactly how much credit is flowing through the economy. TSF is the best guestimate that is published directly by the People’s Bank of China (PBOC). If China is going to really get its act together, TSF growth needs to reach levels seen in the years following the 2008 Global Financial Crisis. China bailed out the world by spending money with no abandon from 2008 to 2015.

Contrary to popular belief, credit is getting more expensive in China. This dovetails with the previous chart. Beijing is holding back on allowing credit growth to accelerate to levels needed to inspire confidence in the economy once more.

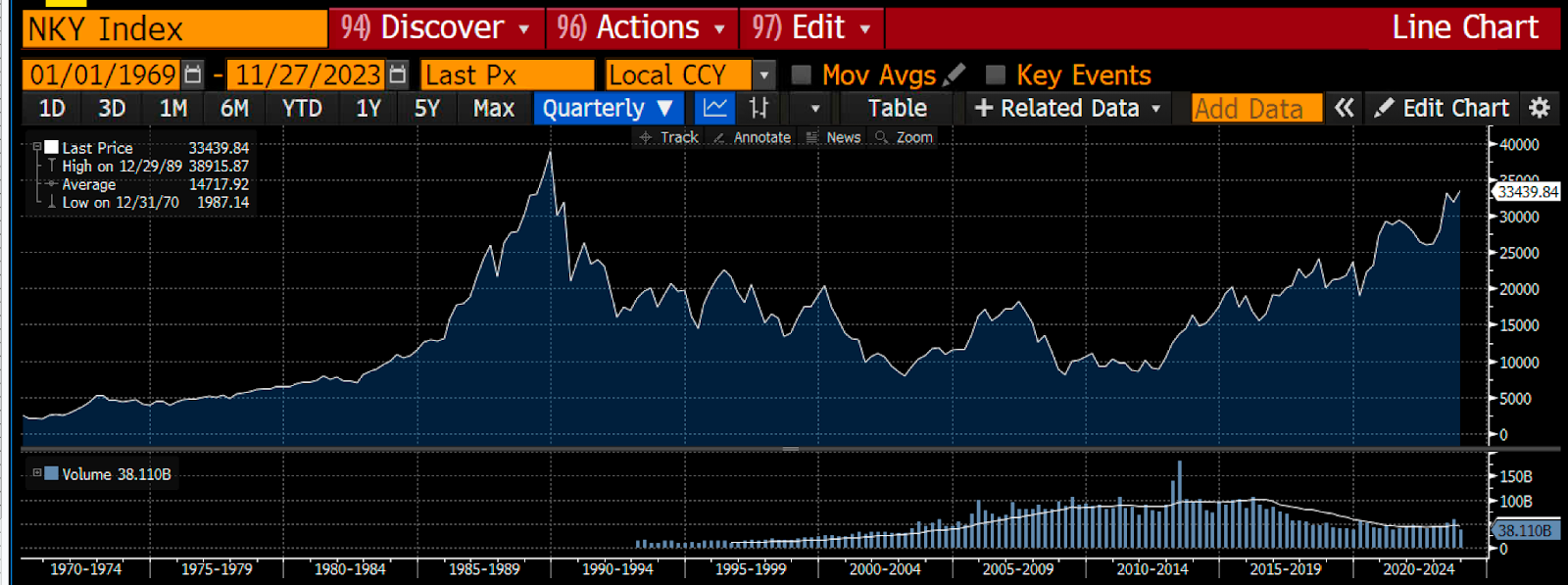

The market desperately wants to believe that China is ready to do what it takes to propel its economy. However, the official data leaves much to be desired. It appears that Beijing is all talk – it is not willing, for good reason, to really press that brrrr button. That is why the market shrugs off China as an investment destination. They fear China is set for a few decades of low to no growth matching Japan from 1990 to the present. The Japanese Nikkei 225, for example, still hasn’t regained its 1989 peak. Does a similar fate await those invested in Chinese equities?

Nikkei 225 Index

Time for Change

What has changed is the recoupling of ChiMerica. Even if this cosier relationship only lasts a few years, it gives the Chinese cover to do what the world desires … print money as they did from 2008 to 2015.

