(Any views expressed here are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

What do you do when the market is down but you have an election to win?

What do you do when the market is down but you have an election to win?

That’s an easy answer if you are a politician. Your number one goal is to secure re-election. Therefore, you print money and manipulate prices higher.

Imagine you are Kamala Harris, the Democratic Party nominee for US President, facing a formidable Orange Man. You need everything to go right because so much has gone wrong since the last election under your stewardship as Vice President. The last thing you need on election day is a raging global financial crisis.

Harris is an astute politician. And given that she is an Obama stooge, I can bet he is in her ear warning her how bad it would be if a 2008 Global Financial Crisis (GF) were to land on her doorstep a few months out from the election. US President Slow Joe Biden is out on the vegetable patch, so the assumption is that Harris is running the show.

George W. Bush was about to finish his second term as president when Lehman Brothers went bankrupt in September 2008, which kicked off the GFC for realz. Given that he was a Republican President, one could argue that part of Obama’s appeal as a Democrat was that he was a member of the other party and, therefore, not responsible for the economic slump. Obama went on to win the 2008 presidential election.

Let’s focus back on Harris’ dilemma of what to do about a developing global financial crisis sparked by the unwinding of Japan Inc.’s monster yen carry trade. She could let the chips fall as they may, allow the free market to destroy overleveraged businesses, and permit wealthy baby boomer financial asset holders to experience some real pain. Or, she could instruct US Treasury Secretary Bad Gurl Yellen to fix it with printed money.

Like any politician, regardless of party affiliation or economic beliefs, Harris will instruct Yellen to use the monetary tools available to her to avert a financial crisis. Of course, that means the money printer will go brrr in some way, shape, or form. Harris will not want Yellen to wait – she’ll want Yellen to act forcefully and immediately. Therefore, if you share my view that this yen carry trade unwind could collapse the entire global financial system, you must also believe that Yellen will swing into action no later than the opening of Asian trading next Monday, August 12th.

To impress upon you the size and magnitude of the potential effects of a Japan Inc. carry trade unwind, I will step through an excellent research piece by Deutsche Bank from November 2023. Then, I will walk through how I would construct a bailout if, by some act of the devil, I was put in charge of the US Treasury.

The Widow Maker

What is a carry trade? A carry trade is when you borrow a currency with a low interest rate and buy financial assets in another currency that yield more or have a higher chance of appreciating. When it comes time to repay the loan, money is lost if the currency borrowed appreciates relative to the currency of the assets you purchased. If the currency borrowed depreciates, money is made. Some investors hedge the currency risk; some do not. In this case, because the BOJ can print an infinite amount of yen, there is no need for Japan Inc. to hedge its borrowed yen.

Japan Inc. refers to the BOJ, corporations, households, pension funds, and insurance companies. Some entities are public, some are private, but they all act together to better Nippon, or at least they intend to.

Deutsche Bank wrote an excellent report entitled “The World’s Biggest Carry Trade” on 13 November 2023. The author asked the rhetorical question, “Why hasn’t the yen carry trade blown up and taken the Japanese economy down with it?” The situation today is quite different than it was at the end of last year.

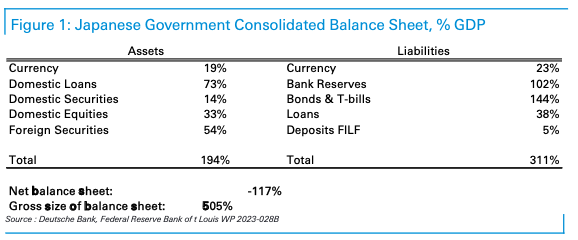

The narrative is that Japan is highly indebted. Hedge fund bro after hedge fund bro has bet that a collapse is imminent. But those who have bet against Japan have always lost. It ain’t called the “Widow Maker” trade for nothing. So many macro investors are too bearish on Japan because of their failure to understand Japan’s consolidated public and private balance sheets. It is an easy mental mistake for a Western investor who believes in individual rights. But in Japan, the collective reigns supreme. Therefore, certain actors who would be deemed private in the West are just alternate arms of the government.

Let’s first tackle the liability side. These are the things that fund the carry trade. This is how yen is borrowed. There is an interest cost attached to them. The two main line items are Bank Reserves and Bonds & T-bills.