Let me first step through a few charts to show the time is now to flood the world with yuan credit.

The Yuan Will Strengthen

The blue-shaded area is a chart showing the deviation of the PBOC fixing for the CNY vs. the market fair value. The higher the amount, the more the CNY should weaken against the USD. What you can see is that due to the weakening JPY (green), the CNY (yellow) was under pressure to weaken, but the PBOC held it stronger than it should have been. That is expensive because it means the PBOC is selling USD assets in order to keep the CNY artificially strong.

Now that Bad Gurl Yellen is running a weak dollar policy, the PBOC doesn’t have to spend precious dollars to prop up the CNY. The JPY is strengthening and recoupling with the strong CNY. Japan is China’s largest export competitor. If the yen weakens, the yuan must weaken so Chinese exporters remain globally competitive. The CNY is now fairly valued and will actually strengthen as the dollar continues to weaken. This gives China the wiggle room to dramatically increase the amount of onshore CNY credit without the currency weakening or putting immense pressure on the PBOC to hold the currency stronger than it should be.

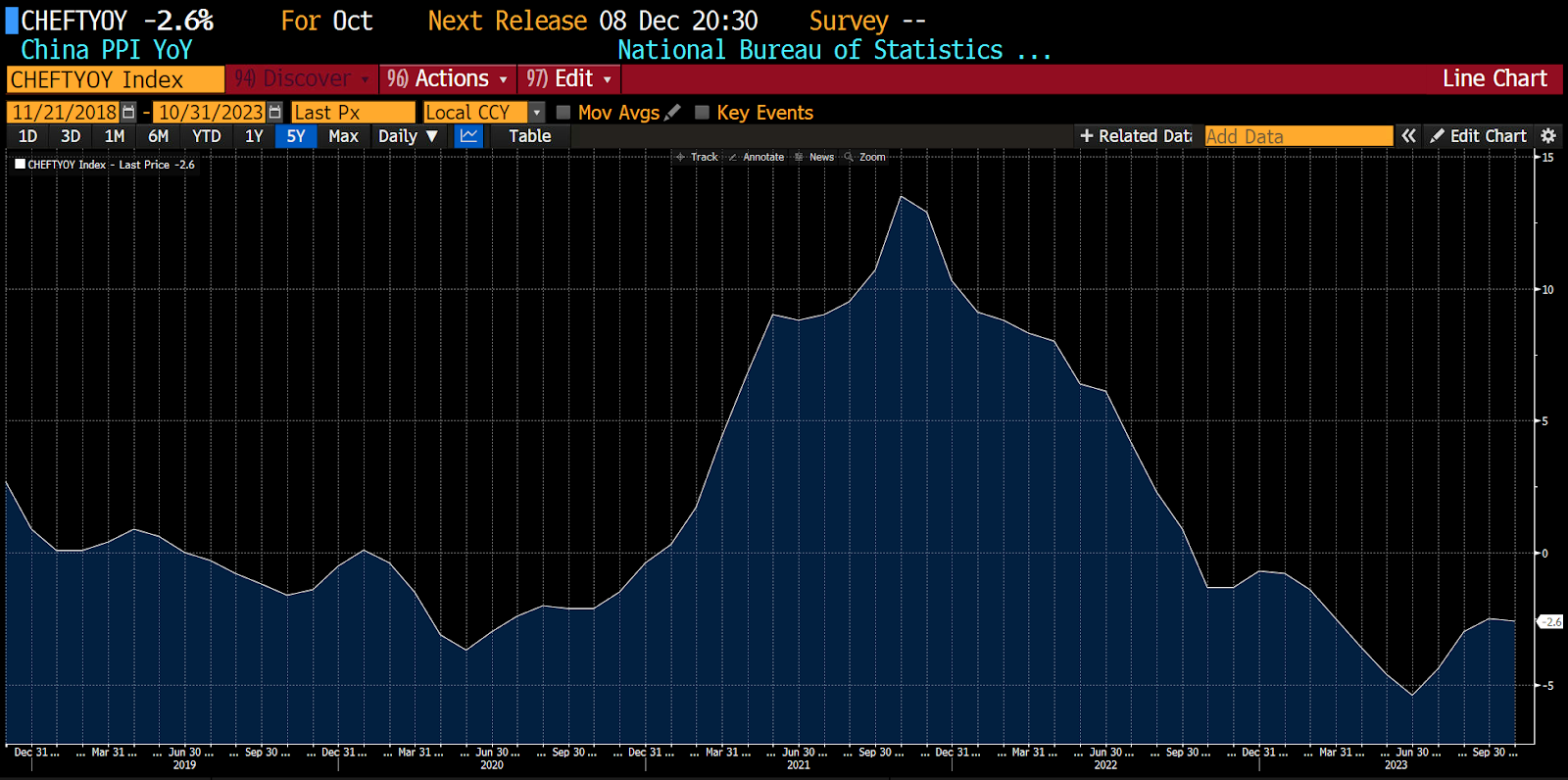

China Is In Deflation

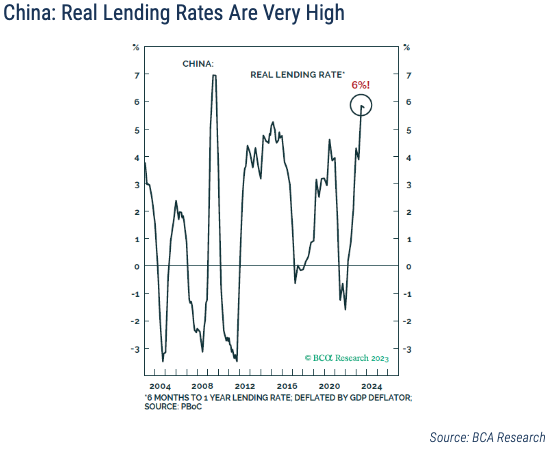

China’s economy is built on infrastructure investment and manufacturing, not consumer purchases, which is referred to as a supply-side or supply-led economic structure. Therefore, the inflation statistic most relevant is the Producer Price Index (PPI), not the Consumer Price Index (CPI). PPI is falling, which means the supply side of the economy is unwell.

The PBOC has a lot of scope to ease via increased credit growth because PPI is in deflationary territory.

As I have illustrated above, China has the breathing room to dramatically increase credit. The credit expansion will not result in higher inflation because PPI is deflationary territory. It will not result in a weakening of the currency, which causes capital flight, because the US is running a weak dollar policy, and the yen is strengthening.

Even if this all quickly comes to pass, how and why do we crypto traders make money?

Property Bailout