Bank Reserves – these are funds banks hold at the BOJ. The amount is significant because the BOJ creates bank reserves when it engages in bond purchases. Remember, the BOJ owns almost half of the JGB market. Therefore, the amount of bank reserves is massive, at 102% of GDP. The cost of these reserves is 0.25%, which the BOJ pays to the banks. For context, the Fed pays 5.4% on excess bank reserves. This funding cost is practically zero.

Bonds & T-bills – these are JGBs issued by the government. Due to the BOJ’s market manipulation, JGB yields are at rock bottom levels. The current on-the-run 10-yr JGB yields, around the time of publishing, is 0.77%. This funding cost is meagre

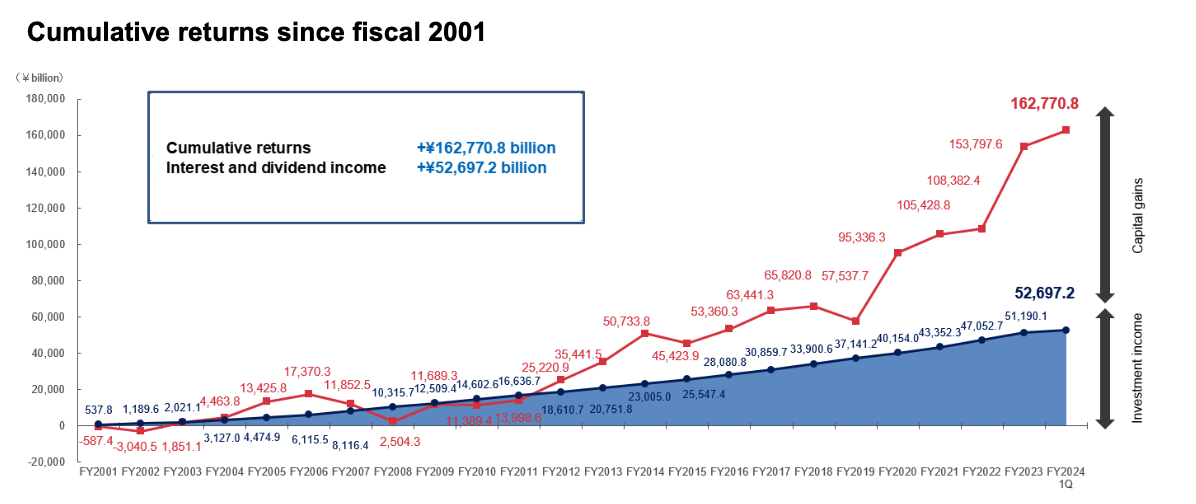

On the asset side, the most extensive line item is Foreign Securities. These are the financial assets the public and private sectors own abroad. One massive private holder of foreign assets is the Government Pension Investment Fund (GPIF). At $1.14 trillion, it is one of the largest, if not the largest, pension funds in the world. It owns foreign stocks, bonds, and real estate.

Domestic Loans, Securities, and Equities also all perform well when the BOJ price fixes bonds. Finally, yen depreciation, as a result of the massive creation of yen liabilities, elevates the domestic stock and property market.

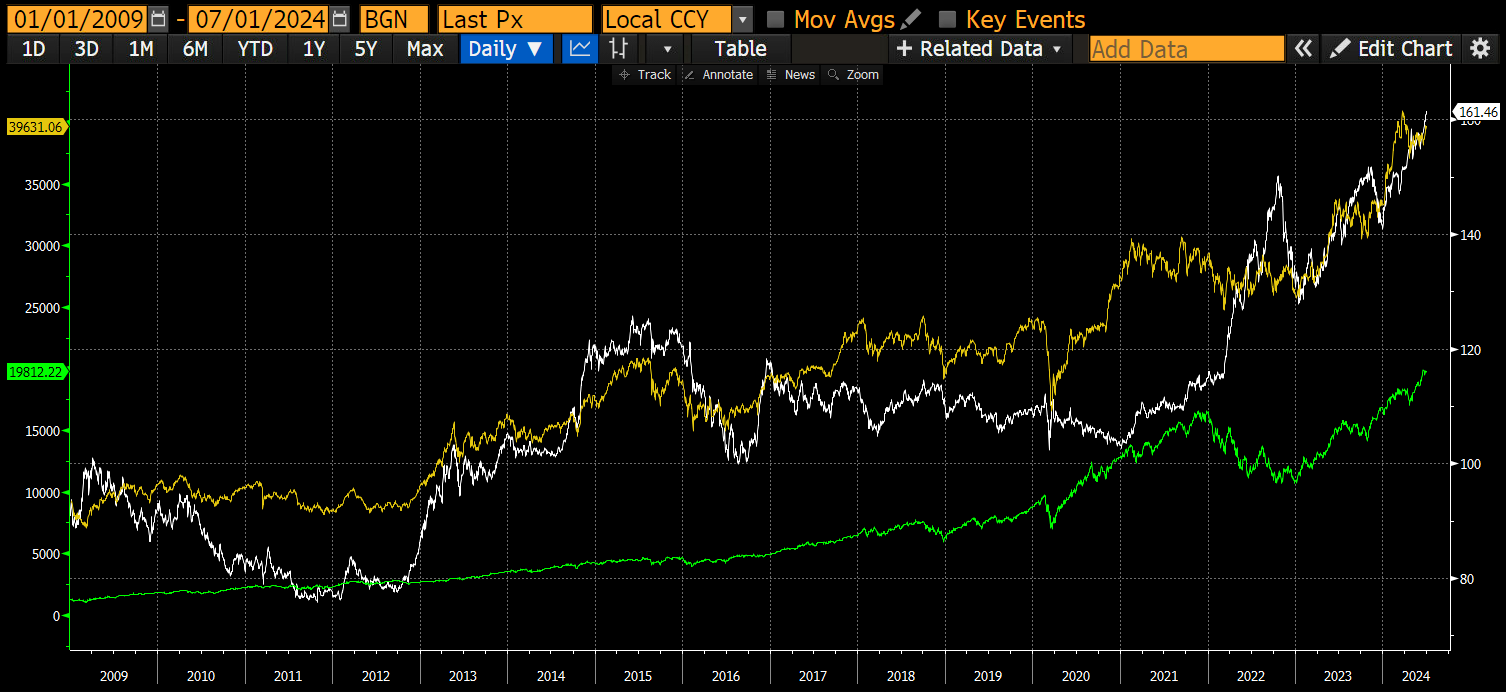

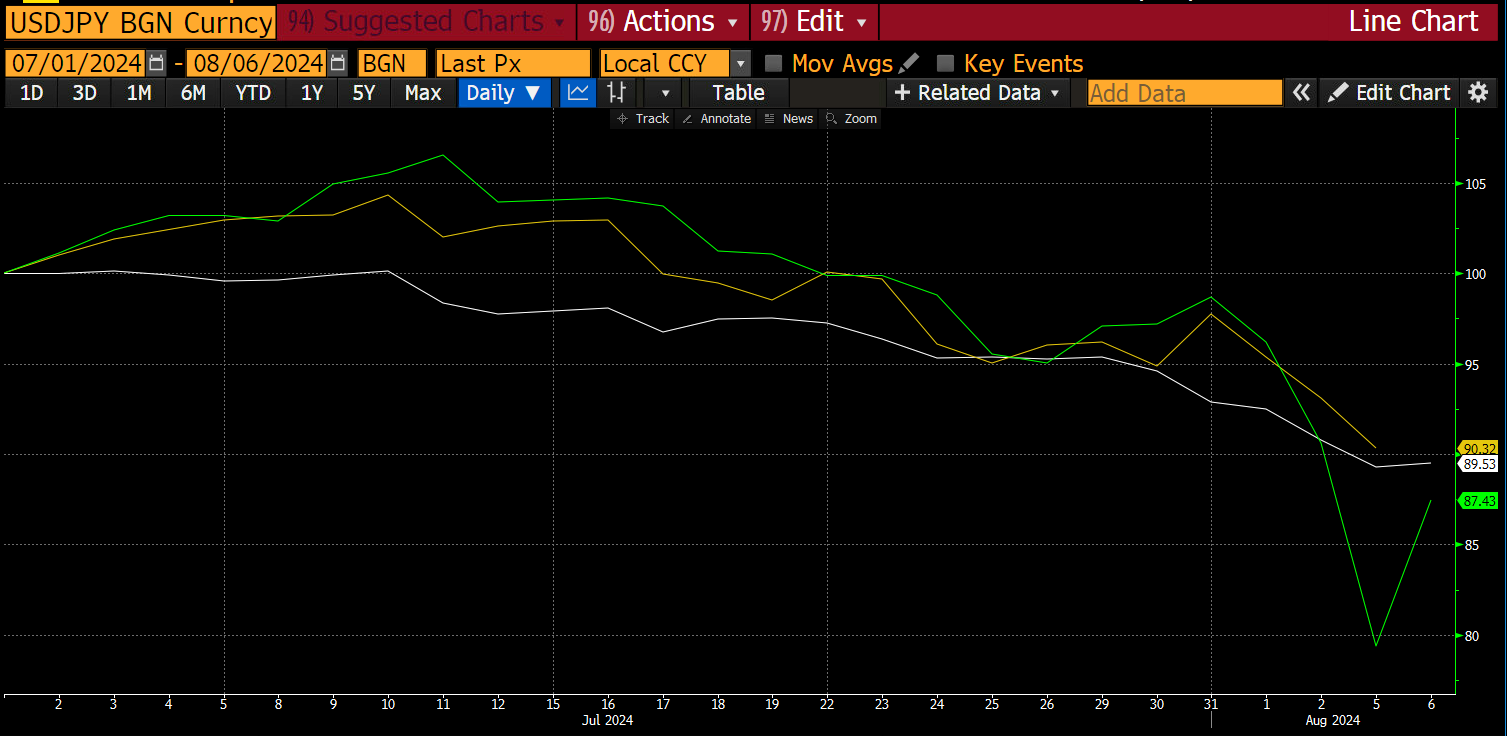

The dollar-yen (white) rose, which means the yen weakened vs. the dollar. It took the Nasdaq 100 Index (green) and the Nikkei 225 (yellow) along for the ride.

Taken as a whole, Japan Inc. funds itself using BOJ-imposed financial repression and earns high returns due to the resulting weak yen. This is why BOJ can continue to run the loosest monetary policy in the world in the face of rising global inflation. It’s fucking insanely profitable.

GPIF is kicking ass, and even more so over the last decade. What has happened over the previous decade is that the yen has depreciated massively. As the yen depreciates, the return on foreign assets jumps.

GPIF would have lost money last quarter if not for the stellar returns of its foreign stock and bond portfolio. Domestic bonds lost money because the BOJ exited YCC, which caused JGB yields to rise and prices to fall. However, the yen continued to weaken because the interest rate differential between the BOJ and the Fed is wider than Sam Bankman-Fried’s eyes when he spots an Emsam pill.

Japan Inc. put this trade on in MASSIVE size. Japan’s GDP is roughly $4tn, with a gross exposure of 505%, and they are running $24tn worth of risk. As Cardi B says, “I want you to park that big Mack truck right in this little garage.” She was definitely rapping about the Japanese men running the show in the Land of the Setting Sun.

This trade obviously worked, but the yen got too weak. The Dollar-yen pair at 162 earlier in July was too much to bear because domestic inflation was and is currently raging.