The most apparent way that Beijing will funnel credit into the Chinese economy is by bailing out property developers. The major banks will be ordered to lend at affordable rates to developers. Also, developer and local government loans backed by land or property assets will be rolled over with no penalties. Given that property development and finance are the largest sectors of the Chinese economy at almost 25%, this will, in effect, lower the real cost of interest in the Chinese economy.

Michael Pettis, a former Bear Stearns bond trader and current professor at Peking University, believes that China exhausted its capacity to absorb debt in the early 2000s. Since then, all debt added has been malinvested in various projects that do not earn a rate of return in excess of the debt’s rate of interest. The result is that while trillions of yuan have been allocated to this and that project, society gets poorer and poorer because it becomes almost impossible for future economic growth to match interest costs and principal repayments.

As real interest rates fall, SOE companies that manufacture things will, in theory, be able to expand production. Of course, there will be more Chinese knick-knacks flooding the American and European markets. However, a bulk of the financing will be used to speculate in the financial markets as the world just doesn’t need more stuff. This is because, as Pettis argues, China cannot profitably absorb more debt, so it gets punted in the financial markets instead.

Capital, by which I mean digital fiat credit money, is globally fungible. If China is printing yuan, it will make its way into the global markets and support the prices of all types of risk assets. If a significant portion of the hundreds of billions of USD worth of CNY makes its way outside of China, then the only reason that SOE’s and households are speculating in the global financial markets is because there are insufficient real uses of capital at home.

There are micro and macro ways in which capital makes its way from China into Bitcoin.

Micro

Hong Kong is China’s window to the global capital markets. SOE’s and wealthy Chinese people are all banked out of Hong Kong for any international dealings. Hong Kong now has a few fully licensed crypto exchanges and brokers where Bitcoin can be purchased.