The BOJ did not want to shut down this trade immediately, instead aiming to exit slowly over time … that’s what they always say. Ueda-domo took over as the governor of the BOJ in April 2023 from Kuroda-domo, the chief architect of this massive trade. He got out while the getting was good. Ueda-domo was the only schmuck left in the pool of eligible candidates who wished to commit seppuku by attempting to unwind this trade. The market knew Ueda-domo would try to extricate the BOJ from this carry trade. The question was always about the pace of normalisation.

The Unwind

What could a disorderly unwind look like? What would happen to the various assets held by Japan Inc.? How much would the yen appreciate?

To unwind this trade, the BOJ needs to raise rates by ceasing to purchase JGBs and ultimately selling them back into the market.

On the liability side, what happens?

Without the BOJ constantly stomping on JGB yields, they will rise as the market demands, with a yield that, at the very least, matches inflation. Japan’s consumer price index (CPI) rose 2.8% on a YoY basis in June. If JGB yields rise to 2.8%, higher than any bond yields at any point on the yield curve, the cost of debt at any tenor will increase. The interest cost of bonds and T-bills liability line item surges.

The BOJ must also raise the interest paid on bank reserves to prevent that money from escaping its clutches. Again, given the notionals involved, this cost will go from nearly zero to gigantic.

In short, allowing interest rates to rise to a market-clearing level will necessitate the BOJ paying billions of yen worth of interest annually to fund its position. Without any income from sales of assets on the other side of the ledger, the BOJ would have to print an enormous amount of yen to remain current on its liabilities. Doing that would worsen the situation; inflation would rise and the yen would weaken. Therefore, assets must be sold.

On the asset side, what happens?

The biggest headache for the BOJ is how to sell its massive pile of doo-doo JGBs. Over the past two decades, the BOJ destroyed the JGB market via its various quantitative easing (QE) and yield curve control (YCC) programs. For all intents and purposes, there is no more JGB market. The BOJ must force another member of Japan Inc. to do their duty and purchase JGBs at a price that would not send the BOJ into insolvency. When in doubt, call on the banks.

Japanese commercial banks were forced to de-lever after the 1989 property and stock market bubble burst. Since then, bank lending has been moribund. The BOJ got into the money-printing game because corporates were not borrowing from banks. Given that the banks are healthy, it is time to slam a few quadrillion yen worth of JGBs back onto their balance sheets.

While the BOJ can tell the banks to buy bonds, the banks need to get the capital somewhere. As JGB yields rise, profit-seeking Japanese businesses, alongside banks that hold trillions of dollars’ worth of foreign assets, will sell these, repatriate the capital back to Japan, and deposit it into a bank. The bank and these corporates will buy JGBs in SIZE. The yen strengthens due to the inward capital flows, and JGB yields do not rise to levels that put the BOJ out of business while they reduce their holdings.

The major casualty is the declining prices of foreign stocks and bonds that Japan Inc. sells to generate capital to repatriate. Given the enormous size of this carry trade, Japan Inc. is the marginal price setter for stocks and bonds globally. This is especially true for any Pax Americana listed security as their market is the preferred destination for yen carry trade financed capital. Many TradFi trading books mirror Japan Inc., given that the yen is a freely convertible currency.

As the yen weakens, more and more investors globally are encouraged to borrow yen and buy US equities and bonds. Everyone rushes to cover simultaneously as the yen strengthens because they are highly leveraged.

I showed you a chart earlier of what happens when the yen weakens. What happens when it strengthens just a tiny bit? Remember the early chart showing dollar-yen’s stroll from 90 to 160 in 15 years? In 4 trading days, it went from 160 to 142, and this is what happened:

Dollar-yen (white) strengthened 10%, the Nasdaq 100 (white) dropped 10%, and the Nikkei 225 (green) dropped 13%. This is a roughly 1:1 ratio between the yen’s percentage rise and equity indices’ fall. Extending this further, if the dollar-yen reached 100, a 38% move, the Nasdaq would drop to ~12,600 and the Nikkei to ~25,365.

A dollar-yen move to 100 is plausible. A 1% de-grossing of Japan Inc.’s carry trade corresponds to a notional of ~$240bn. At the margin, this is a fuck ton of capital. Different players in Japan Inc. have different sub-priorities. We saw this with the fifth largest Japanese commercial bank, Norinchukin. Their part of this carry trade blew up, and they were forced to begin unwinding. They are selling down their positions in foreign bonds and covering forward dollar-yen FX hedges. This announcement occurred only a few months ago. Insurance companies and pension funds will be under pressure to disclose unrealised losses and exit trades. Alongside them are all the copy traders who will be liquidated quickly by their broker as currency and equity volatility rises. Remember, everyone is unwinding the same trade all at once. Neither we nor the elites running global monetary policy have any idea what the total size is of the yen carry trade-funded positions that are lurking within the financial system. The opacity of the situation means a swift overcorrection in the other direction as the market shines light on this highly leveraged part of the global financial system.

Spooked

Why does Bad Gurl Yellen care?

Since the 2008 GFC, I argue that China and Japan saved Pax Americana from an even more severe economic downturn. China engaged in one of the largest fiscal stimulus exercises in human history, manifesting itself through a debt-fueled infrastructure buildout. China needed to purchase goods and raw commodities from the rest of the world to complete projects. Japan, via the BOJ, printed an enormous amount of money to gross up its carry trade. With those yen, Japan Inc. bought US equities and bonds.

The US government earns a substantial amount of income from capital gains taxes, which are the result of a roaring stock market. From January 2009 until early July 2024, the Nasdaq 100 rose 16x, and the S&P 500 rose 6x. Capital gains tax rates range from roughly 20% to 40%.

Despite the record capital gains tax haul, the US government still runs a deficit. To finance that deficit, the Treasury must issue debt. Japan Inc. is one of the largest marginal buyers of Treasury debt … or at least they were, until the yen began strengthening. The Japanese help keep US debt affordable for profligate politicians who need to buy votes with tax cuts (Republicans) or various forms of welfare checks (Democrats).