Bitcoin is a Chinese phenomenon. Many of the largest Bitcoin miners started their operations in China. Pre-2020, when BTC/CNY trading pairs were available, Chinese clients dominated global spot trading flows. Any wealthy coastal Chinese person knows about Bitcoin and its promise as a store of value. They have watched the currency from its infancy until the current moment and have been active participants in its success. If there is a way to legally move cash from the Mainland to Hong Kong, Bitcoin will be one of many risk assets that will be purchased.

Macro

Since the late 2010’s, the Chinese authorities have been attempting to rebalance the Chinese from a supply-led to a demand-led economy. At a fundamental level, they affect this policy by making credit more expensive onshore. This shifts activity away from capital-intensive heavy industry and more towards consumer goods and services. Therefore many firms, property developers being some of the most prolific, resorted to borrowing dollars offshore. This demand for dollars and the repayment of said dollar loans pushes up the dollar’s value and makes credit more expensive globally. That bid for dollar credit and liquidity will be removed as the Chinese banking system provides more plentiful yuan credit.

Given that the dollar is the world’s largest funding currency, if the price of credit falls, all fixed supply assets like Bitcoin and gold will rise in dollar fiat price terms. The great part about this macro pillar of bullishness is that it doesn’t require Chinese firms and wealthy individuals to buy any Bitcoin. The fungible nature of global fiat credit will dictate that the marginal fiat dollar will flow into hard monetary assets like Bitcoin.

2024 and Beyond

There is nothing like an election year to force optical change. The number one job of any politician is to be re-elected. The Democratic party will do whatever it takes, and they have shown a willingness to do so by placing former President Trump under arrest to remain the top dog. As such, expect a friendly Biden administration to push any small China / US misunderstandings under the rug.

Xi is no fool and knows this marriage of convenience will be very short-lived. Slow Joe fucked up and told the world what he really thinks about Xi, in that he is a dictator. Obviously, that wasn’t part of the plan, as Biden’s handlers cringed off on the sidelines at the gaff. If it means getting into bed with China, the Democrats will do it so that the economy appears strong on election day. That’s great, but what if they lose? The Republicans now have an easy dig on the Dems in that they kowtowed to commie China. Just look how quickly the homeless were ushered out of sight, out of mind in the Democratic-run city of San Francisco. I thought they had rights …

The window to flood China with credit and not suffer negative consequences is now. If Bad Gurl Yellen was running a strong dollar policy, there would be no way for China to turn the credit taps on to the degree required to re-energise the economy. Given these facts, China will go big. Because after election day, regardless of who wins, the gloves come off again, and you can expect a change in trade and monetary policy aimed at restarting the strategic competition between the US and China.

There are no sure things in financial markets. When I started writing this essay, it appeared that the two pro-China parties in Taiwan (KMT and TPP) would unite under one ticket to best the pro-independence DPP candidate in the presidential election. However, at the last minute, the deal fell apart, and both pro-China candidates officially filed their intention to stand for the presidency. I expect China to put sufficient pressure to get either the KMT or the TPP candidate to drop out so they don’t split the vote. China successfully nudged Foxconn founder Terry Guo to drop out due to increased regulatory scrutiny of his massive manufacturing business onshore. Xi knows how to dangle a carrot and stick to force compliance with the Party’s diktats.

If either the KMT or TPP wins the election, I expect the China credit bazooka to be strong to very strong. Otherwise, it’s more up in the air on how much stimulus Beijing wants to provide. The last thing Xi wants to do is blow his credit load onshore but then have to spend more to increase military posturing towards a newly aggressive Taiwan. I will be following this election closely.

There is no better place to be than in Asia when China is in bull market mode. It’s just so much fucking fun! I already got my playlist lined up for the K.

Chinese New Year occurs in mid-February next year. I expect that Xi will provide his comrades a phat 红包 (Hong2Bao1) so they return to their families feeling rich and ready to spend once the New Year holidays finish. As such, I will continue moving money out of T-bills and into crypto because I want to get in now before it becomes apparent through the data that China’s money printer is going brrrrr!

Related

The post appeared first on Blog BitMex