The total amount of US debt outstanding (yellow) is up and to the right. However, 10-yr Treasury bond (white) yields have been pretty range-bound and practically uncorrelated with the growing pile of debt.

My point is that the structure of the US economy requires Japan Inc. and those aping them to remain in this carry trade. Should this trade unwind, the finances of the US government will be torn to shreds.

The Bailout

My assumption about a coordinated bailout of Japan Inc.’s carry trade positions rests on my belief that Harris will not allow her election chances to wane because some foreigners there decided it was time to exit some trade she probably doesn’t even understand. Her voters certainly have no idea what is happening, nor do they care. Either their stock portfolio is up, or it ain’t. And if it ain’t, they won’t be showing up on election day to vote Democrat. Voter turnout will determine whether the clown emperor is Trump or Harris.

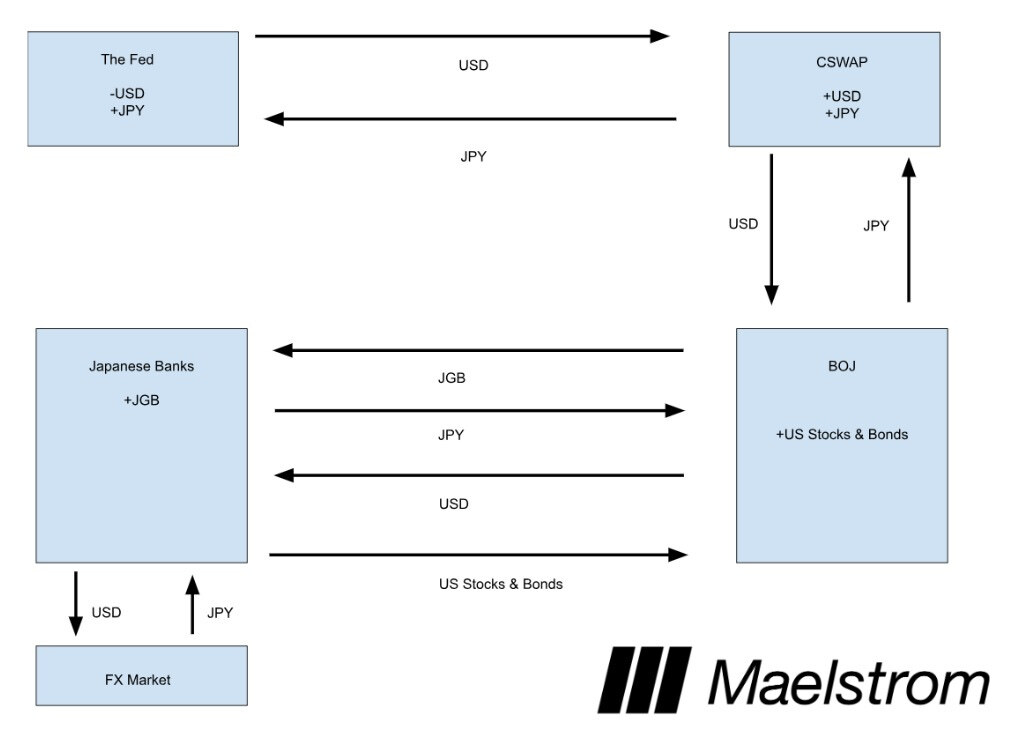

Japan Inc. must unwind its positions, but it cannot sell certain assets in the open market. That means that some government body in the US must print money and loan it to some member of Japan Inc. Allow me to reintroduce myself. My name is the Central Bank Currency Swap (CSWAP).

Let me walk you through how I would conduct a bailout if I were Bad Gurl Yellen.

On Sunday night, August 11th, I would release a communique (I’m speaking as if I were Yellen):

The US Treasury Department, Federal Reserve, and our counterparts in Japan spoke at length about the volatile market conditions of the past week. During this call, I reiterated our support for the usage of dollar-yen Central Bank Swap lines.

That’s it. To the public, it appears to be completely innocuous. It isn’t some statement where the Fed folds and conducts an aggressive rate cut coupled with the restart of QE. That is because the plebes know that doing any of these would result in a reacceleration of already uncomfortably high inflation. If inflation rages on election day and is easily traced back to the Fed, Harris will lose.

Most American voters have no idea what a CSWAP is, why it was created, or how it can be used to print an infinite amount of money. However, the market will correctly view this as a stealth bailout because of how the facility will be used.

- The BOJ borrows billions of dollars and provides yen as collateral to the Fed. These swaps are rolled over as many times as the BOJ wishes.

- The BOJ speaks privately to large corporations and banks and tells them that it is ready to pay dollars in exchange for US equities and US Treasury bonds.

This transfers ownership of foreign assets from Japanese corporates and banks to the BOJ. Flush with dollars, these private entities repatriate that capital to Japan by selling dollars and buying yen. Then, they purchase JGBs from the BOJ at the current high prices / low yields. The result would be that the size of outstanding CSWAPS balloons, and this dollar amount is akin to the amount of money printed by the Fed.

I created an ugly box and arrow diagram, which will help illustrate the flow.

The net effect is what is important.

The Fed – they increased the amount of dollar supply or, in other words, in return, received yen previously created by the growth of the carry trade.

CSWAP – the Fed is owed USD by the BOJ. And the BOJ is owed JPY by the Fed.

BOJ – they now hold more US stocks and bonds, which will increase in price because the amount of USD rises due to the growing CSWAP balance.

Japanese Banks – they now hold additional JGBs.

As you can see, there is no impact on the US stock or bond market, and Japan Inc.’s gross carry trade exposure remains constant. The yen strengthens against the dollar, and most importantly, US stocks and bonds rose in price due to the Fed printing dollars. An additional bonus is that Japanese banks can issue an infinite amount of yen-denominated loans with their newfound JGB collateral. This trade reflates the system in both the US and Japan.

The Timeline

The unwind of Japan Inc.’s carry trade will happen; of this, I am certain. The question is when the Fed and Treasury will print money to blunt its effects on Pax Americana.

If the US equity markets dump into Friday, August 9th, to such an extent that both the S&P 500 and Nasdaq 100 are down 20% from their recent July all-time highs, then some sort of action over the weekend is probable. For the S&P 500, the level is 4,533; for the Nasdaq 100, it is 16,540. I also expect the 2-yr Treasury note to yield around 3.80% or less. This yield was reached during the March 2023 Regional Banking Crisis, which was dealt with via the Bank Term Funding Program bailout.

If the yen starts to weaken again, the crisis is over in the immediate term. The unwind will continue, albeit at a slower pace. I believe the markets will throw another tantrum between September and November as the dollar-yen pair resumes its death march toward 100. There will definitely be a response this time around, as the US presidential election will be weeks or days away.

Trading this in a crypto fashion is difficult.

Two opposing forces influence my crypto positioning.

Liquidity Positive Force:

After a quarter of net restrictive policy, the US Treasury will net inject dollar liquidity because it will issue Treasury bills and possibly deplete the Treasury General Account. This shift in policy was laid out in the most recent Quarterly Refunding Announcement. TL;DR: Bad Gurl Yellen will inject $301bn to $1.05tn between now and year-end. I will explain this in a subsequent essay if it is warranted.

Liquidity Negative Force:

This is the strengthening of the yen. The unwinding of the trade causes coordinated global selling of all financial assets as yen debt, which gets more expensive by the tick, must be repaid.

Which force is stronger really depends on the pace of the carry trade unwind. This we cannot know a priori. The only observable effect is how Bitcoin correlates with dollar-yen. If Bitcoin trades in a convex fashion, meaning Bitcoin rises in both cases when the dollar-yen pair strengthens or weakens aggressively, then I know that the market expects a bailout if the yen gets too strong and the liquidity provided by the US Treasury is sufficient. This is convex-Bitcoin. If Bitcoin falls as the yen strengthens and rises as the yen weakens, then Bitcoin will trade in lock-step with TradFi markets. This is correlated-Bitcoin.

If the setup is convex-Bitcoin, I will aggressively add positions as we have reached the local bottom. If the setup is correlated-Bitcoin, then I will sit on the sidelines and wait for the eventual market capitulation. The mega assumption is that the BOJ will not reverse course, cut deposit rates back to 0%, and resume unlimited JGB purchases. If the BOJ sticks by the plan it laid out at its last meeting, the carry trade unwind will continue.

That’s as prescriptive as I can be at the moment. As always, these trading days and months will define your returns for this bull cycle. If you must use leverage, use it wisely and constantly monitor your positions. When you have a levered position, you better be babysitting your Bitcoin or shitcoins. Otherwise, you will get liquidated.

Over and out bitches, I have the last leg of my August holiday to enjoy.

Yachtzee!

Related

The post appeared first on Blog BitMex